Estrategia de seguimiento de tendencias parametrizada adaptativa KNN

Resumen

Esta estrategia es un sistema de seguimiento de tendencia adaptativo y parametrizado basado en el algoritmo de aprendizaje automático K-Nearest Neighbors (KNN). La estrategia utiliza el algoritmo KNN para ajustar dinámicamente los parámetros de seguimiento de tendencia, combinando medias móviles para generar señales de trading. El sistema puede ajustar automáticamente los parámetros de la estrategia según los cambios en el entorno del mercado, mejorando su adaptabilidad y estabilidad. Esta estrategia emplea métodos de aprendizaje automático para optimizar las estrategias tradicionales de seguimiento de tendencia, representando una combinación de tecnología e innovación en el campo de la inversión cuantitativa.

Principio de la estrategia

El principio central de la estrategia consiste en utilizar el algoritmo KNN para analizar datos históricos de precios, prediciendo la evolución del precio mediante el cálculo de la similitud entre el estado actual del mercado y los datos históricos. Los pasos específicos de implementación son:

- Definir el tamaño de la ventana de observación y el valor K, recopilando datos históricos de precios para formar vectores de características.

- Calcular la distancia euclidiana entre la serie de precios actual y los datos históricos.

- Seleccionar las K series de precios históricas más similares como muestras vecinas.

- Analizar el movimiento posterior del precio de estas K muestras vecinas.

- Combinar la media móvil y generar señales de trading basadas en el cambio promedio del precio de las muestras vecinas.

Cuando el cambio promedio del precio de las K muestras vecinas es positivo y el precio actual se encuentra por encima de la media móvil, el sistema genera una señal de compra (largo); en caso contrario, genera una señal de venta (corto).

Ventajas de la estrategia

- Alta adaptabilidad: el algoritmo KNN puede ajustar automáticamente los parámetros según los cambios en el entorno del mercado, otorgando a la estrategia una fuerte capacidad de adaptación.

- Análisis multidimensional: combina algoritmos de aprendizaje automático e indicadores técnicos, ofreciendo una perspectiva de análisis de mercado más completa.

- Control de riesgo razonable: utiliza la media móvil como confirmación auxiliar, reduciendo el impacto de señales falsas.

- Lógica de cálculo clara: el proceso de ejecución de la estrategia es transparente, facilitando su comprensión y optimización.

- Parámetros flexibles y ajustables: se pueden ajustar parámetros como el valor K y el tamaño de la ventana según diferentes entornos de mercado.

Riesgos de la estrategia

- Alta complejidad computacional: el algoritmo KNN requiere calcular grandes volúmenes de datos históricos, lo que puede afectar la eficiencia de ejecución de la estrategia.

- Sensibilidad a los parámetros: la selección del valor K y el tamaño de la ventana tiene un impacto significativo en el rendimiento de la estrategia.

- Dependencia del entorno del mercado: en condiciones de mercado altamente volátiles, el valor de referencia de la similitud histórica puede disminuir.

- Riesgo de sobreajuste: una dependencia excesiva de los datos históricos puede provocar un sobreajuste de la estrategia.

- Riesgo de retraso: debido a la necesidad de recopilar suficientes datos históricos, puede haber un retraso en las señales.

Direcciones de optimización de la estrategia

-

Optimización de la ingeniería de características:

- Agregar más indicadores técnicos como características.

- Introducir indicadores de sentimiento del mercado.

- Optimizar los métodos de normalización de características.

-

Mejora de la eficiencia del algoritmo:

- Utilizar estructuras de datos como KD-tree para optimizar la búsqueda de vecinos.

- Implementar computación paralela.

- Optimizar el almacenamiento y acceso a datos.

-

Refuerzo del control de riesgos:

- Añadir mecanismos de stop-loss y take-profit.

- Introducir filtros de volatilidad.

- Diseñar un sistema dinámico de gestión de posiciones.

-

Plan de optimización de parámetros:

- Implementar selección adaptativa del valor K.

- Ajustar dinámicamente el tamaño de la ventana de observación.

- Optimizar el período de la media móvil.

-

Mejora del mecanismo de generación de señales:

- Introducir un sistema de puntuación de intensidad de señal.

- Diseñar mecanismos de confirmación de señales.

- Optimizar los momentos de entrada y salida.

Conclusión

Esta estrategia aplica de manera innovadora el algoritmo KNN al trading de seguimiento de tendencia, optimizando las estrategias tradicionales de análisis técnico mediante métodos de aprendizaje automático. La estrategia posee una fuerte adaptabilidad y flexibilidad, permitiendo ajustar dinámicamente los parámetros según el entorno del mercado. Aunque presenta riesgos como alta complejidad computacional y sensibilidad a los parámetros, mediante una optimización razonable y medidas de control de riesgo, la estrategia sigue teniendo un buen valor de aplicación. Se recomienda a los inversores que, en la práctica, ajusten los parámetros según las características del mercado y combinen otros métodos de análisis para tomar decisiones de trading.

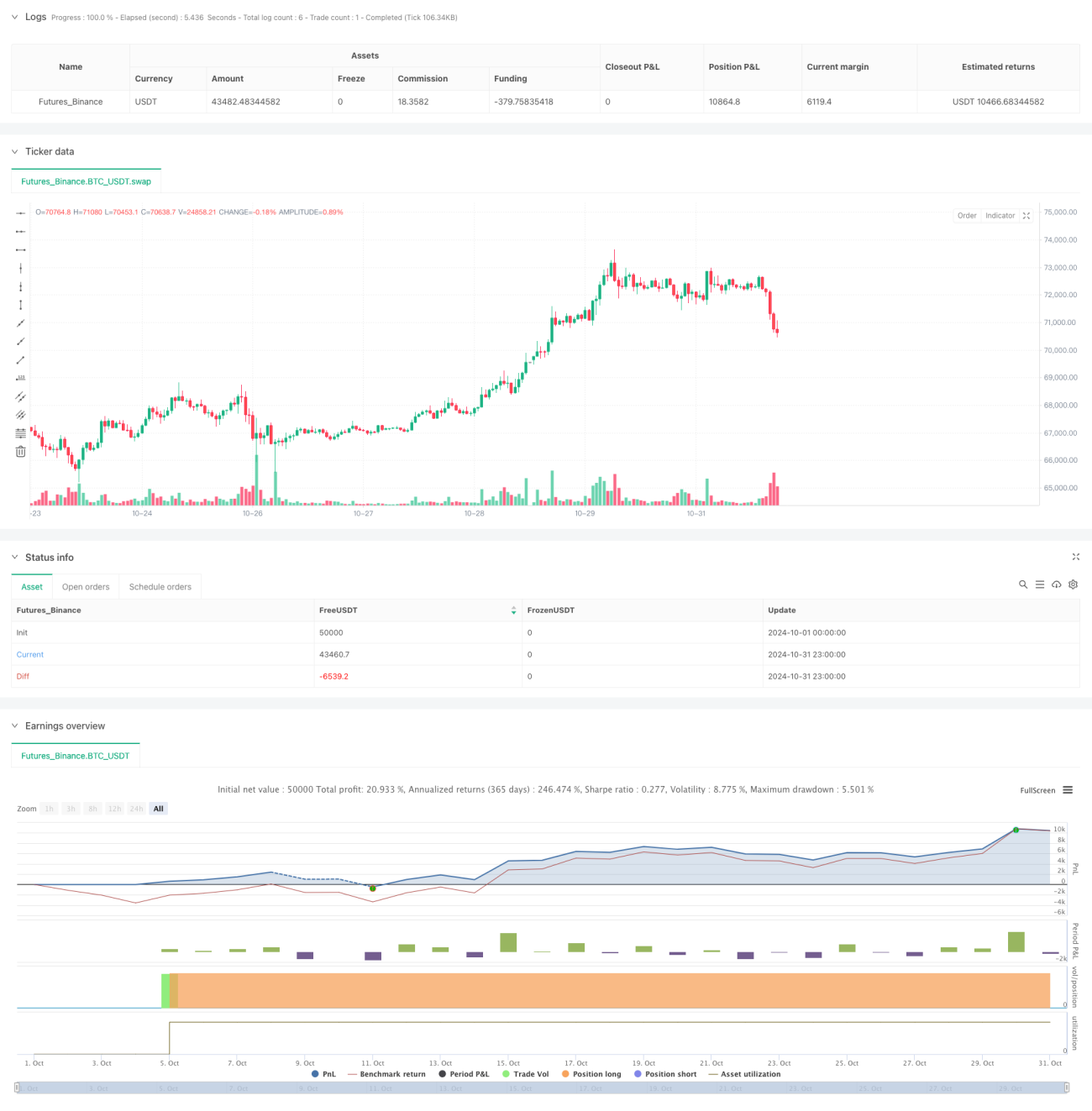

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Trend Following Strategy with KNN", overlay=true,commission_value=0.03,currency='USD', commission_type=strategy.commission.percent,default_qty_type=strategy.cash)

- 1