Estrategia de equilibrio de control psicológico del trading

Resumen

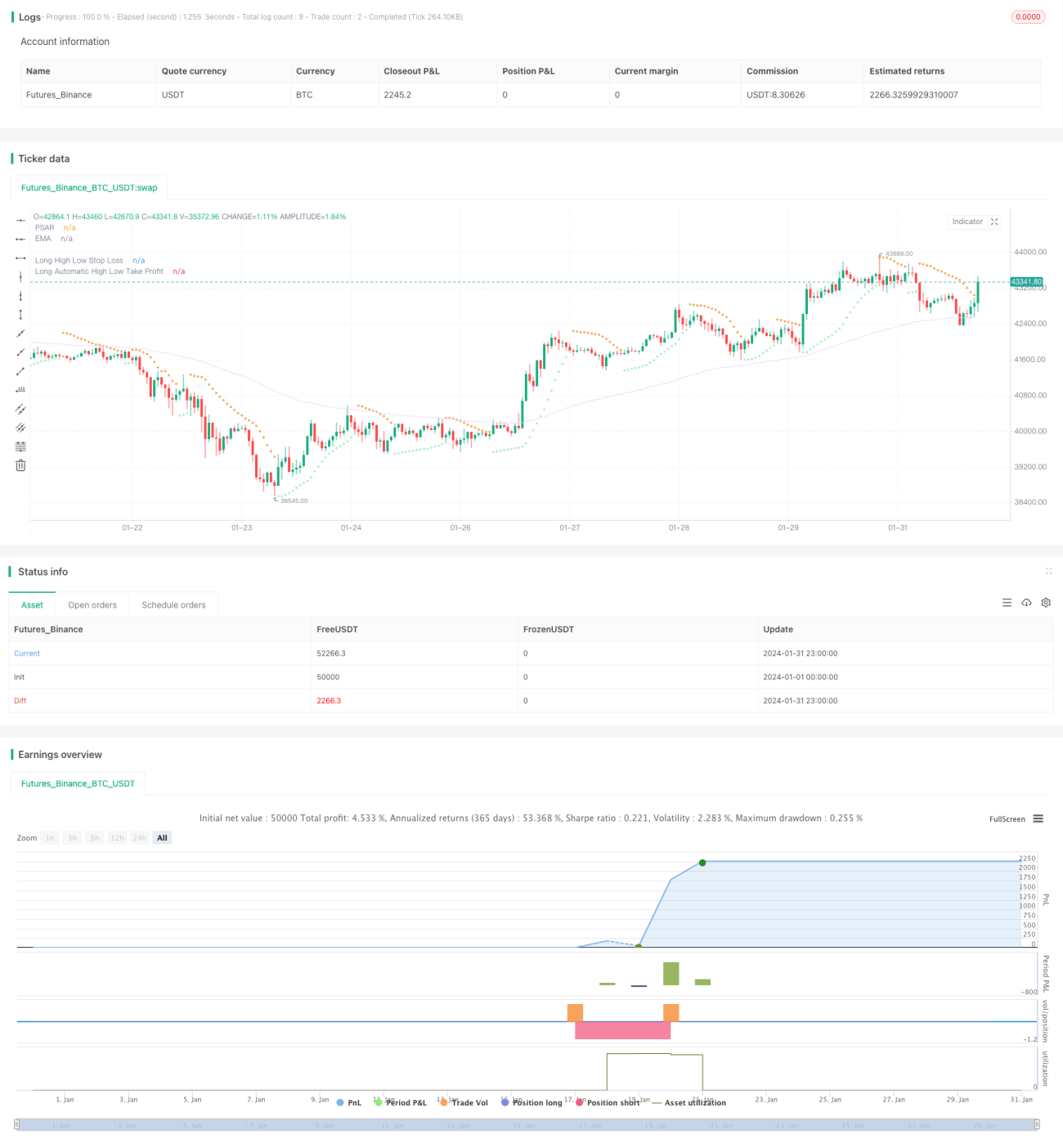

El objetivo de esta estrategia es equilibrar la psicología del trader y el rendimiento de las operaciones mediante el ajuste de diferentes parámetros, con el fin de obtener rendimientos más estables. Utiliza indicadores como medias móviles, Bandas de Bollinger, canales de Keltner para determinar la tendencia del mercado y la volatilidad, combina el indicador PSAR para detectar señales de reversión y emplea el indicador de compresión TTM (TTM Squeeze) para evaluar el momento. Las señales de trading se generan a partir de la combinación de estos indicadores. Además, la estrategia gestiona el riesgo mediante stop loss basado en máximos/mínimos y take profit basado en la relación riesgo-recompensa.

Principio de la Estrategia

La lógica principal de esta estrategia es la siguiente:

-

Determinación de la tendencia: Se utiliza la media móvil exponencial (EMA) para determinar la dirección de la tendencia del precio. Si el precio está por encima de la EMA, es una tendencia alcista; si está por debajo, es una tendencia bajista.

-

Detección de reversiones: Se emplea el PSAR para identificar puntos de reversión del precio. Un punto PSAR que aparece por encima del precio es una señal alcista; si aparece por debajo del precio, es una señal bajista.

-

Evaluación del momento: Se utiliza el indicador TTM Squeeze para medir la volatilidad y el momento del mercado. El TTM Squeeze compara la anchura de las Bandas de Bollinger con la del canal de Keltner para medir la volatilidad; una compresión indica una volatilidad extremadamente baja. Una liberación de la compresión señala un aumento de la volatilidad y un posible movimiento direccional significativo del precio.

-

Generación de señales de trading: Se genera una señal alcista cuando el precio cruza por encima de la EMA, el punto PSAR y el indicador TTM Squeeze libera la compresión. Se genera una señal bajista cuando el precio cruza por debajo de la EMA, el punto PSAR y el indicador TTM Squeeze entra en compresión.

-

Método de stop loss: Se utiliza un stop loss basado en máximos/mínimos. El punto de stop loss se determina multiplicando el precio máximo o mínimo más reciente de un período determinado por un factor configurable.

-

Método de take profit: Se utiliza un take profit automático basado en la relación riesgo-recompensa. El punto de take profit se obtiene multiplicando la distancia desde el stop loss hasta el precio actual por el parámetro de relación riesgo-recompensa configurado.

Mediante la configuración de parámetros, se puede controlar la frecuencia de las operaciones, la gestión de la posición, los puntos de stop loss y take profit, equilibrando así la psicología del trading.

Análisis de Ventajas

Esta estrategia presenta las siguientes ventajas:

- Juicio basado en múltiples indicadores, mejorando la precisión de las señales.

- Prioriza las reversiones, complementándolas con la tendencia, capturando puntos de inflexión y reduciendo la probabilidad de comprar en picos y vender en mínimos.

- El indicador TTM Squeeze puede identificar eficazmente los periodos de consolidación dentro de una tendencia, evitando operaciones ineficaces durante dichos periodos.

- El stop loss basado en máximos/mínimos es simple y práctico, y la distancia del stop loss se puede ajustar según el mercado.

- El método de take profit basado en la relación riesgo-recompensa cuantifica la relación entre ganancias y pérdidas, facilitando su ajuste.

- Los diversos parámetros son flexibles y se pueden ajustar según la tolerancia al riesgo personal.

Análisis de Riesgos

Esta estrategia también conlleva los siguientes riesgos:

- La combinación de múltiples indicadores, aunque mejora la precisión de las señales, también aumenta la posibilidad de perderse puntos de entrada.

- Al priorizar las reversiones, la estrategia puede tener un rendimiento deficiente en mercados con tendencias fuertes.

- El stop loss basado en máximos/mínimos a veces puede ser superado, sin poder evitar completamente el riesgo.

- El take profit basado en la relación riesgo-recompensa puede fallar debido a saltos de precio o ajustes del mercado.

- Una configuración inadecuada de los parámetros puede provocar pérdidas o stops frecuentes.

Direcciones de Optimización

Esta estrategia se puede optimizar en los siguientes aspectos:

- Añadir o ajustar el peso de los indicadores para hacer las señales más precisas.

- Optimizar los parámetros de los indicadores de reversión y tendencia para aumentar la probabilidad de obtener ganancias.

- Optimizar los parámetros del stop loss basado en máximos/mínimos para que el stop loss sea más razonable.

- Probar diferentes ratios de riesgo-recompensa para obtener los mejores resultados.

- Ajustar el parámetro de tamaño de la posición para reducir el impacto de una pérdida individual.

Conclusión

En general, esta estrategia, mediante el juicio combinado de indicadores y el ajuste de parámetros, puede equilibrar eficazmente la psicología del trading y obtener rentabilidades positivas estables. Aunque todavía tiene margen de mejora, ya posee valor para su aplicación en operaciones reales. A través de la retroalimentación del mercado y el ajuste fino de los parámetros, esta estrategia tiene el potencial de convertirse en una herramienta eficaz para controlar la psicología del trading y lograr beneficios estables a largo plazo.

- 1