Estrategia de SuperTrend dinámico adaptativo de volatilidad de múltiples pasos

Resumen

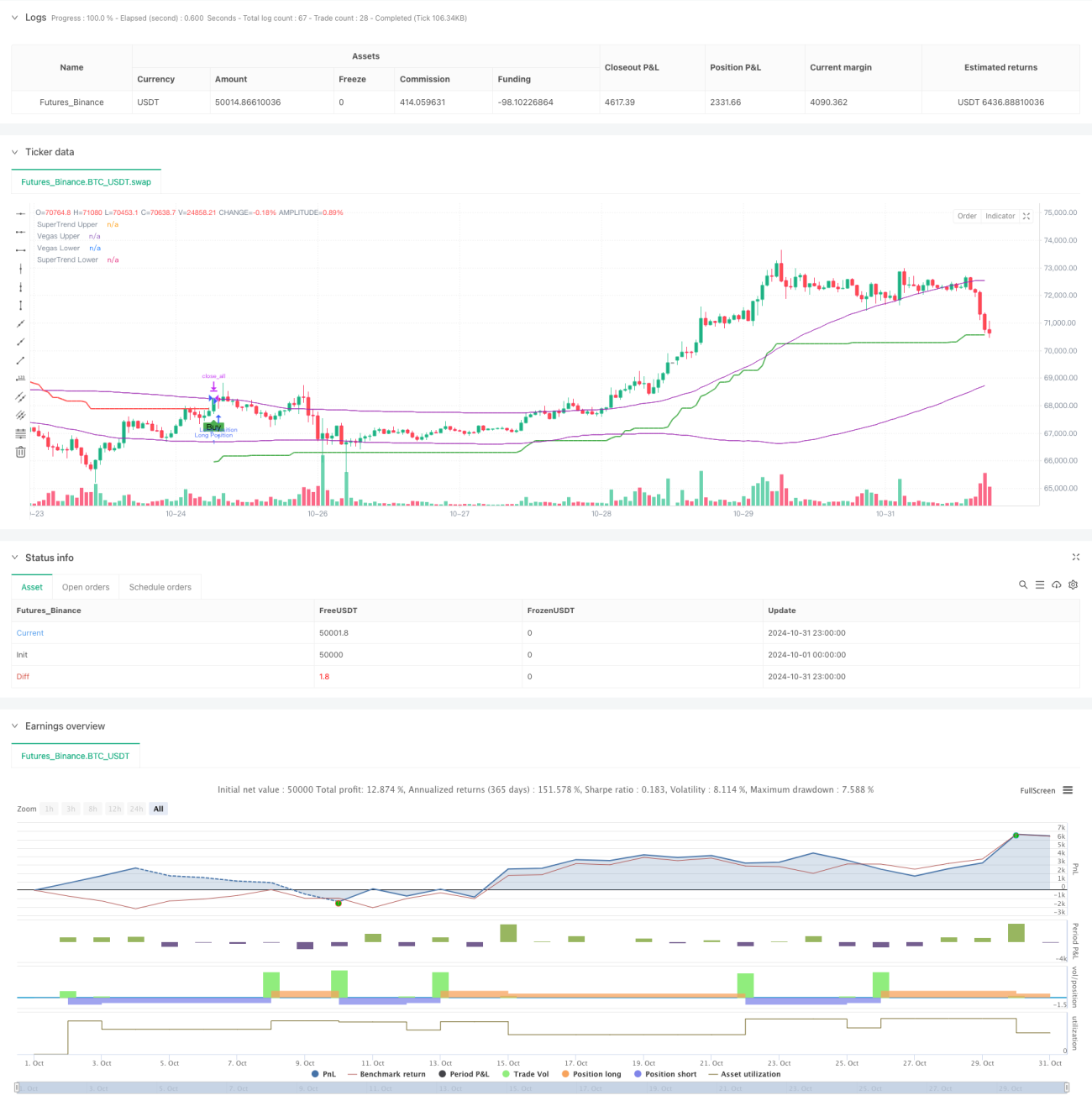

La Estrategia de Supertendencia Dinámica Adaptativa a la Volatilidad Multietapa es un sistema de trading innovador que combina el canal de Vegas y el indicador SuperTrend. Su singularidad radica en la capacidad de adaptarse dinámicamente a la volatilidad del mercado y en el uso de un mecanismo de toma de ganancias en múltiples pasos para optimizar la relación riesgo-rendimiento. Al combinar el análisis de volatilidad del canal de Vegas con la función de seguimiento de tendencias del SuperTrend, la estrategia ajusta automáticamente sus parámetros cuando cambian las condiciones del mercado, proporcionando así señales de trading más precisas.

Principio de la Estrategia

El funcionamiento de la estrategia se basa en tres componentes principales: el cálculo del canal de Vegas, la detección de tendencias y el mecanismo de toma de ganancias en múltiples pasos. El canal de Vegas utiliza la media móvil simple (SMA) y la desviación estándar (STD) para definir el rango de fluctuación del precio, mientras que el indicador SuperTrend determina la dirección de la tendencia basándose en el valor ATR ajustado. Cuando la tendencia del mercado cambia, el sistema genera una señal de trading. El mecanismo de toma de ganancias en múltiples pasos permite salir parcialmente en diferentes niveles de precio, bloqueando ganancias mientras se permite que una parte de la posición continúe obteniendo beneficios potenciales. La singularidad de la estrategia radica en su factor de ajuste de volatilidad, que modifica dinámicamente el multiplicador del SuperTrend según la anchura del canal de Vegas.

Ventajas de la Estrategia

- Adaptabilidad dinámica: A través del factor de ajuste de volatilidad, la estrategia puede adaptarse automáticamente a diferentes condiciones del mercado.

- Gestión del riesgo: El mecanismo de toma de ganancias en múltiples pasos proporciona un plan sistemático para asegurar beneficios.

- Personalización: Ofrece múltiples opciones de ajuste de parámetros para adaptarse a diferentes estilos de trading.

- Cobertura integral del mercado: Admite operaciones tanto en largo como en corto.

- Retroalimentación visual: Proporciona una interfaz gráfica clara que facilita el análisis y la toma de decisiones.

Riesgos de la Estrategia

- Sensibilidad a los parámetros: Diferentes combinaciones de parámetros pueden dar lugar a una gran variabilidad en el rendimiento de la estrategia.

- Retardo: Los indicadores basados en medias móviles presentan cierto rezago.

- Riesgo de falsas rupturas: En mercados laterales, pueden generarse señales erróneas.

- Compensación en la toma de ganancias: Una toma de ganancias prematura puede hacer perder grandes tendencias, mientras que una demasiado tardía puede erosionar las ganancias ya obtenidas.

Direcciones de Optimización

- Introducir un filtro de condiciones de mercado: Ajustar los parámetros de la estrategia según las diferentes condiciones del mercado.

- Añadir análisis de volumen: Mejorar la fiabilidad de las señales.

- Desarrollar un mecanismo adaptativo de toma de ganancias: Ajustar dinámicamente los niveles de toma de ganancias según la volatilidad del mercado.

- Integrar otros indicadores técnicos: Proporcionar confirmación de señales.

- Implementar gestión dinámica de posiciones: Ajustar el tamaño de las operaciones según el riesgo del mercado.

Conclusión

La Estrategia de Supertendencia Dinámica Adaptativa a la Volatilidad Multietapa representa un enfoque avanzado de trading cuantitativo. Al combinar múltiples indicadores técnicos y un innovador mecanismo de toma de ganancias, ofrece a los traders un sistema de trading integral. Su adaptabilidad dinámica y sus funciones de gestión de riesgos la hacen especialmente adecuada para operar en diferentes entornos de mercado, y cuenta con un buen potencial de escalabilidad y optimización. Mediante mejoras y optimizaciones continuas, se espera que esta estrategia proporcione un rendimiento de trading más estable en el futuro.

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Multi-Step Vegas SuperTrend - strategy [presentTrading]", shorttitle="Multi-Step Vegas SuperTrend - strategy [presentTrading]", overlay=true, precision=3, commission_value=0.1, commission_type=strategy.commission.percent, slippage=1, currency=currency.USD)

// Input settings allow the user to customize the strategy's parameters.- 1