Estrategia de seguimiento de tendencia con triple confirmación

Resumen

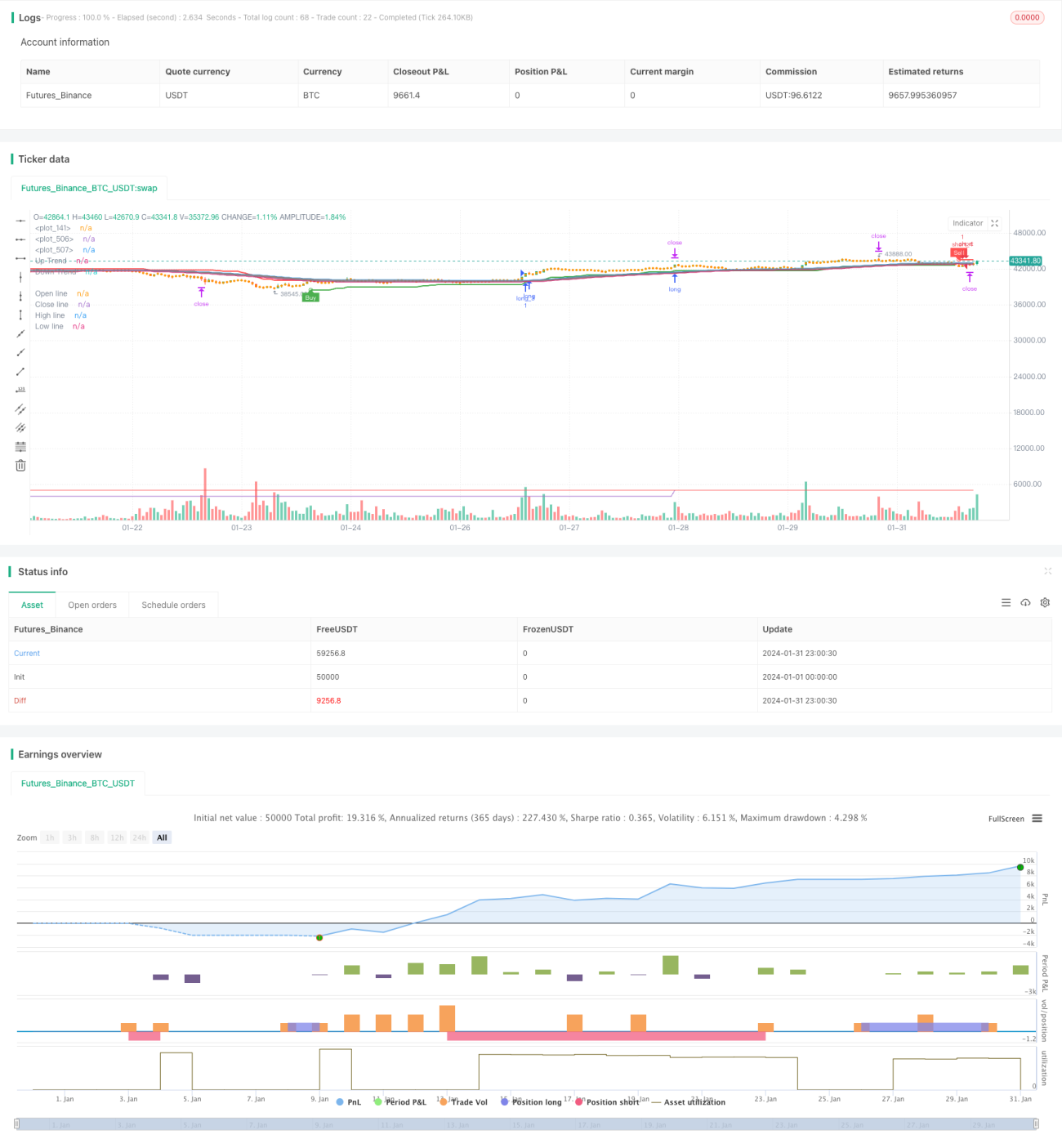

La estrategia de seguimiento de tendencia con triple confirmación combina señales de tres indicadores principales (media móvil, línea de la memoria emocional y supertendencia) para lograr una alta probabilidad de capturar tendencias. Cuando los tres indicadores emiten simultáneamente una señal de compra o venta, la estrategia ingresa oportunamente y sigue la tendencia; cuando la tendencia se revierte, la estrategia cierra la posición rápidamente y toma una posición corta.

Principio de la estrategia

Media móvil para determinar la tendencia principal

La estrategia utiliza una media móvil de período 52 para determinar la dirección de la tendencia principal. Cuando el precio cruza por encima de la media móvil, se considera una tendencia alcista; cuando el precio cruza por debajo, se considera una tendencia bajista.

Línea de la memoria emocional para identificar retrocesos secundarios

La estrategia también emplea la línea de la memoria emocional (línea del olvido) para identificar retrocesos secundarios a corto plazo. Su cálculo es similar al de la media móvil, pero reemplaza el precio de cierre por el precio de apertura, lo que permite reflejar más rápidamente las reversiones de precio. Cuando el precio cruza por encima de la línea de la memoria emocional descendente, indica una señal de estabilización y rebote a corto plazo; cuando cruza por debajo de la línea ascendente, indica una señal de caída temporal.

Supertendencia para determinar puntos de reversión

La estrategia también combina el indicador de supertendencia para identificar puntos clave de reversión. Este indicador, basado en el ATR y los datos de precio, ajusta dinámicamente los canales superior e inferior para determinar el momento de la reversión.

Filtro de triple confirmación de señales

Cuando los tres indicadores (media móvil, línea de la memoria emocional y supertendencia) emiten simultáneamente una señal de compra, la estrategia abre una posición larga; cuando los tres emiten señal de venta, abre una posición corta. Esta triple confirmación filtra eficazmente las señales falsas y aumenta la probabilidad de entrada.

Análisis de ventajas

Juicio multidimensional, alta probabilidad

La estrategia combina tres indicadores que evalúan la tendencia y los puntos clave desde diferentes dimensiones, garantizando entradas de alta probabilidad.

Reacción rápida, seguimiento en tiempo real

La inclusión de la línea de la memoria emocional permite una rápida reacción ante retrocesos a corto plazo; el indicador de supertendencia con canales adaptativos basados en ATR sigue los cambios de precio en tiempo real.

Take profit y stop loss automáticos, control efectivo del riesgo

La estrategia incorpora lógica automática de take profit y stop loss, ajustando dinámicamente los niveles según el ATR, controlando eficazmente las pérdidas por operación.

Riesgos y soluciones

Riesgo de alta frecuencia de operaciones

Debido a la frecuencia de las señales, se puede generar un exceso de operaciones. Se recomienda aumentar el período de la media móvil para reducir la frecuencia.

Riesgo de incertidumbre en las reversiones

La efectividad de la línea de la memoria emocional y la supertendencia para identificar reversiones no es absoluta, pudiendo haber falsas señales. Se pueden agregar filtros adicionales en los parámetros de los indicadores para asegurar señales de reversión de mayor probabilidad.

Riesgo de pérdidas en mercados laterales

En mercados laterales, los cruces repetidos provocan aperturas y cierres frecuentes, generando pérdidas. Se puede identificar este tipo de mercado y pausar la estrategia durante ese período.

Direcciones de optimización

Incorporar indicadores de volatilidad

Se puede considerar agregar indicadores de volatilidad como las Bandas de Bollinger. Cuando el precio se acerca a los bordes superior o inferior de las bandas, evitar nuevas entradas para reducir el riesgo en mercados laterales.

Agregar filtros de entrada

Se pueden probar otros indicadores auxiliares como KDJ, MACD, etc., para que la entrada solo se realice cuando también emitan señales. Esto filtra más señales falsas y reduce operaciones innecesarias.

Optimizar la estrategia de take profit y stop loss

Se puede mejorar la estrategia de take profit y stop loss, por ejemplo mediante trailing stop, trailing stop exponencial, o take profit parcial escalonado, para obtener ganancias más estables y mayores.

Conclusión

La estrategia de seguimiento de tendencia con triple confirmación aprovecha las fortalezas de la media móvil, la línea de la memoria emocional y la supertendencia para lograr una alta probabilidad de identificar y capturar tendencias. Además, incorpora mecanismos automáticos de take profit y stop loss para controlar las pérdidas por operación. Para mejorar su practicidad, se puede optimizar añadiendo indicadores auxiliares como filtros de entrada y mejorando la estrategia de take profit y stop loss.

- 1