Sistema de trading de seguimiento de media móvil de impulso mixto de doble cadena

Resumen

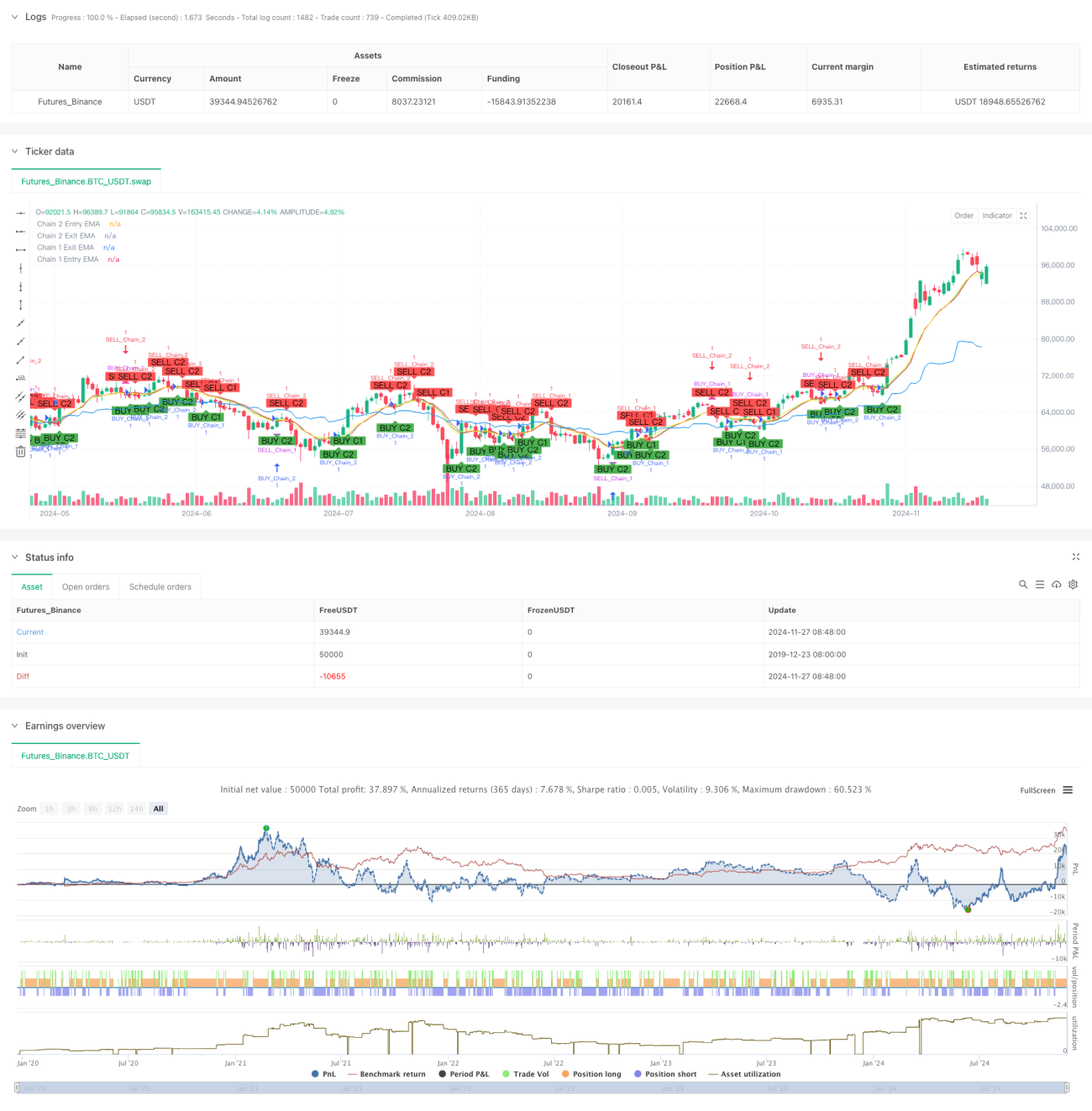

Esta estrategia es un sistema de trading innovador basado en la media móvil exponencial (EMA), que captura oportunidades del mercado mediante la configuración de dos cadenas de trading independientes en diferentes marcos temporales. La estrategia integra las ventajas del seguimiento de tendencia a largo plazo y el trading de impulso a corto plazo, generando señales de trading a través del cruce de EMA en múltiples marcos temporales como semanal, diario, 12 horas y 9 horas, logrando un análisis y comprensión multidimensional del mercado.

Principio de la estrategia

La estrategia adopta un diseño de doble cadena, cada una con su propia lógica de entrada y salida:

Cadena 1 (Tendencia a largo plazo) utiliza los marcos temporales semanal y diario:

- Señal de entrada: Cuando el precio de cierre supera la EMA en el marco semanal, se genera una señal de compra.

- Señal de salida: Cuando el precio de cierre cruza por debajo de la EMA en el marco diario, se genera una señal de cierre de posición.

- Período de EMA predeterminado: 10, ajustable según sea necesario.

Cadena 2 (Impulso a corto plazo) utiliza los marcos temporales de 12 horas y 9 horas:

- Señal de entrada: Cuando el precio de cierre supera la EMA en el marco de 12 horas, se genera una señal de compra.

- Señal de salida: Cuando el precio de cierre cruza por debajo de la EMA en el marco de 9 horas, se genera una señal de cierre de posición.

- Período de EMA predeterminado: 9, ajustable según sea necesario.

Ventajas de la estrategia

- Análisis multidimensional del mercado: mediante la combinación de diferentes marcos temporales, se obtiene una comprensión completa de la tendencia del mercado.

- Alta flexibilidad: las dos cadenas se pueden activar o desactivar de forma independiente, adaptándose a diferentes estilos de trading.

- Control de riesgos sólido: utiliza múltiples marcos temporales para confirmar, reduciendo el riesgo de señales falsas.

- Alta capacidad de ajuste de parámetros: tanto los períodos de EMA como los marcos temporales se pueden modificar según sea necesario.

- Función de backtesting completa: incluye configuración del período de backtesting, facilitando la validación y optimización de la estrategia.

Riesgos de la estrategia

- Riesgo de reversión de tendencia: puede generar rezago en mercados altamente volátiles.

- Riesgo de configuración de marcos temporales: diferentes mercados pueden requerir diferentes combinaciones de marcos temporales.

- Riesgo de optimización de parámetros: la optimización excesiva puede provocar sobreajuste.

- Riesgo de superposición de señales: la activación simultánea de ambas cadenas puede aumentar el riesgo de la posición.

Recomendaciones para el control de riesgos:

- Establecer niveles razonables de stop loss.

- Ajustar los parámetros según las características del mercado.

- Realizar backtesting suficiente antes de operar en vivo.

- Controlar la proporción de capital en cada operación.

Direcciones de optimización de la estrategia

- Optimización del filtrado de señales:

- Agregar un mecanismo de confirmación de volumen.

- Introducir indicadores de volatilidad para filtrar señales.

- Agregar confirmación de fuerza de tendencia.

- Optimización del control de riesgos:

- Desarrollar un mecanismo dinámico de stop loss.

- Diseñar un sistema de gestión de posiciones.

- Agregar funciones de control de drawdown.

- Optimización de marcos temporales:

- Investigar la combinación óptima de marcos temporales.

- Desarrollar un mecanismo adaptativo de marcos temporales.

- Agregar funciones de identificación del estado del mercado.

Resumen

El sistema de trading de doble cadena híbrido de medias móviles y seguimiento de impulso logra un análisis y comprensión multidimensional del mercado mediante la combinación innovadora de estrategias de medias móviles de largo y corto plazo. El diseño del sistema es flexible y se puede ajustar según diferentes condiciones del mercado y estilos de traders, ofreciendo una alta practicidad. Con un control de riesgos adecuado y una optimización continua, esta estrategia tiene el potencial de generar ganancias estables en el trading real. Se recomienda a los traders realizar backtesting suficiente y optimizar los parámetros antes de usarla en vivo para lograr los mejores resultados de trading.

- 1