Estrategia avanzada de trading de tendencia de momentum con media móvil exponencial

Resumen

Esta estrategia es una estrategia de seguimiento de tendencia basada en la media móvil exponencial (EMA) y el indicador de momentum. Combina señales de ruptura de momentum con un filtro de tendencia EMA para operar cuando la tendencia del mercado es clara. La estrategia incluye un módulo completo de gestión de riesgos, un filtro flexible de horario de negociación y funciones detalladas de análisis estadístico para mejorar la estabilidad y confiabilidad de la estrategia.

Principios de la Estrategia

La lógica central de la estrategia se basa en los siguientes elementos clave:

- Identificación de señales de momentum: Calcula el valor de momentum en un período de tiempo definido por el usuario. Cuando el momentum supera el umbral superior, se genera una señal de compra; cuando supera el umbral inferior, se genera una señal de venta.

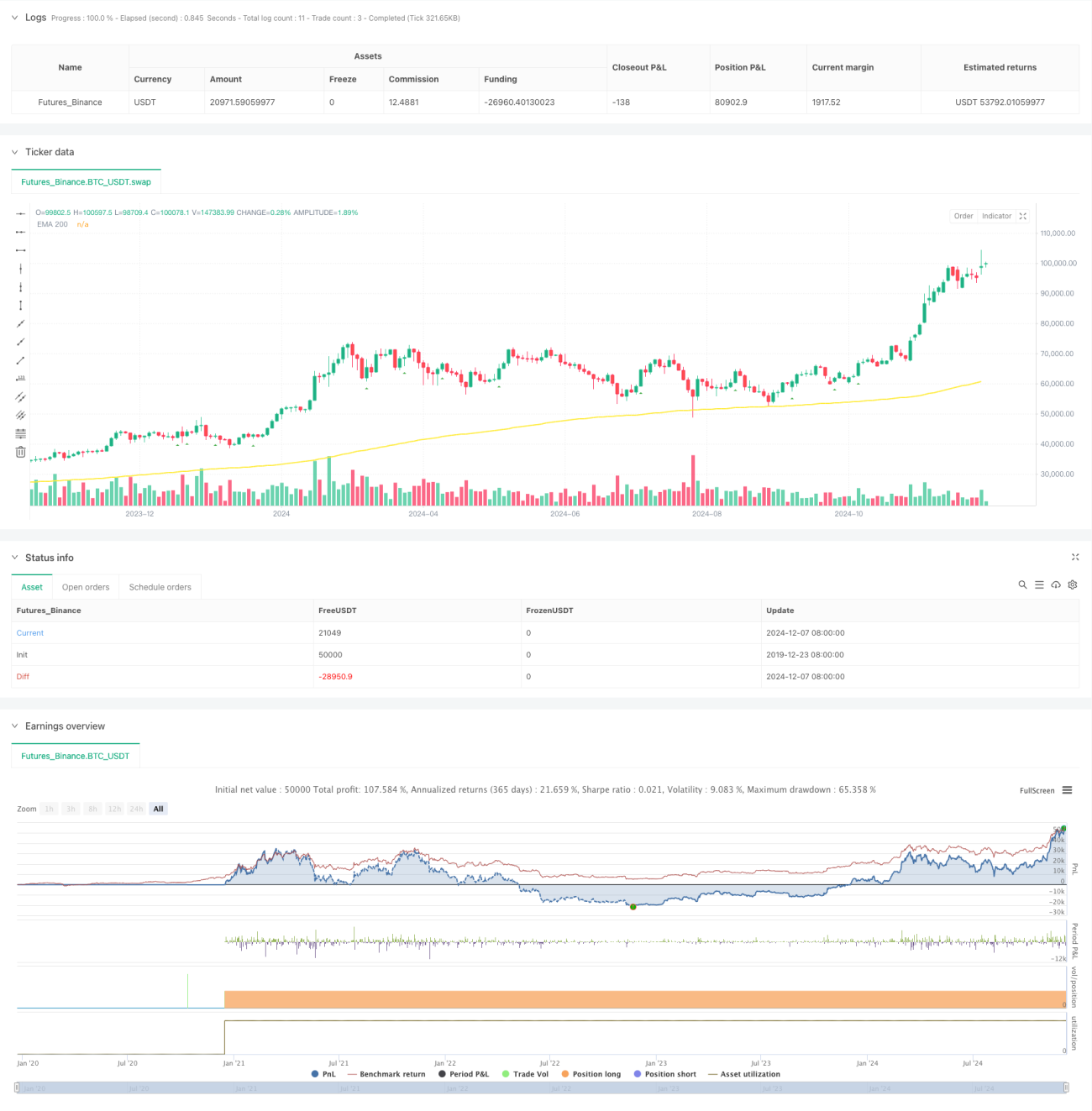

- Filtro de tendencia EMA: Utiliza una EMA de 200 períodos como referencia de tendencia. Cuando el precio está por encima de la EMA, se permiten posiciones largas; cuando está por debajo, se permiten posiciones cortas.

- Filtro de tiempo: Permite establecer horarios específicos de negociación y admite ajuste de zona horaria GMT, lo que permite que la estrategia se adapte mejor a los horarios de negociación de diferentes mercados.

- Control de riesgos: Admite configuraciones de stop loss y take profit basadas en ATR o un porcentaje fijo, y limita el número máximo de operaciones diarias.

Ventajas de la Estrategia

- Fuerte capacidad de seguimiento de tendencia: Mediante la doble confirmación de EMA y momentum, puede capturar efectivamente los movimientos principales de la tendencia.

- Gestión de riesgos completa: Ofrece múltiples opciones de stop loss, ya sea mediante stop loss dinámico basado en ATR o stop loss basado en un porcentaje fijo.

- Análisis estadístico integral: Realiza un seguimiento en tiempo real de múltiples indicadores de rendimiento, incluyendo la tasa de acierto en compras y ventas, y la relación riesgo-beneficio.

- Parámetros flexibles y ajustables: Los parámetros principales pueden optimizarse y ajustarse según las características de diferentes mercados.

Riesgos de la Estrategia

-

Riesgo de mercado lateral: En mercados con tendencia lateral, pueden generarse señales falsas con frecuencia.

Solución propuesta: Agregar un filtro de indicador de oscilación o aumentar el umbral de ruptura. -

Riesgo de deslizamiento: Durante períodos de alta volatilidad, puede enfrentarse a un deslizamiento significativo.

Solución propuesta: Establecer un rango de stop loss razonable y evitar operar en períodos de alta volatilidad. -

Riesgo de sobretrading: Las señales demasiado frecuentes pueden provocar sobretrading.

Solución propuesta: Limitar de manera razonable el número máximo de operaciones diarias.

Direcciones de Optimización de la Estrategia

- Optimización dinámica de parámetros: Ajustar automáticamente el umbral de momentum y el período de la EMA según la volatilidad del mercado.

- Análisis de múltiples marcos temporales: Agregar confirmación de tendencia en varios marcos temporales para mejorar la confiabilidad de las señales.

- Identificación del entorno del mercado: Incorporar un módulo de análisis de volatilidad para utilizar diferentes configuraciones de parámetros en distintos entornos de mercado.

- Clasificación de la intensidad de la señal: Clasificar las señales de ruptura según su intensidad y ajustar dinámicamente el tamaño de la posición según la intensidad de la señal.

Conclusión

Se trata de una estrategia de seguimiento de tendencia bien diseñada que captura oportunidades de mercado mediante la combinación de rupturas de momentum y la tendencia de la EMA. La estrategia cuenta con un sistema completo de gestión de riesgos, potentes funciones de análisis estadístico, y posee una buena practicidad y escalabilidad. Con una optimización y mejora continuas, se espera que esta estrategia pueda mantener un rendimiento estable en diferentes entornos de mercado.

- 1