Sistema de trading de acción del precio con soporte y resistencia dinámicos

Resumen

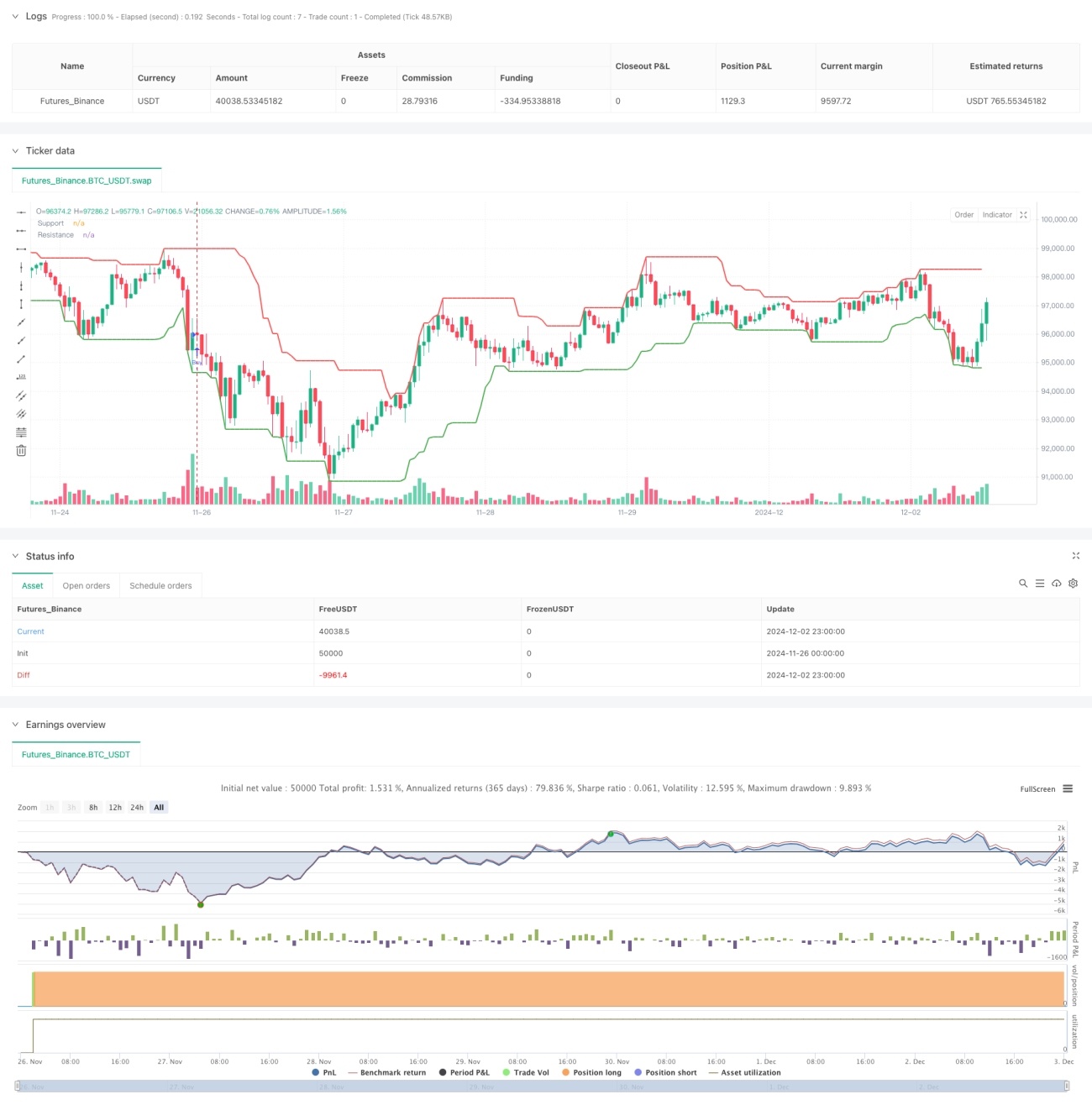

Esta estrategia es un sistema de trading basado en la acción del precio y niveles dinámicos de soporte y resistencia, que identifica patrones de precios clave cerca de dichos niveles para operar. El sistema utiliza un cálculo dinámico de soporte y resistencia de 16 períodos, combinado con cuatro patrones clásicos de velas de reversión — martillo, estrella fugaz, doji y pin bar — para capturar posibles oportunidades de reversión en el mercado. La estrategia emplea un stop loss y take profit de porcentaje fijo para gestionar el riesgo, y utiliza un parámetro de sensibilidad para controlar la rigurosidad de las señales de entrada.

Principio de la Estrategia

El núcleo de la estrategia consiste en calcular dinámicamente niveles de soporte y resistencia, formando un límite superior e inferior para la acción del precio. Cuando el precio se aproxima a estos niveles clave, el sistema busca patrones de velas específicos como señales de reversión. La condición de entrada requiere que aparezca un patrón de reversión dentro de un rango del 1,8% (sensibilidad por defecto) respecto a los niveles de soporte/resistencia. El sistema utiliza una regla de gestión de capital del 35%, combinada con un stop loss del 16% y un take profit del 9,5%, limitando el riesgo de cada operación a aproximadamente el 5,6% del capital total de la cuenta. La estrategia se implementa en Pine Script e incluye funciones completas de gestión de operaciones y visualización.

Ventajas de la Estrategia

- Combina dos de los elementos más fiables del análisis técnico: patrones de precio y soporte/resistencia, aumentando la fiabilidad de las señales.

- Utiliza niveles de soporte y resistencia calculados dinámicamente, adaptándose a los cambios del mercado.

- Aplica una estricta gestión de capital y medidas de control de riesgo, previniendo grandes retrocesos.

- La lógica de la estrategia es clara y los parámetros son altamente ajustables, facilitando la optimización según diferentes condiciones del mercado.

- Las señales de entrada son definidas y no requieren juicio subjetivo, siendo adecuadas para el trading automatizado.

Riesgos de la Estrategia

- En mercados de alta volatilidad, la efectividad de los niveles de soporte y resistencia puede disminuir.

- El stop loss se sitúa relativamente lejos (16%), lo que podría generar pérdidas significativas en movimientos bruscos.

- El ajuste del parámetro de sensibilidad tiene un gran impacto en la frecuencia y precisión de las operaciones.

- Depender únicamente de patrones de velas podría hacer pasar por alto otras señales importantes del mercado.

- Es necesario considerar el impacto de los costos de transacción en la rentabilidad de la estrategia.

Direcciones de Optimización

- Incorporar el volumen como indicador de confirmación adicional para mejorar la fiabilidad de las señales.

- Desarrollar un parámetro de sensibilidad adaptativo que se ajuste dinámicamente según la volatilidad del mercado.

- Optimizar la colocación del stop loss, considerando el uso de stop loss móvil o por tramos.

- Agregar un filtro de tendencia para evitar operar en contra de tendencias fuertes.

- Desarrollar un sistema de gestión de posición dinámico que ajuste el tamaño de las operaciones según las condiciones del mercado.

Conclusión

Esta estrategia de trading basada en la acción del precio, al combinar niveles dinámicos de soporte/resistencia y patrones de reversión clásicos, proporciona a los traders un enfoque sistemático para operar. Su ventaja radica en una lógica clara y un riesgo controlable, aunque aún requiere una optimización continua según los resultados reales de las operaciones. Se recomienda a los traders realizar pruebas retrospectivas exhaustivas y ajustar los parámetros antes de utilizarla en cuentas reales, además de personalizarla según su experiencia en el mercado.

/*backtest

start: 2024-11-26 00:00:00

end: 2024-12-03 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © felipemiransan

//@version=5- 1