Estrategia de posiciones nocturnas basada en el indicador EMA para tendencias alcistas y bajistas en múltiples mercados

Esta estrategia es una estrategia de posiciones nocturnas entre mercados basada en el indicador técnico EMA, diseñada para capturar oportunidades de trading antes del cierre del mercado y después de la apertura del día siguiente. Mediante un control de tiempo preciso y un filtrado de indicadores técnicos, la estrategia logra operaciones inteligentes en diferentes entornos de mercado.

Resumen de la estrategia

La estrategia obtiene ganancias entrando en el mercado en un momento específico antes del cierre del mercado y saliendo en un momento específico después de la apertura del día siguiente. Combinado con el indicador EMA como confirmación de la tendencia, busca oportunidades de trading en múltiples mercados globales. La estrategia también integra funciones de trading automatizado, permitiendo operaciones sin supervisión.

Principio de la estrategia

- Control de tiempo: Según los horarios de negociación de diferentes mercados, se ingresa en un momento fijo antes del cierre y se sale en un momento fijo después de la apertura.

- Filtro EMA: Utiliza el indicador EMA opcional para verificar las señales de entrada.

- Selección de mercado: Admite la adaptación automática a los horarios de negociación de los mercados de EE. UU., Asia y Europa.

- Protección de fin de semana: Fuerza el cierre de posiciones antes del cierre del viernes para evitar el riesgo de mantener posiciones durante el fin de semana.

Ventajas de la estrategia

- Adaptabilidad a múltiples mercados: Permite ajustar los horarios de negociación de manera flexible según las características de cada mercado.

- Control de riesgo completo: Incluye un mecanismo de protección de cierre de posiciones de fin de semana.

- Alto nivel de automatización: Admite la conexión con interfaces de trading automático.

- Parámetros ajustables: Los horarios de negociación y los parámetros de los indicadores técnicos se pueden personalizar.

- Consideración de costos de negociación: Incluye configuraciones de comisiones y deslizamiento.

Riesgos de la estrategia

- Riesgo de volatilidad del mercado: Mantener posiciones nocturnas puede enfrentar el riesgo de brechas de precios.

- Dependencia del tiempo: La efectividad de la estrategia se ve afectada por la elección del período de mercado.

- Limitación de indicadores técnicos: Un solo indicador EMA puede presentar retraso.

Recomendación: Establecer límites de stop-loss y agregar más validación de indicadores técnicos.

Direcciones de optimización de la estrategia

- Agregar más combinaciones de indicadores técnicos.

- Introducir un mecanismo de filtrado de volatilidad.

- Optimizar la selección de tiempos de entrada y salida.

- Incorporar funciones de ajuste de parámetros adaptativos.

- Reforzar el módulo de control de riesgos.

Conclusión

Esta estrategia logra un sistema de trading nocturno confiable mediante un control de tiempo preciso y un filtrado de indicadores técnicos. El diseño de la estrategia considera de manera integral las necesidades prácticas, incluyendo la adaptabilidad a múltiples mercados, el control de riesgos, el trading automatizado, etc., lo que le otorga un alto valor práctico. Con una optimización y mejora continuas, se espera que esta estrategia obtenga rendimientos estables en operaciones reales.

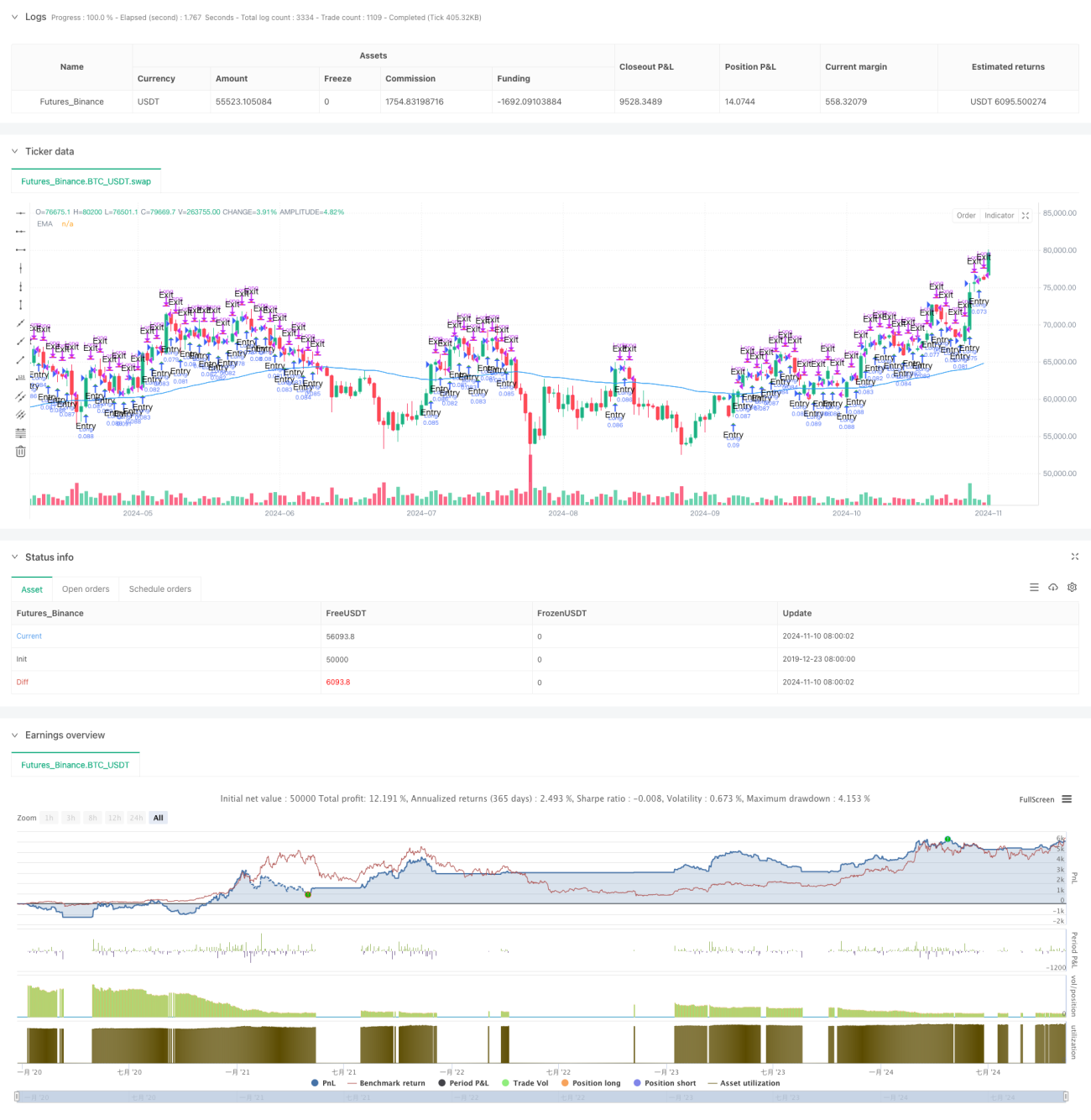

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-11 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy, titled "Overnight Market Entry Strategy with EMA Filter," is designed for entering long positions shortly before - 1