Estrategia de regresión bidireccional de cruce de RSI y Bandas de Bollinger

Resumen

Esta estrategia es un sistema de trading basado en el análisis técnico dual del Índice de Fuerza Relativa (RSI) y las Bandas de Bollinger. La estrategia combina las señales de sobrecompra/sobreventa del RSI con las señales de ruptura de los canales de precios de las Bandas de Bollinger, construyendo un marco completo de decisión comercial. Está especialmente diseñada para operar en entornos de mercado con alta volatilidad, logrando operaciones con riesgo controlado mediante condiciones estrictas de entrada y salida.

Principio de la Estrategia

La lógica central de la estrategia se basa en la acción coordinada de dos indicadores técnicos principales:

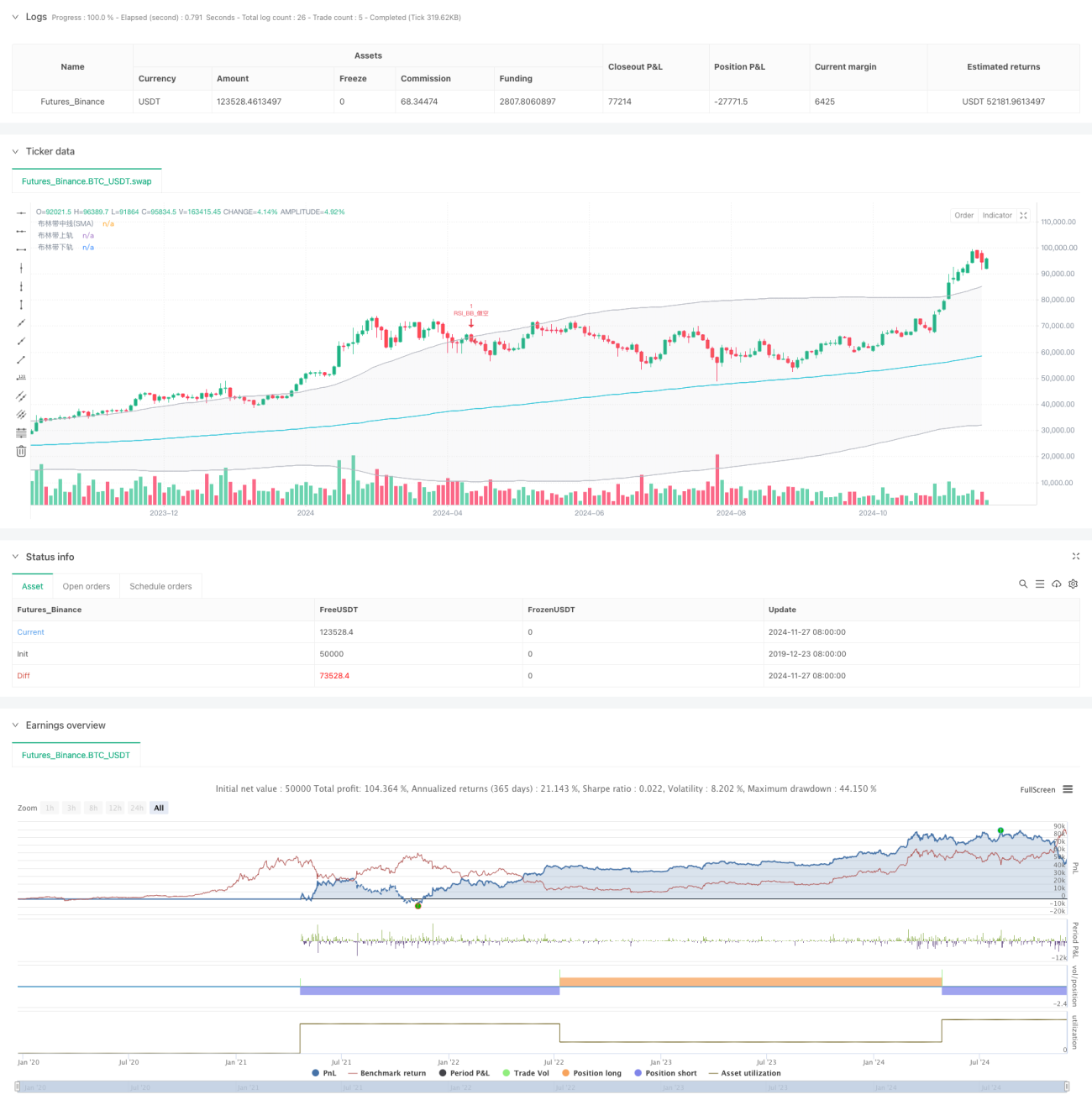

- El indicador RSI utiliza un período de cálculo de 6, estableciendo 50 como nivel crítico de sobrecompra/sobreventa para capturar el estado de sobrecompra o sobreventa del precio.

- Las Bandas de Bollinger emplean una media móvil de 200 períodos como banda central, con un múltiplo de desviación estándar de 2.0, formando las bandas superior e inferior.

- Condición de compra (largo): Se activa cuando el RSI supera al alza el nivel de sobreventa (50) y, al mismo tiempo, el precio supera al alza la banda inferior de Bollinger.

- Condición de venta (corto): Se activa cuando el RSI cruza a la baja el nivel de sobrecompra (50) y, al mismo tiempo, el precio cruza a la baja la banda superior de Bollinger.

- La estrategia utiliza un mecanismo de gestión de órdenes OCA (One-Cancels-All), asegurando que solo haya una operación activa en cada momento.

Ventajas de la Estrategia

- Mecanismo de doble confirmación: Reduce las señales falsas mediante la confirmación conjunta del RSI y las Bandas de Bollinger.

- Control de riesgo sólido: Utiliza las Bandas de Bollinger como nivel de stop-loss, proporcionando criterios claros de control de riesgo.

- Alta adaptabilidad: Las Bandas de Bollinger ajustan automáticamente el rango de negociación según la volatilidad del mercado.

- Optimización de la gestión de órdenes: El mecanismo OCA evita operaciones duplicadas y mejora la eficiencia del uso del capital.

- Parámetros ajustables: Todos los parámetros clave pueden optimizarse según las características del mercado.

Riesgos de la Estrategia

- Riesgo de mercado lateral: En mercados laterales o en rango, puede generar señales de ruptura falsas con frecuencia.

- Riesgo de rezago: Debido al uso de medias móviles, la estrategia presenta cierto rezago.

- Sensibilidad a parámetros: La configuración de los parámetros del RSI y las Bandas de Bollinger afecta significativamente el rendimiento de la estrategia.

- Dependencia del entorno del mercado: La estrategia se desempeña mejor en mercados con tendencia clara, y puede tener un rendimiento deficiente en mercados laterales.

Direcciones de Optimización de la Estrategia

- Ajuste dinámico de parámetros: Se puede ajustar dinámicamente el umbral de sobrecompra/sobreventa del RSI según la volatilidad del mercado.

- Incorporar filtro de entorno de mercado: Agregar indicadores de juicio de tendencia para utilizar parámetros de trading diferentes según el entorno del mercado.

- Optimización del mecanismo de toma de ganancias: Se puede añadir un mecanismo de toma de ganancias dinámico basado en el ATR.

- Optimización de la gestión de posición: Ajustar dinámicamente el tamaño de la posición según la intensidad de la señal y la volatilidad del mercado.

- Filtro de tiempo: Agregar restricciones de ventana horaria para evitar operar en períodos no adecuados.

Conclusión

Esta estrategia, mediante la acción coordinada del RSI y las Bandas de Bollinger, construye un sistema de trading relativamente completo. Su principal ventaja radica en el mecanismo de doble confirmación y el control de riesgo sólido, pero también se debe prestar atención al impacto del entorno del mercado en su rendimiento. A través de las direcciones de optimización propuestas, se puede mejorar aún más la estabilidad y la capacidad de generación de beneficios de la estrategia.

- 1