Estrategia Adaptativa Híbrida de Dos Medias Móviles y RSI

Resumen

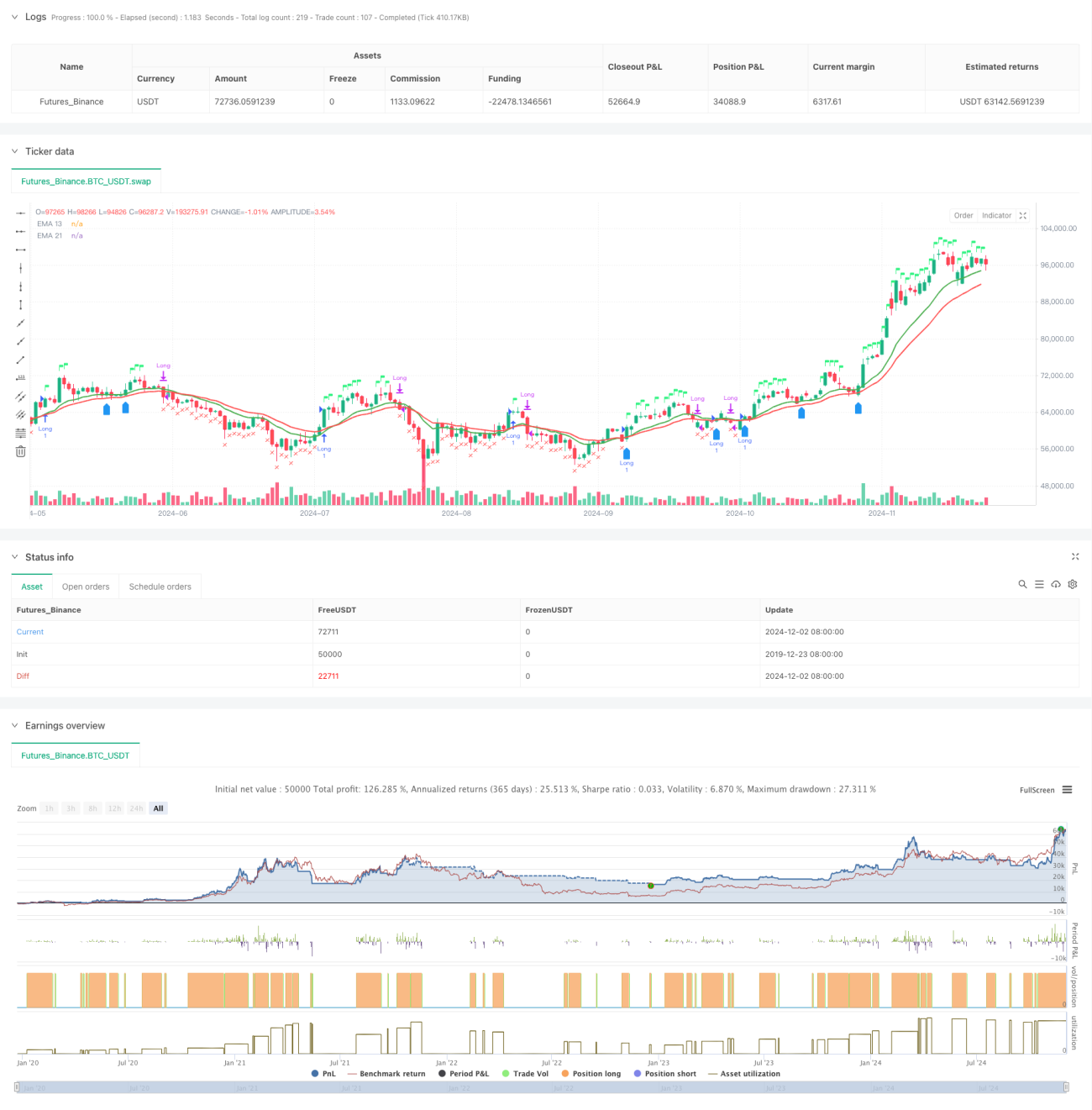

Esta estrategia es un sistema de trading integral que combina un sistema de medias móviles dobles, el Índice de Fuerza Relativa (RSI) y el análisis de Fuerza Relativa (RS). La estrategia confirma la tendencia mediante el cruce de las medias móviles exponenciales (EMA) de 13 y 21 períodos, al mismo tiempo que combina el RSI y el valor RS en relación con el índice de referencia para confirmar las señales de trading, logrando así un mecanismo de toma de decisiones multidimensional. Esta estrategia también incluye un mecanismo de control de riesgos basado en el máximo de 52 semanas y la evaluación de condiciones para reingresar al mercado.

Principio de la Estrategia

La estrategia utiliza un mecanismo de confirmación de señales múltiples:

- Las señales de entrada deben cumplir simultáneamente las siguientes condiciones:

- EMA13 cruza por encima de EMA21 o el precio está por encima de EMA13.

- RSI mayor a 60.

- Fuerza Relativa (RS) positiva.

- Las condiciones de salida incluyen:

- El precio cae por debajo de EMA21.

- RSI por debajo de 50.

- RS se vuelve negativo.

- Condiciones de reingreso:

- El precio cruza por encima de EMA13 y EMA13 es mayor que EMA21.

- RS se mantiene positivo.

- O el precio supera el máximo de la semana anterior.

Ventajas de la Estrategia

- El mecanismo de confirmación de señales múltiples reduce el riesgo de falsos rompimientos.

- La combinación con el análisis de fuerza relativa permite seleccionar eficazmente los activos más fuertes.

- Incorpora un mecanismo de ajuste de período de tiempo adaptativo.

- Cuenta con un sistema completo de control de riesgos.

- Incluye un mecanismo inteligente de reingreso.

- Proporciona visualización en tiempo real del estado de las operaciones.

Riesgos de la Estrategia

- En mercados laterales puede generar operaciones frecuentes.

- La dependencia de múltiples indicadores puede provocar un retraso en las señales.

- Los umbrales fijos del RSI pueden no adaptarse a todos los entornos de mercado.

- El cálculo de la fuerza relativa depende de la precisión del índice de referencia.

- El stop loss basado en el máximo de 52 semanas podría ser demasiado amplio.

Direcciones de Optimización de la Estrategia

- Introducir umbrales adaptativos para el RSI.

- Optimizar la lógica de evaluación de las condiciones de reingreso.

- Agregar la dimensión del análisis de volumen de operaciones.

- Mejorar los mecanismos de take profit y stop loss.

- Incorporar un filtro de volatilidad.

- Optimizar el período de cálculo de la fuerza relativa.

Conclusión

Esta estrategia construye un sistema de trading integral mediante la combinación del análisis técnico y el análisis de fuerza relativa. Su mecanismo de confirmación de señales múltiples y su sistema de control de riesgos le otorgan una gran utilidad práctica. A través de las direcciones de optimización sugeridas, la estrategia aún tiene margen para mejorar. La implementación exitosa de la estrategia requiere que el trader tenga un profundo conocimiento del mercado y ajuste los parámetros adecuadamente según las características específicas del activo a operar.

- 1