Resumen

Esta estrategia es un sistema de trading inteligente que combina el MACD (Moving Average Convergence Divergence) y la Pendiente de Regresión Lineal (LRS). La estrategia optimiza el cálculo del indicador MACD mediante la combinación de múltiples métodos de media móvil e introduce el análisis de regresión lineal para mejorar la fiabilidad de las señales de trading. Permite al trader elegir de forma flexible entre utilizar un solo indicador o una combinación de dos indicadores para generar señales de trading, y está equipada con mecanismos de take profit y stop loss para controlar el riesgo.

Principio de la Estrategia

El núcleo de la estrategia es capturar las tendencias del mercado mediante el MACD optimizado y el indicador de regresión lineal. La parte del MACD emplea una combinación de cuatro métodos de media móvil: SMA, EMA, WMA y TEMA, lo que mejora la sensibilidad a las tendencias de precios. La parte de regresión lineal determina la dirección y la fuerza de la tendencia calculando la pendiente y la posición de la línea de regresión. Las señales de compra pueden basarse en el cruce dorado del MACD, la tendencia alcista de la regresión lineal, o la confirmación de ambos. Del mismo modo, las señales de venta también se pueden configurar de forma flexible. La estrategia incluye una configuración de take profit y stop loss basada en porcentajes, gestionando eficazmente la relación riesgo-beneficio de cada operación.

Ventajas de la Estrategia

- Flexibilidad en la combinación de indicadores: Permite elegir entre usar un solo indicador o una combinación de dos según las condiciones del mercado.

- Cálculo mejorado del MACD: Aumenta la precisión en la identificación de tendencias mediante múltiples métodos de media móvil.

- Confirmación objetiva de tendencias: Utiliza la regresión lineal para proporcionar un juicio de tendencia respaldado por estadísticas matemáticas.

- Gestión de riesgos completa: Integra mecanismos de take profit y stop loss.

- Alta ajustabilidad de parámetros: Los parámetros clave se pueden optimizar según las características del mercado.

Riesgos de la Estrategia

- Sensibilidad a los parámetros: Diferentes entornos de mercado pueden requerir ajustes frecuentes de los parámetros.

- Retardo en las señales: Los indicadores de media móvil presentan cierto rezago.

- No apta para mercados laterales: Puede generar señales falsas en mercados en rango lateral.

- Costo de oportunidad por confirmación doble: La confirmación estricta con dos indicadores puede hacer que se pierdan algunas buenas oportunidades de trading.

Direcciones de Optimización de la Estrategia

- Añadir identificación del entorno de mercado: Introducir indicadores de volatilidad para distinguir entre mercados en tendencia y en rango.

- Ajuste dinámico de parámetros: Ajustar automáticamente los parámetros del MACD y la regresión lineal según el estado del mercado.

- Optimizar take profit y stop loss: Introducir take profit y stop loss dinámicos, ajustando automáticamente según la volatilidad del mercado.

- Añadir análisis de volumen: Combinar indicadores de volumen para aumentar la credibilidad de las señales.

- Introducir análisis de marcos temporales: Considerar la confirmación en múltiples marcos temporales para mejorar la precisión del trading.

Resumen

Esta estrategia crea un sistema de trading que combina flexibilidad y fiabilidad mediante la combinación de versiones mejoradas de indicadores clásicos y métodos estadísticos. Su diseño modular permite al trader ajustar de forma flexible los parámetros de la estrategia y los mecanismos de confirmación de señales según las diferentes condiciones del mercado. Con una optimización y mejora continuas, esta estrategia tiene el potencial de mantener un rendimiento estable en diversos entornos de mercado.

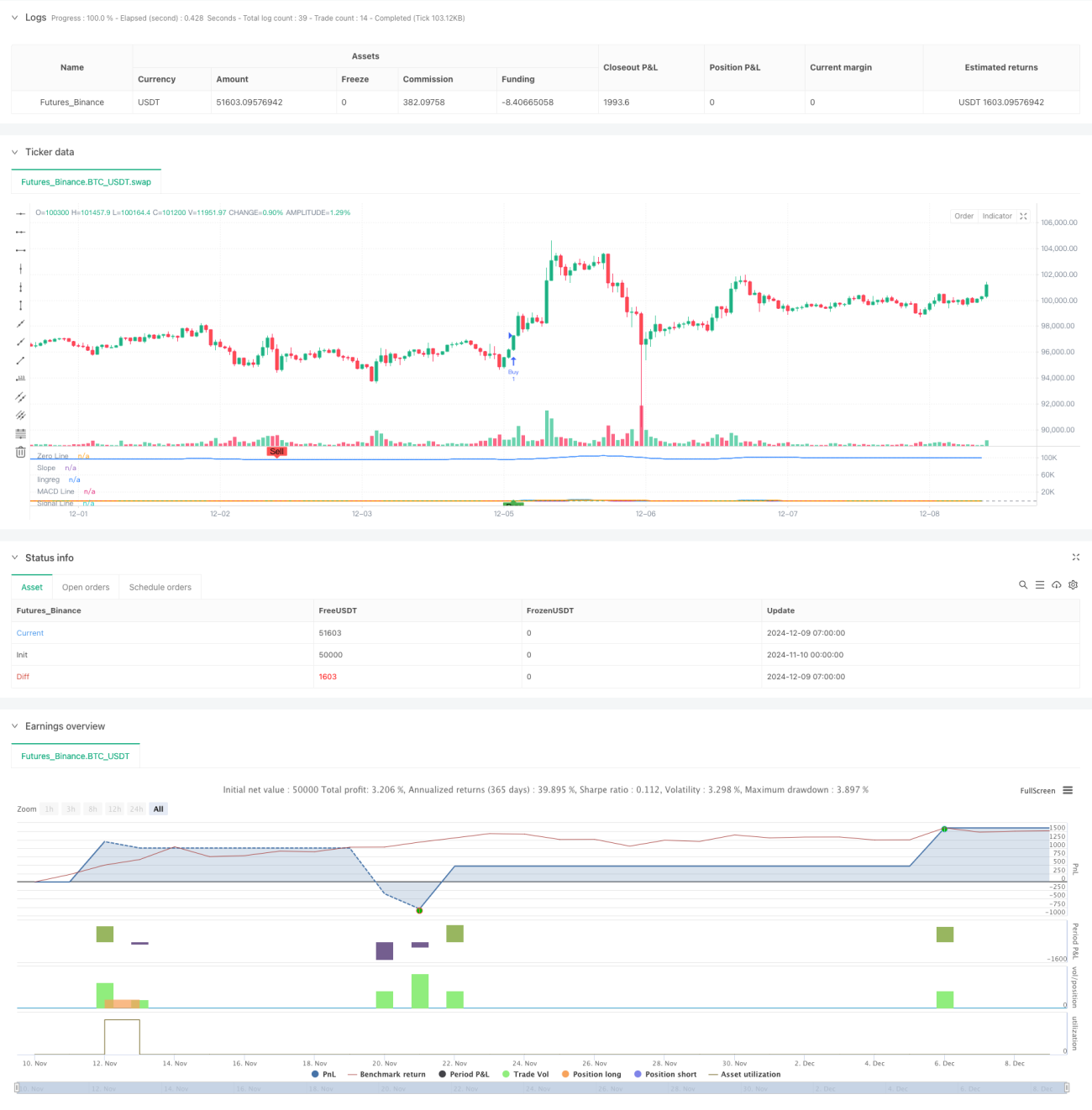

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('SIMPLIFIED MACD & LRS Backtest by NHBProd', overlay=false)

// Function to calculate TEMA (Triple Exponential Moving Average)- 1