Estrategia Kuberan: Estrategia de convergencia para el control del mercado

Resumen de la estrategia

La estrategia Kuberan es una poderosa estrategia de trading escrita por Kathir. Combina múltiples técnicas de análisis para formar un enfoque de trading único y robusto. Nombrada en honor a Kuberan, el dios de la riqueza, simboliza su objetivo de enriquecer las carteras de los traders.

Kuberan no es solo una estrategia, sino un sistema de trading integral. Integra análisis de tendencias, indicadores de momentum e indicadores de volumen para identificar oportunidades de trading de alta probabilidad. Al aprovechar la sinergia de estos elementos, Kuberan proporciona señales claras de entrada y salida, adecuadas para traders de todos los niveles.

Principio de la estrategia

El núcleo de la estrategia Kuberan es el principio de confluencia de múltiples indicadores. Utiliza una combinación única de indicadores que trabajan juntos para reducir el ruido y las señales falsas. Específicamente, la estrategia emplea los siguientes componentes clave:

- Determinación de la dirección de la tendencia: Compara el precio actual con los niveles de soporte y resistencia para determinar la dirección de la tendencia.

- Niveles de soporte y resistencia: Identifica niveles clave de soporte y resistencia mediante el indicador Zigzag y puntos pivote.

- Detección de divergencias: Compara la acción del precio con indicadores de momentum para detectar divergencias, señalando posibles reversiones de tendencia.

- Adaptación a la volatilidad: Ajusta dinámicamente los niveles de stop-loss utilizando el indicador ATR para adaptarse a diferentes condiciones de volatilidad del mercado.

- Reconocimiento de patrones de velas: Utiliza combinaciones específicas de velas para confirmar tendencias y señales de reversión.

Al considerar todos estos factores de manera integral, la estrategia Kuberan puede adaptarse de forma dinámica a diversas condiciones del mercado, capturando oportunidades de trading de alta probabilidad.

Ventajas de la estrategia

- Confluencia de múltiples indicadores: La estrategia Kuberan aprovecha la sinergia de varios indicadores, mejorando significativamente la fiabilidad de las señales y reduciendo la interferencia del ruido.

- Alta adaptabilidad: Mediante el ajuste dinámico de parámetros, la estrategia puede adaptarse a entornos de mercado cambiantes, siendo difícil que quede obsoleta.

- Señales claras: Kuberan proporciona señales de entrada y salida nítidas, simplificando el proceso de toma de decisiones en el trading.

- Robustez en backtesting: La estrategia ha sido sometida a rigurosas pruebas históricas, demostrando un rendimiento sólido en diversas condiciones del mercado.

- Amplia aplicabilidad: Kuberan es adecuada para múltiples mercados e instrumentos, sin limitarse a activos específicos.

Riesgos de la estrategia

- Sensibilidad a los parámetros: El rendimiento de la estrategia Kuberan es sensible a la elección de parámetros; una selección inadecuada puede degradar el rendimiento.

- Eventos imprevistos: La estrategia se basa principalmente en señales técnicas, por lo que su capacidad para responder a eventos fundamentales repentinos es limitada.

- Riesgo de sobreajuste: Si se consideran demasiados datos históricos durante la optimización de parámetros, la estrategia podría ajustarse excesivamente al pasado, reduciendo su adaptabilidad a condiciones futuras.

- Riesgo de apalancamiento: El uso de un apalancamiento excesivo puede conllevar el riesgo de liquidación en caso de retrocesos significativos.

Para mitigar estos riesgos, se pueden implementar medidas de control adecuadas, como ajustar periódicamente los parámetros, establecer stop-loss razonables, controlar el apalancamiento de forma moderada y mantenerse atento a los cambios fundamentales.

Direcciones de optimización

- Optimización mediante aprendizaje automático: Se pueden introducir algoritmos de aprendizaje automático para optimizar dinámicamente los parámetros de la estrategia, mejorando su adaptabilidad.

- Incorporación de factores fundamentales: Considerar la integración del análisis fundamental en las decisiones de trading para afrontar situaciones en las que las señales técnicas fallen.

- Gestión de carteras: A nivel de gestión de capital, se puede incluir la estrategia Kuberan en una cartera, formando una cobertura efectiva con otras estrategias.

- Optimización por segmentos de mercado: Personalizar y optimizar los parámetros de la estrategia según las características específicas de diferentes instrumentos y mercados.

- Adaptación a alta frecuencia: Transformar la estrategia en una versión de trading de alta frecuencia para capturar más oportunidades de trading a corto plazo.

Conclusión

Kuberan es una estrategia de trading potente, segura y fiable. Combina hábilmente múltiples métodos de análisis técnico mediante el principio de confluencia de indicadores, destacando en la captura de tendencias y en la identificación de puntos de inflexión. Aunque ninguna estrategia está exenta de riesgos, Kuberan ha demostrado su solidez en pruebas retrospectivas. Con una adecuada gestión de riesgos y medidas de optimización, se cree que esta estrategia puede ayudar a los traders a tomar ventaja en el juego del mercado, impulsando el crecimiento estable a largo plazo de sus carteras.

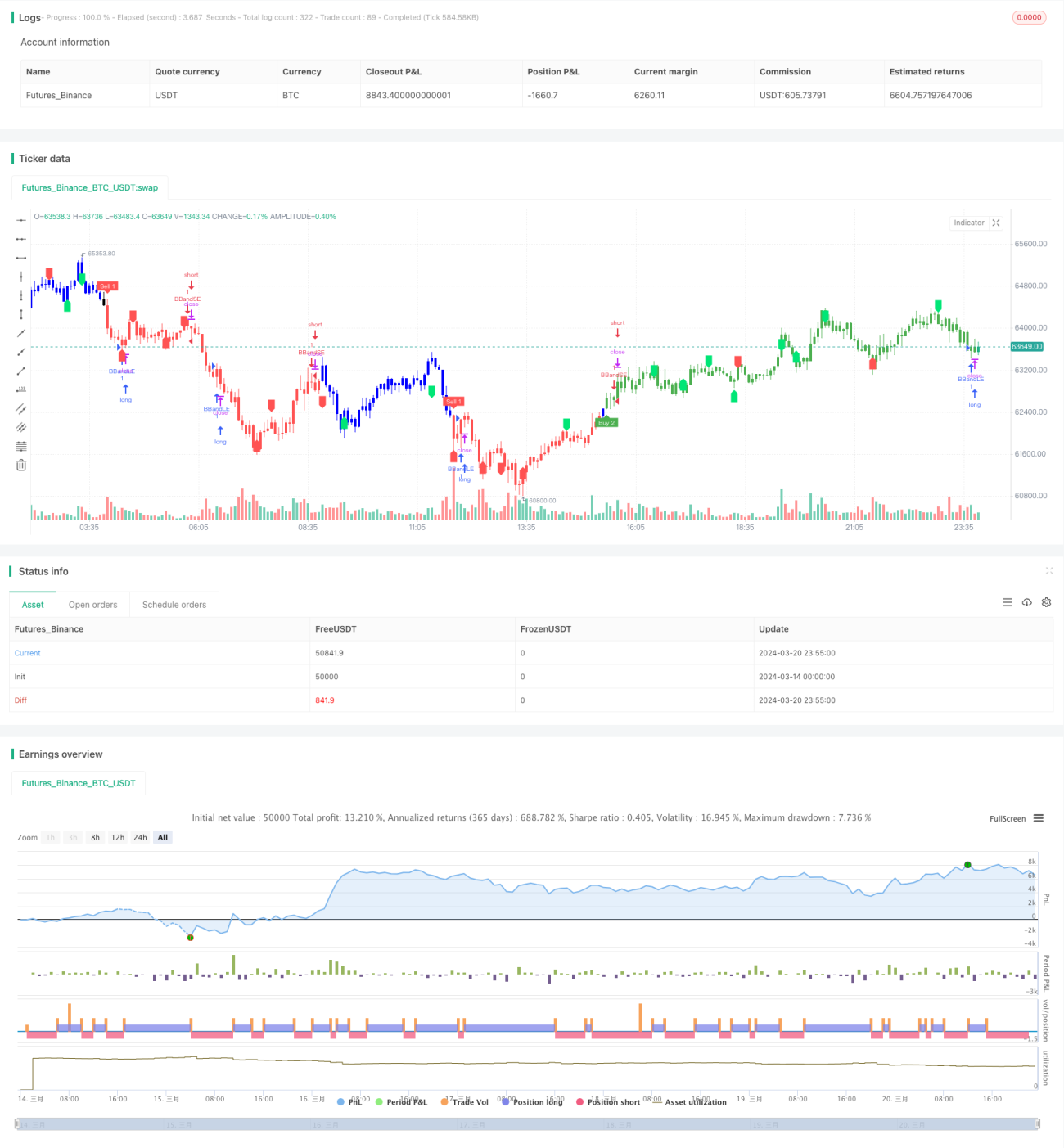

/*backtest

start: 2024-03-14 00:00:00

end: 2024-03-21 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue- 1