Estrategia avanzada de detección de brechas de valor razonable basada en gestión dinámica de riesgos y ganancias fijas

Resumen

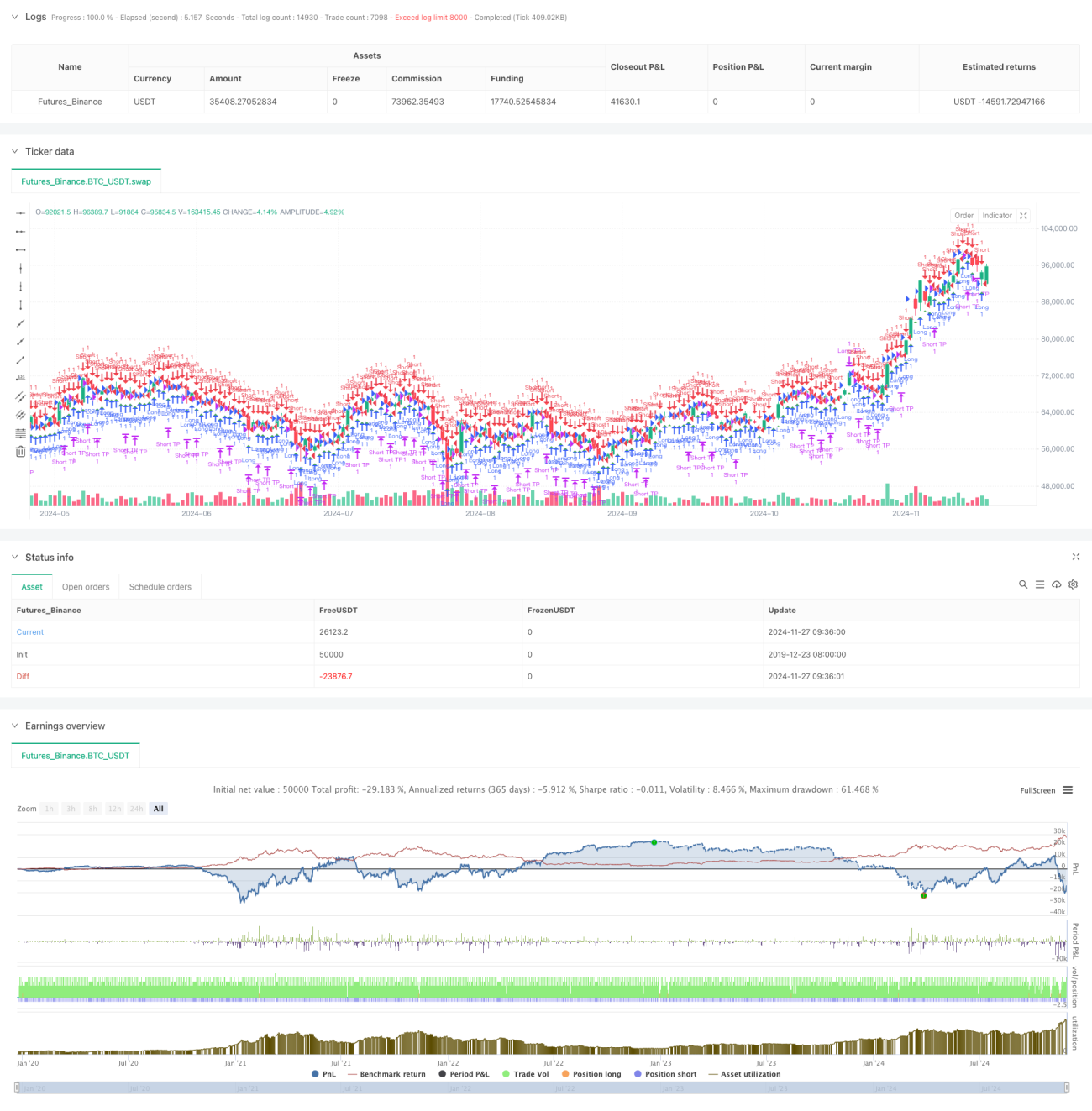

Esta estrategia de trading se basa en el Brecha de Valor Justo (FVG, por sus siglas en inglés), combinando una gestión dinámica del riesgo con un objetivo de beneficio fijo. Opera en el marco temporal de 15 minutos, identificando brechas de precios en el mercado para capturar oportunidades de trading potenciales. Según los datos de backtesting, entre noviembre de 2023 y agosto de 2024, la estrategia logró un rendimiento neto del 284,40%, completando un total de 153 operaciones, con una tasa de ganancia del 71,24% y un factor de beneficio de 2,422.

Principio de la estrategia

El núcleo de la estrategia consiste en identificar brechas de valor justo mediante el monitoreo de la relación de precios entre tres velas consecutivas. Específicamente:

- Condición para la formación de un FVG alcista: cuando el precio más alto de la vela anterior es inferior al precio más bajo de las dos velas previas.

- Condición para la formación de un FVG bajista: cuando el precio más bajo de la vela anterior es superior al precio más alto de las dos velas previas.

- La señal de entrada se activa según el parámetro de umbral de FVG, solo cuando el tamaño de la brecha supera un porcentaje específico del precio.

- El control del riesgo utiliza una proporción fija (1%) del capital de la cuenta como estándar de stop loss.

- El objetivo de beneficio se establece en un número fijo de puntos (50 puntos).

Ventajas de la estrategia

- Gestión de riesgos científica y razonable: utiliza un stop loss basado en un porcentaje del capital de la cuenta, logrando un control dinámico del riesgo.

- Reglas de trading claras: emplea un objetivo de beneficio fijo, evitando juicios subjetivos.

- Rendimiento sobresaliente: la alta tasa de ganancia y el factor de beneficio indican una buena estabilidad de la estrategia.

- Implementación simple: la lógica del código es clara, fácil de entender y mantener.

- Buena adaptabilidad: se puede ajustar mediante parámetros para adaptarse a diferentes entornos de mercado.

Riesgos de la estrategia

- Riesgo de volatilidad del mercado: en mercados de alta volatilidad, el objetivo de beneficio fijo en puntos puede no ser lo suficientemente flexible.

- Riesgo de deslizamiento: las operaciones frecuentes pueden generar costos de deslizamiento elevados.

- Dependencia de parámetros: el rendimiento de la estrategia depende fuertemente del umbral de FVG.

- Riesgo de falsas rupturas: algunas señales de FVG pueden ser falsas rupturas, requiriendo indicadores de confirmación adicionales.

- Riesgo de gestión del capital: un stop loss de proporción fija en caso de pérdidas consecutivas puede provocar una rápida disminución del capital.

Direcciones de optimización de la estrategia

- Introducir indicadores de volatilidad del mercado para ajustar dinámicamente el objetivo de beneficio.

- Agregar un filtro de tendencia para evitar operar en mercados laterales.

- Desarrollar un mecanismo de confirmación de múltiples marcos temporales.

- Optimizar el algoritmo de gestión de posiciones, introduciendo un sistema de posiciones variables.

- Agregar un filtro de horario de negociación para evitar períodos de alta volatilidad.

- Desarrollar un sistema de puntuación de intensidad de señales para filtrar oportunidades de trading de alta calidad.

Conclusión

Esta estrategia combina la teoría de las brechas de valor justo con métodos científicos de gestión de riesgos, demostrando buenos resultados de trading. La alta tasa de ganancia y el factor de beneficio estable indican su valor práctico en el trading real. Mediante las direcciones de optimización sugeridas, la estrategia aún tiene margen de mejora. Se recomienda que los operadores realicen una optimización de parámetros exhaustiva y una verificación de backtesting antes de su uso en operaciones reales.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Fair Value Gap Strategy with % SL and Fixed TP", overlay=true, initial_capital=500, default_qty_type=strategy.fixed, default_qty_value=1)

// Parameters- 1