Estrategia de trading de múltiples marcos temporales basada en indicadores de compresión

Resumen

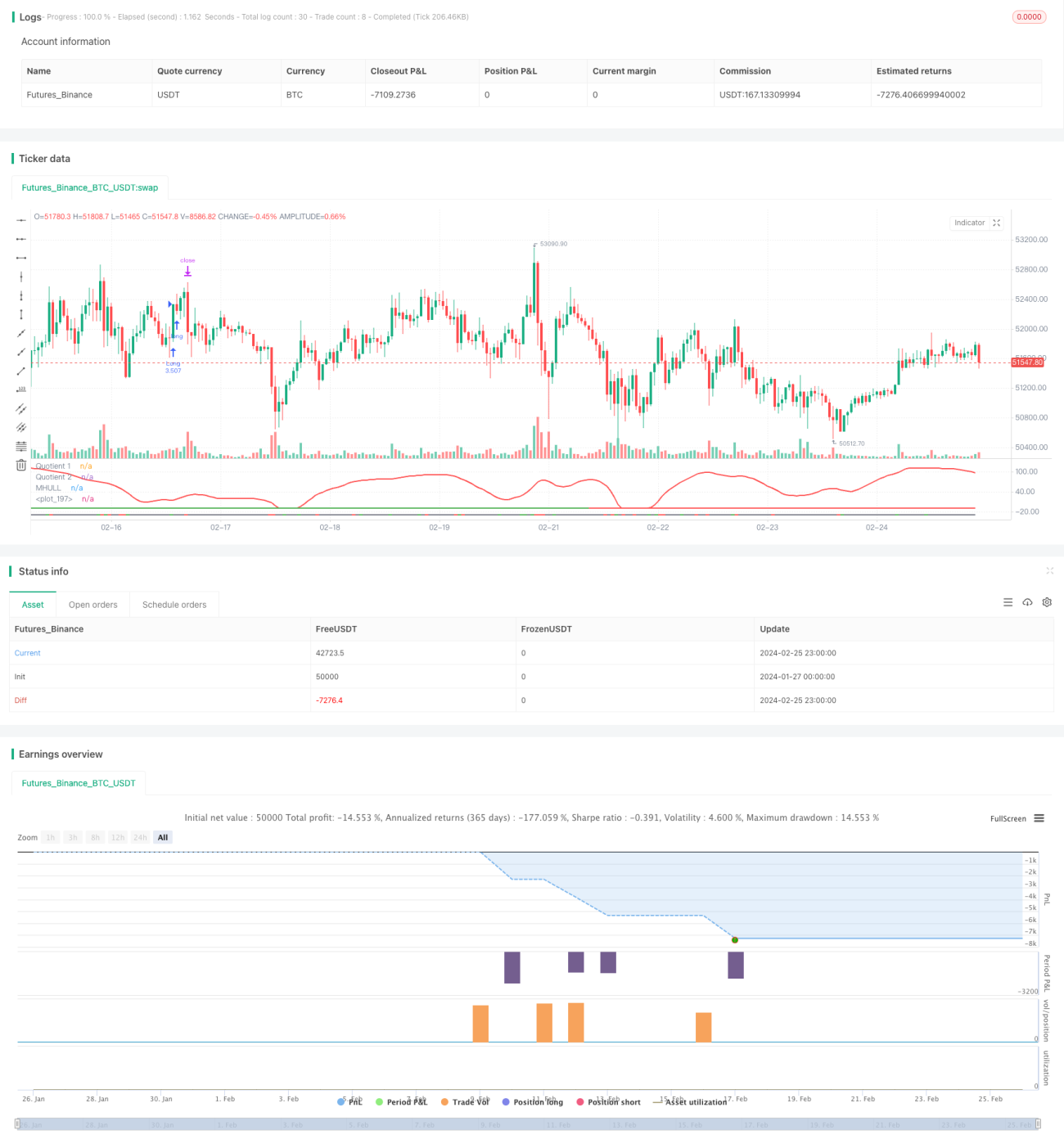

Esta estrategia combina tres indicadores: Boom Hunter, Hull Suite y Volatility Oscillator para implementar una estrategia cuantitativa de seguimiento de tendencias y trading de rupturas en múltiples marcos temporales. Es adecuada para activos digitales como Bitcoin, que presentan alta volatilidad y movimientos de precios repentinos.

Principios

La lógica central de la estrategia se basa en los siguientes tres indicadores:

-

Boom Hunter: Un oscilador que utiliza la técnica de compresión de indicadores. Genera señales de compra y venta mediante el cruce de dos indicadores (Quotient1 y Quotient2).

-

Hull Suite: Un conjunto de indicadores de medias móviles suavizadas que identifica la dirección de la tendencia mediante la relación entre la banda central y las bandas superior e inferior.

-

Volatility Oscillator: Un oscilador que cuantifica la información de la volatilidad de los precios.

La lógica de entrada de la estrategia es la siguiente: cuando los dos indicadores Quotient de Boom Hunter se cruzan al alza o a la baja, al mismo tiempo el precio debe superar la banda central de Hull y divergir con respecto a la banda superior o inferior, mientras que el indicador de volatilidad se encuentra en zona de sobrecompra o sobreventa. Esto ayuda a filtrar señales falsas de ruptura y mejora la precisión de la entrada.

El stop loss se establece buscando el valle mínimo o el pico máximo dentro de un período determinado (por defecto 20 velas). La ganancia se obtiene multiplicando el porcentaje de stop loss por la relación de take profit configurada (por defecto 3 veces). La posición se calcula en función del porcentaje del capital total de la cuenta (por defecto 3%) y la amplitud del stop loss del activo específico.

Ventajas

- Extrae las principales señales de trading de los precios mediante la técnica de compresión de indicadores, mejorando la probabilidad de obtener ganancias.

- Combinación de múltiples indicadores para verificar, evitando rupturas falsas y juzgando con precisión la dirección de la tendencia.

- Establecimiento dinámico de stop loss y take profit, logrando un seguimiento de tendencia con riesgo controlable.

- Utiliza un indicador de volatilidad para garantizar operaciones en entornos de alta volatilidad.

- Análisis en múltiples marcos temporales, mejorando la estabilidad de la estrategia.

Riesgos

- El indicador Boom Hunter puede presentar distorsión por compresión, generando señales erróneas.

- La banda central de Hull Suite tiene retraso, lo que impide seguir los cambios de precio de manera oportuna.

- Cuando la volatilidad disminuye, se pueden perder oportunidades de trading o provocar liquidaciones con pérdidas.

Soluciones:

- Ajustar los parámetros del indicador de compresión para equilibrar la sensibilidad del indicador.

- Probar el uso de medias móviles exponenciales como EHMA para reemplazar la banda central.

- Agregar otros indicadores de juicio para evitar la desinformación de la volatilidad.

Optimización

Esta estrategia se puede optimizar en los siguientes aspectos:

-

Optimización de parámetros: Modificar parámetros del indicador, como la longitud del período y el coeficiente de compresión, para obtener la mejor combinación de parámetros.

-

Optimización del marco temporal: Probar diferentes períodos de tiempo (1 minuto, 5 minutos, 30 minutos, etc.) para encontrar el marco de trading más adecuado.

-

Optimización de la posición: Cambiar el tamaño y la proporción de la posición en cada operación para encontrar la mejor utilización del capital.

-

Optimización del stop loss: Ajustar la posición del stop loss según diferentes pares de trading para lograr la mejor relación riesgo-recompensa.

-

Optimización de condiciones: Agregar o reducir condiciones de filtro del indicador para obtener un momento de entrada más preciso.

Conclusión

Esta estrategia combina los tres indicadores: Boom Hunter, Hull Suite y Volatility Oscillator, logrando un seguimiento de tendencia en múltiples marcos temporales. Es capaz de identificar eficazmente los movimientos repentinos de precios y es adecuada para activos digitales con alta volatilidad. La estrategia tiene un riesgo controlable y, mediante la optimización de parámetros, condiciones de filtro y stop loss, posee una fuerte practicidad y escalabilidad.

- 1