Transformador de Backtesting de Squeeze v2.0

Resumen

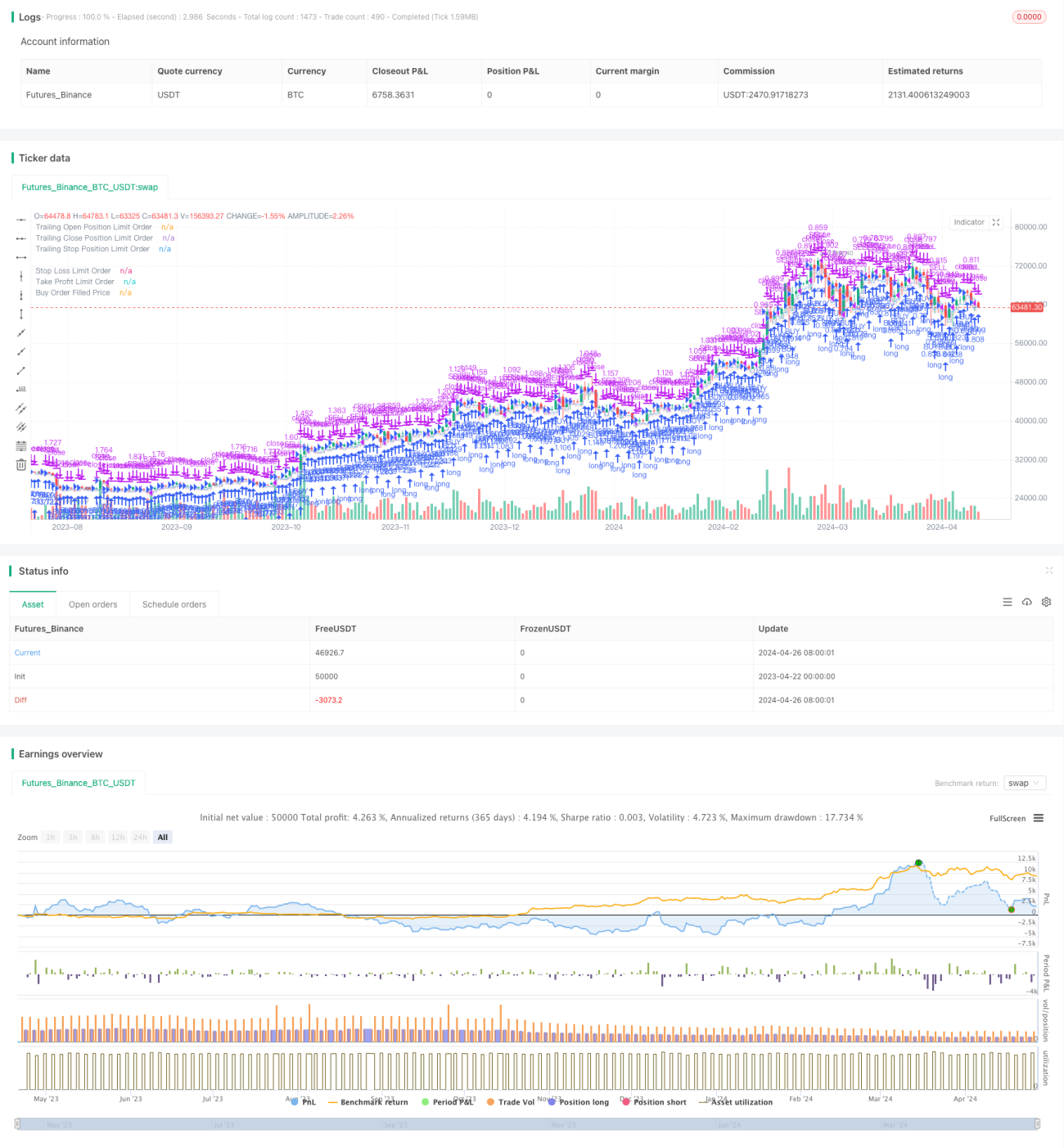

Transformers de Backtesting de Squeeze v2.0 es un sistema de trading cuantitativo basado en una estrategia de tipo squeeze. Permite realizar backtesting de la estrategia en un rango de tiempo específico mediante la configuración de parámetros como porcentajes de entrada, stop loss y take profit, así como el tiempo máximo de mantenimiento de posición. La estrategia admite operaciones en múltiples direcciones, pudiendo configurar de forma flexible la dirección de trading como larga o corta. Además, ofrece opciones variadas para el período de backtesting, lo que permite seleccionar cómodamente un rango de tiempo fijo o un tiempo máximo de backtesting.

Principio de la Estrategia

- Primero, según los parámetros del período de backtesting establecidos por el usuario, se determinan la hora de inicio y la hora de finalización del backtesting.

- Durante el período de backtesting, si no hay ninguna posición abierta y el precio alcanza el precio de entrada (calculado según el porcentaje de apertura), se abre una posición y se establecen simultáneamente los precios de stop loss y take profit (calculados según los porcentajes de stop loss y take profit).

- Si ya hay una posición abierta, se cancelan las órdenes anteriores de take profit y stop loss, y se establecen nuevos precios de take profit y stop loss (calculados según el precio promedio actual de la posición).

- Si se ha configurado un tiempo máximo de mantenimiento de posición, cuando el tiempo de tenencia alcanza el máximo, se fuerza el cierre de la posición.

- La estrategia admite operaciones tanto en dirección larga como corta.

Ventajas de la Estrategia

- Configuración flexible de parámetros, que se pueden ajustar según las diferentes condiciones del mercado y necesidades de trading.

- Soporte para operaciones en múltiples direcciones, lo que permite obtener ganancias en diferentes condiciones del mercado.

- Ofrece opciones variadas para el período de backtesting, facilitando el backtesting y análisis con datos históricos.

- La configuración de stop loss y take profit permite controlar eficazmente el riesgo y mejorar la eficiencia del uso del capital.

- El tiempo máximo de mantenimiento de posición evita el riesgo de mercado por mantener posiciones demasiado tiempo.

Riesgos de la Estrategia

- La configuración del precio de entrada, del stop loss y del take profit tiene un gran impacto en el rendimiento de la estrategia; una configuración inadecuada de los parámetros puede provocar pérdidas.

- En condiciones de alta volatilidad del mercado, es posible que se active el stop loss inmediatamente después de abrir una posición, lo que generaría pérdidas.

- Si se fuerza el cierre de la posición al alcanzar el tiempo máximo de mantenimiento, se podría perder la oportunidad de obtener ganancias posteriores.

- La estrategia puede tener un rendimiento deficiente en condiciones de mercado especiales (como mercados laterales).

Direcciones de Optimización de la Estrategia

- Se puede considerar la introducción de más indicadores técnicos o indicadores de sentimiento del mercado para optimizar las condiciones de entrada, stop loss y take profit, mejorando la estabilidad y rentabilidad de la estrategia.

- En cuanto a la configuración del tiempo máximo de mantenimiento de posición, se puede ajustar dinámicamente según la volatilidad del mercado y el estado de ganancias/pérdidas de la posición, evitando el costo de oportunidad que podría generar un cierre por tiempo fijo.

- Dadas las características de los mercados laterales, se puede agregar lógica como la ruptura de rangos de consolidación o la confirmación de cambios de tendencia, reduciendo los costos ocasionados por operaciones frecuentes.

- Considerar la incorporación de estrategias de gestión de posición y gestión de capital para controlar la exposición al riesgo en cada operación, mejorando la eficiencia y estabilidad en el uso del capital.

Conclusión

Transformers de Backtesting de Squeeze v2.0 es un sistema de trading cuantitativo basado en una estrategia de tipo squeeze. Gracias a su configuración flexible de parámetros y al soporte para operaciones en múltiples direcciones, permite realizar transacciones en diferentes entornos de mercado. Además, las abundantes opciones de período de backtesting y la configuración de take profit y stop loss ayudan a los usuarios a realizar análisis de datos históricos y control de riesgos. Sin embargo, el rendimiento de la estrategia se ve muy influenciado por la configuración de los parámetros, por lo que es necesario optimizarla y mejorarla según las características del mercado y las necesidades de trading, con el fin de mejorar su solidez y rentabilidad. En el futuro, se podría considerar la incorporación de más indicadores técnicos, el ajuste dinámico del tiempo máximo de mantenimiento de posición, la optimización de la estrategia para mercados laterales y el fortalecimiento de la gestión de posición y de capital.

/*backtest

start: 2023-04-22 00:00:00

end: 2024-04-27 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Squeeze Backtest by Shaqi v2.0", overlay=true, pyramiding=0, currency="USD", process_orders_on_close=true, commission_type=strategy.commission.percent, commission_value=0.075, default_qty_type=strategy.percent_of_equity, default_qty_value=100, initial_capital=100, backtest_fill_limits_assumption=0)

R0 = "6 Hours"- 1