Estrategia de trading de momento con filtro de doble rango

Resumen

Esta estrategia es una estrategia de trading de impulso basada en un filtro de rango dual. La estrategia calcula rangos suavizados de dos períodos (rápido y lento) para obtener un filtro de rango compuesto, que se utiliza para determinar la tendencia del precio actual. Cuando el precio cruza por encima o por debajo de este rango, la estrategia genera señales de compra o venta. Además, la estrategia establece cuatro niveles de take profit escalonados y un stop loss para controlar el riesgo y asegurar las ganancias.

Principio de la estrategia

- Calcular rangos suavizados de dos períodos: rápido y lento. El rango rápido utiliza un período más corto y un multiplicador menor, mientras que el rango lento usa un período más largo y un multiplicador mayor.

- Tomar el promedio de los rangos rápido y lento como filtro de rango compuesto (TRF).

- Calcular la relación entre el precio actual y el precio anterior para determinar una tendencia ascendente (upward) y descendente (downward).

- Calcular la banda superior dinámica (FUB) y la banda inferior dinámica (FLB) como referencia de la tendencia.

- Generar señales de compra y venta según la relación entre el precio de cierre y el TRF.

- Establecer cuatro niveles de take profit escalonados y un stop loss, correspondientes a diferentes porcentajes de posición y porcentajes de ganancia/pérdida.

Análisis de ventajas

- El filtro de rango dual combina ciclos rápido y lento, lo que permite adaptarse a diferentes ritmos del mercado y capturar más oportunidades de trading.

- El diseño de bandas dinámicas superior e inferior ayuda a seguir la tendencia actual y reduce las señales falsas.

- La configuración de cuatro niveles de take profit escalonados permite obtener más ganancias cuando la tendencia continúa, al mismo tiempo que asegura parte de las ganancias cuando la tendencia se revierte.

- La configuración de stop loss ayuda a controlar la pérdida máxima por operación individual, protegiendo la cuenta.

Análisis de riesgos

- Cuando el mercado se encuentra en un rango lateral o en consolidación, la estrategia puede generar muchas señales falsas, lo que lleva a operaciones frecuentes y pérdidas por comisiones.

- La configuración de take profit escalonado puede hacer que parte de las ganancias se aseguren prematuramente, impidiendo aprovechar completamente las ganancias de una tendencia.

- La configuración de stop loss puede no evitar completamente las pérdidas extremas causadas por eventos de cisne negro.

Direcciones de optimización

- Se puede considerar la incorporación de más indicadores técnicos o indicadores de sentimiento del mercado como condiciones auxiliares para el juicio de tendencia, reduciendo así las señales falsas.

- Para la configuración de take profit y stop loss, se pueden ajustar dinámicamente según las diferentes condiciones del mercado y los activos negociados, mejorando la adaptabilidad de la estrategia.

- Sobre la base de las pruebas retrospectivas, se pueden optimizar aún más los parámetros, como la selección de períodos para los rangos rápido y lento, y el porcentaje de take profit y stop loss, para mejorar la estabilidad y rentabilidad de la estrategia.

Conclusión

La estrategia de trading de impulso con filtro de rango dual construye un filtro compuesto mediante rangos suavizados de ciclos rápido y lento, combinado con bandas dinámicas superior e inferior para evaluar la tendencia del precio y generar señales de compra y venta. La estrategia también establece cuatro niveles de take profit escalonados y un stop loss para controlar el riesgo y asegurar las ganancias. Esta estrategia es adecuada para mercados con tendencia, pero puede generar muchas señales falsas en mercados laterales. En el futuro, se podría considerar la incorporación de más indicadores, optimizar la configuración de take profit y stop loss, y ajustar los parámetros dinámicamente para mejorar la adaptabilidad y estabilidad de la estrategia.

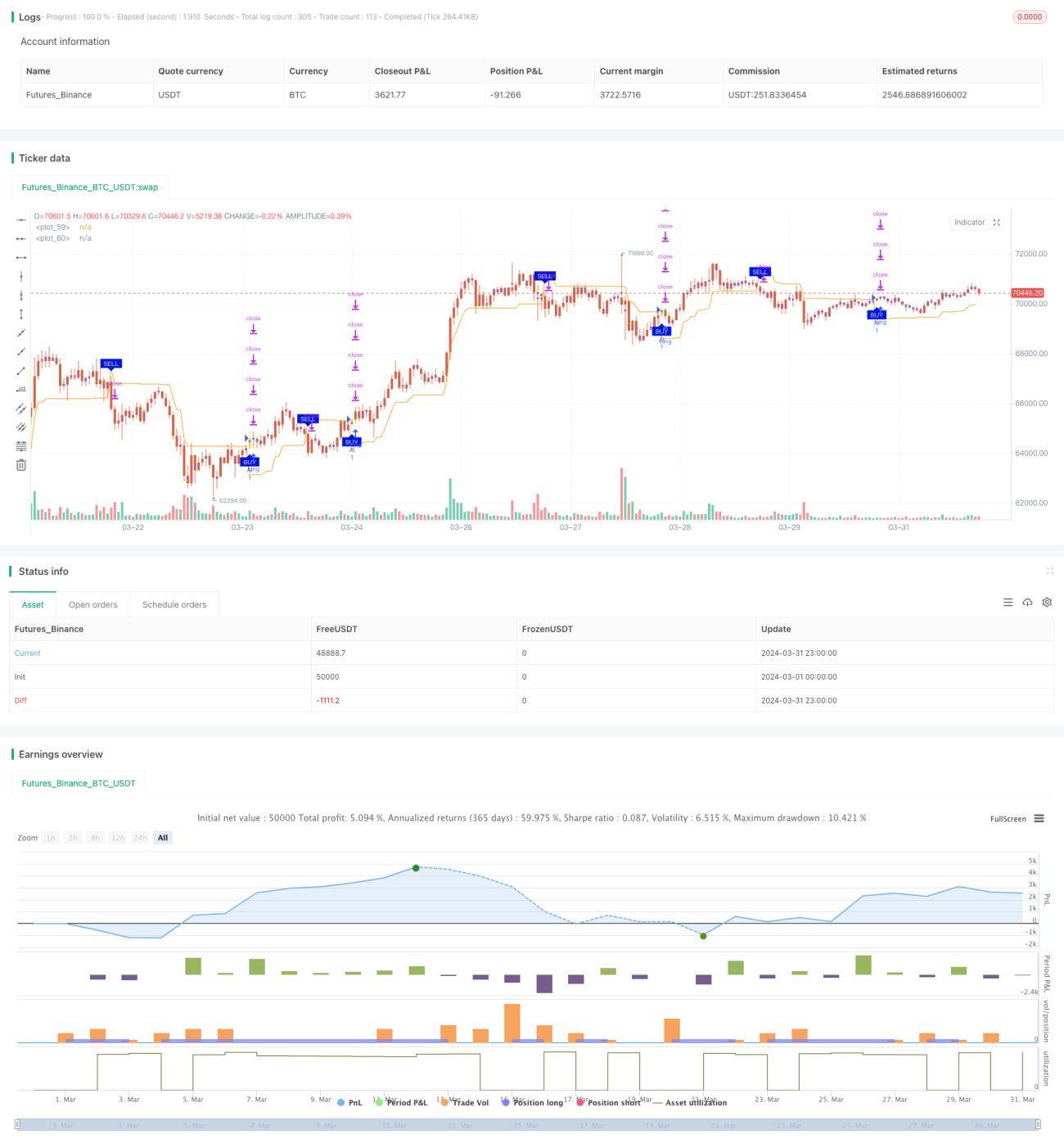

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=5

strategy(title='2"Twin Range Filter', overlay=true)

strat_dir_input = input.string(title='İşlem Yönü', defval='Alis', options=['Alis', 'Satis', 'Tum'])- 1