Estrategia Avanzada de Stop Loss Dinámico y Toma de Ganancias Objetivo

Resumen

Esta estrategia es un sistema de trading avanzado que combina un trailing stop dinámico, una relación riesgo-recompensa y una salida por extremos del RSI. La estrategia identifica patrones específicos en el mercado (patrones de velas paralelas y patrones de velas de aguja) para realizar operaciones, utiliza ATR y el mínimo reciente para establecer stops dinámicos, y determina el objetivo de ganancias según una relación riesgo-recompensa predefinida. El sistema también integra un mecanismo de juicio de sobrecalentamiento/sobreenfriamiento del mercado basado en el indicador RSI, que permite cerrar posiciones a tiempo cuando el mercado alcanza valores extremos.

Principio de la estrategia

La lógica central de la estrategia incluye los siguientes componentes clave:

- Las señales de entrada se basan en dos patrones: el patrón de velas paralelas (una gran vela alcista seguida de una gran vela bajista) y el patrón de doble vela de aguja.

- El trailing stop dinámico utiliza un multiplicador ATR aplicado al mínimo de las últimas N velas, asegurando que el stop se adapte dinámicamente a la volatilidad del mercado.

- El objetivo de ganancias se establece en función de una relación riesgo-recompensa fija, calculada mediante el valor de riesgo (R) de cada operación.

- El tamaño de la posición se calcula dinámicamente según un monto de riesgo fijo y el valor de riesgo de cada operación.

- El mecanismo de salida por extremos del RSI activa una señal de cierre cuando el mercado está sobrecalentado o sobreenfriado.

Ventajas de la estrategia

- Gestión dinámica del riesgo: mediante la combinación de ATR y el mínimo reciente, el stop puede ajustarse dinámicamente según la volatilidad del mercado.

- Control preciso de la posición: el método de cálculo de posición basado en un monto de riesgo fijo asegura que cada operación tenga el mismo riesgo.

- Mecanismo de salida multidimensional: combina trailing stop, objetivo de ganancias fijo y salida por extremos del RSI, tres mecanismos de salida.

- Flexibilidad en la dirección de las operaciones: se puede optar por operar solo en largo, solo en corto, o en ambas direcciones.

- Configuración clara de riesgo-recompensa: a través de una relación riesgo-recompensa predefinida, se establece explícitamente el objetivo de ganancias de cada operación.

Riesgos de la estrategia

- Riesgo de precisión en la identificación de patrones: los patrones de velas paralelas y velas de aguja pueden ser malinterpretados.

- Riesgo de deslizamiento en la configuración del stop: en mercados con alta volatilidad, se puede enfrentar un deslizamiento significativo.

- La salida por extremos del RSI puede ser prematura: en mercados con tendencias fuertes, podría provocar una salida anticipada y perder mayores ganancias.

- Limitación de la relación riesgo-recompensa fija: la relación óptima puede variar en diferentes entornos de mercado.

- Riesgo de sobreoptimización de parámetros: la combinación de múltiples parámetros puede llevar a un sobreajuste.

Direcciones de optimización de la estrategia

- Optimización de la señal de entrada: se pueden agregar más indicadores de confirmación de patrones, como volumen, indicadores de tendencia, etc.

- Relación riesgo-recompensa dinámica: ajustar la relación riesgo-recompensa según la volatilidad del mercado.

- Parámetros adaptativos inteligentes: introducir algoritmos de aprendizaje automático para optimizar dinámicamente los parámetros.

- Confirmación en múltiples marcos temporales: agregar mecanismos de confirmación de señales en más marcos de tiempo.

- Clasificación del entorno del mercado: utilizar diferentes combinaciones de parámetros según las diferentes condiciones del mercado.

Resumen

Se trata de una estrategia de trading bien diseñada que, al combinar múltiples conceptos de análisis técnico consolidados, construye un sistema de trading completo. La ventaja de la estrategia radica en su exhaustivo sistema de gestión de riesgos y sus reglas de trading flexibles, pero también es necesario prestar atención a los problemas de optimización de parámetros y adaptabilidad al mercado. A través de las direcciones de optimización sugeridas, la estrategia aún tiene margen de mejora.

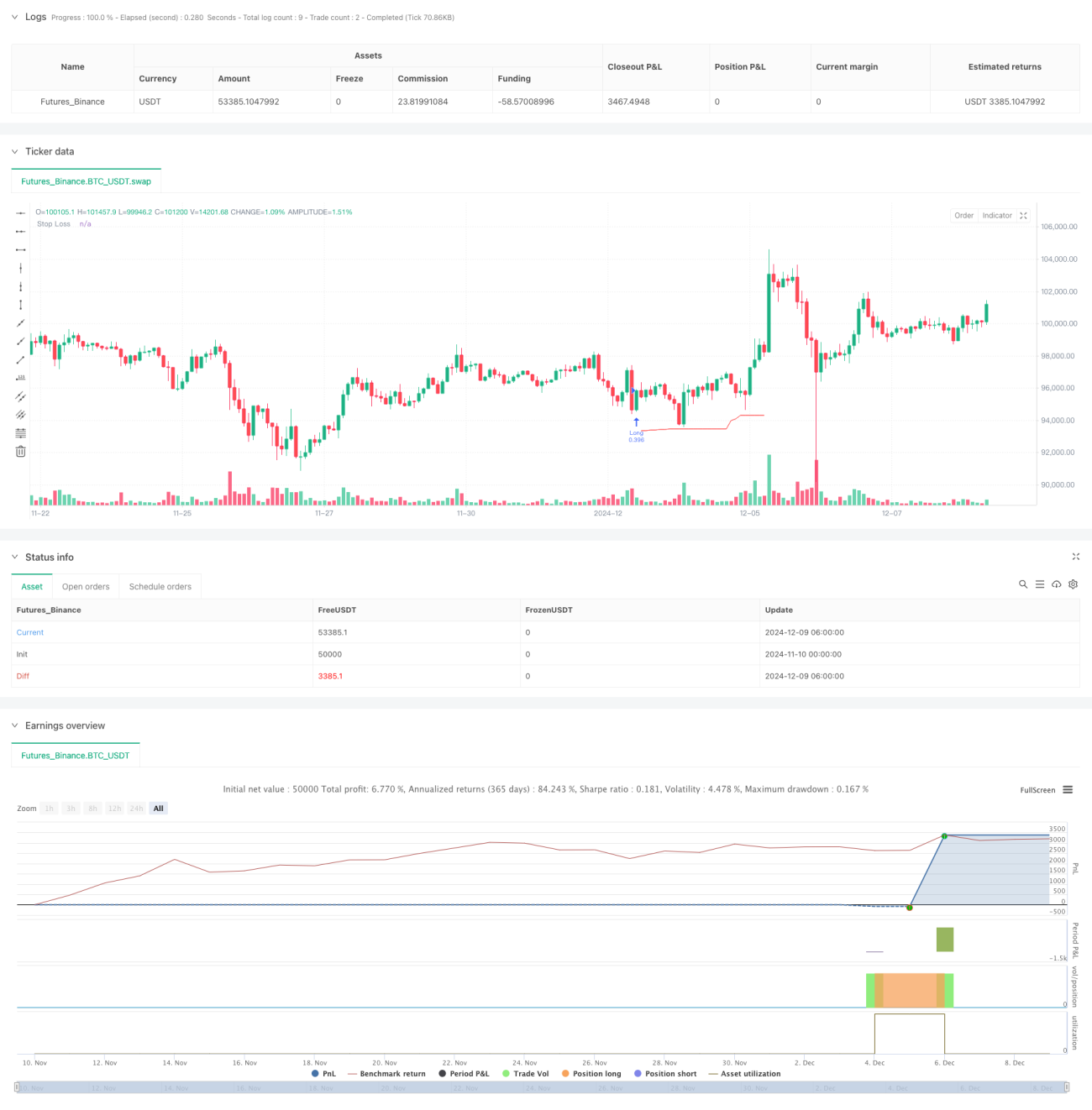

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ZenAndTheArtOfTrading | www.TheArtOfTrading.com

// @version=5

strategy("Trailing stop 1", overlay=true)- 1