Estrategia de trading cuantitativo basada en múltiples indicadores técnicos

Resumen

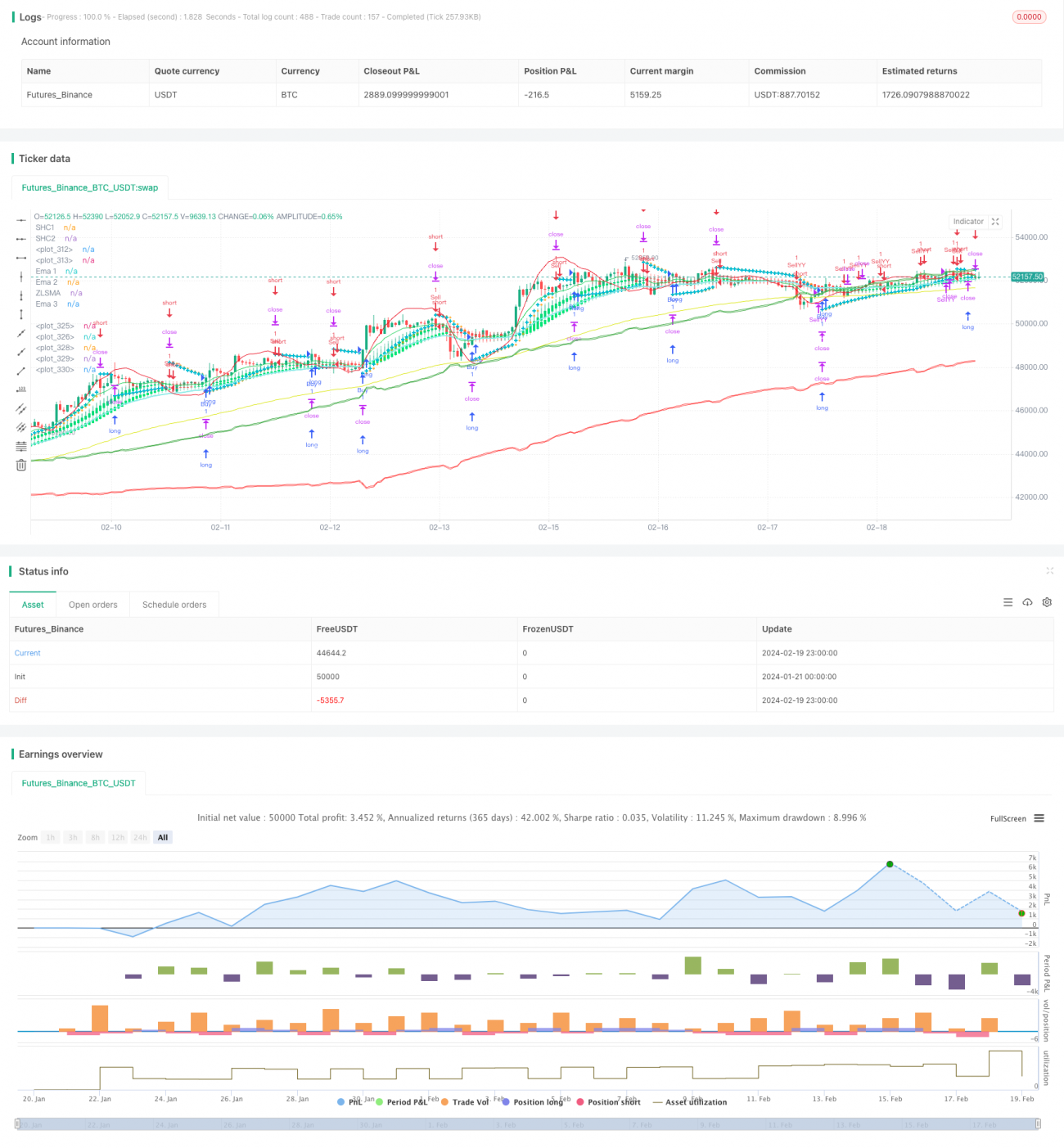

Esta estrategia combina múltiples indicadores técnicos, incluyendo el sistema Parabólico SAR, la estrategia de salida de la Teoría de Chan (缠论), la media móvil simple de retardo cero, la media móvil exponencial y la media móvil suavizada, para identificar posibles puntos de compra y venta en el gráfico.

Principio de la Estrategia

Indicadores principales

- Sistema Parabólico SAR: utilizado para determinar puntos de stop loss y posibles puntos de entrada.

- Estrategia de salida de la Teoría de Chan: utilizada para determinar la dirección de la tendencia.

- Media móvil simple de retardo cero: proporciona una media móvil con bajo retardo.

- Media móvil exponencial: sigue la tendencia y la volatilidad del precio.

- Media móvil suavizada: genera una media móvil más suave.

Señales de trading

- Cuando el sistema Parabólico SAR muestra una tendencia alcista y el precio supera la media móvil exponencial de período 99, se abre una posición larga; cuando muestra una tendencia bajista y el precio está por debajo de la media móvil exponencial de período 99, se abre una posición corta.

- Combinando las señales de la estrategia de salida de la Teoría de Chan, se confirma aún más la dirección de la tendencia.

- La media móvil suavizada, en combinación con las señales del Parabólico SAR, evita falsas rupturas.

Gestión de riesgos

- Se establecen stop loss y take profit.

- Se considera la condición de recompra para ajustar flexiblemente el tamaño de la posición.

Análisis de ventajas

La mayor ventaja de esta estrategia radica en la combinación integral de indicadores, que permite identificar eficazmente la dirección de la tendencia. El sistema Parabólico SAR determina posibles puntos de reversión; la estrategia de salida de la Teoría de Chan juzga la tendencia principal; las medias móviles filtran señales falsas. La verificación mutua de múltiples indicadores mejora significativamente la precisión de las señales.

Además, la estrategia incorpora mecanismos de stop loss y take profit para controlar el riesgo. La media móvil suavizada también se utiliza para evitar interferencias del ruido a corto plazo. Todo esto hace que la estrategia sea muy estable.

Análisis de riesgos

Debido a que depende de múltiples indicadores para el juicio, cuando estos indicadores emiten señales contradictorias, la estrategia puede enfrentar dificultades. Además, una configuración incorrecta de los parámetros también puede afectar negativamente las operaciones.

Asimismo, el trading basado en análisis técnico conlleva riesgos inherentes y no puede evitar pérdidas por completo. Se requiere operar con precaución y evitar seguir ciegamente las señales.

Direcciones de optimización

- Probar y optimizar los parámetros de los indicadores para encontrar la mejor combinación.

- Incorporar algoritmos de aprendizaje automático, utilizando grandes volúmenes de datos para entrenar modelos y mejorar aún más la precisión de las señales.

- Combinar indicadores de sentimiento e información de noticias para evaluar las condiciones del mercado y ajustar dinámicamente el tamaño de la posición y el stop loss.

- Optimizar la lógica de la condición de recompra para hacer la detección de señales más flexible y coherente.

Conclusión

Esta estrategia integra múltiples indicadores técnicos y utiliza su combinación para identificar señales de trading. Sus ventajas son la alta precisión de las señales y una fuerte estabilidad. Al mismo tiempo, las medidas de control de riesgos están bien implementadas. En general, es un plan de trading que vale la pena considerar. Puede mejorarse aún más mediante la optimización de parámetros, el entrenamiento de modelos y la introducción de indicadores de sentimiento.

- 1