Estrategia de stop loss y take profit para el comercio equilibrado con seguimiento adaptativo de retroceso

Resumen

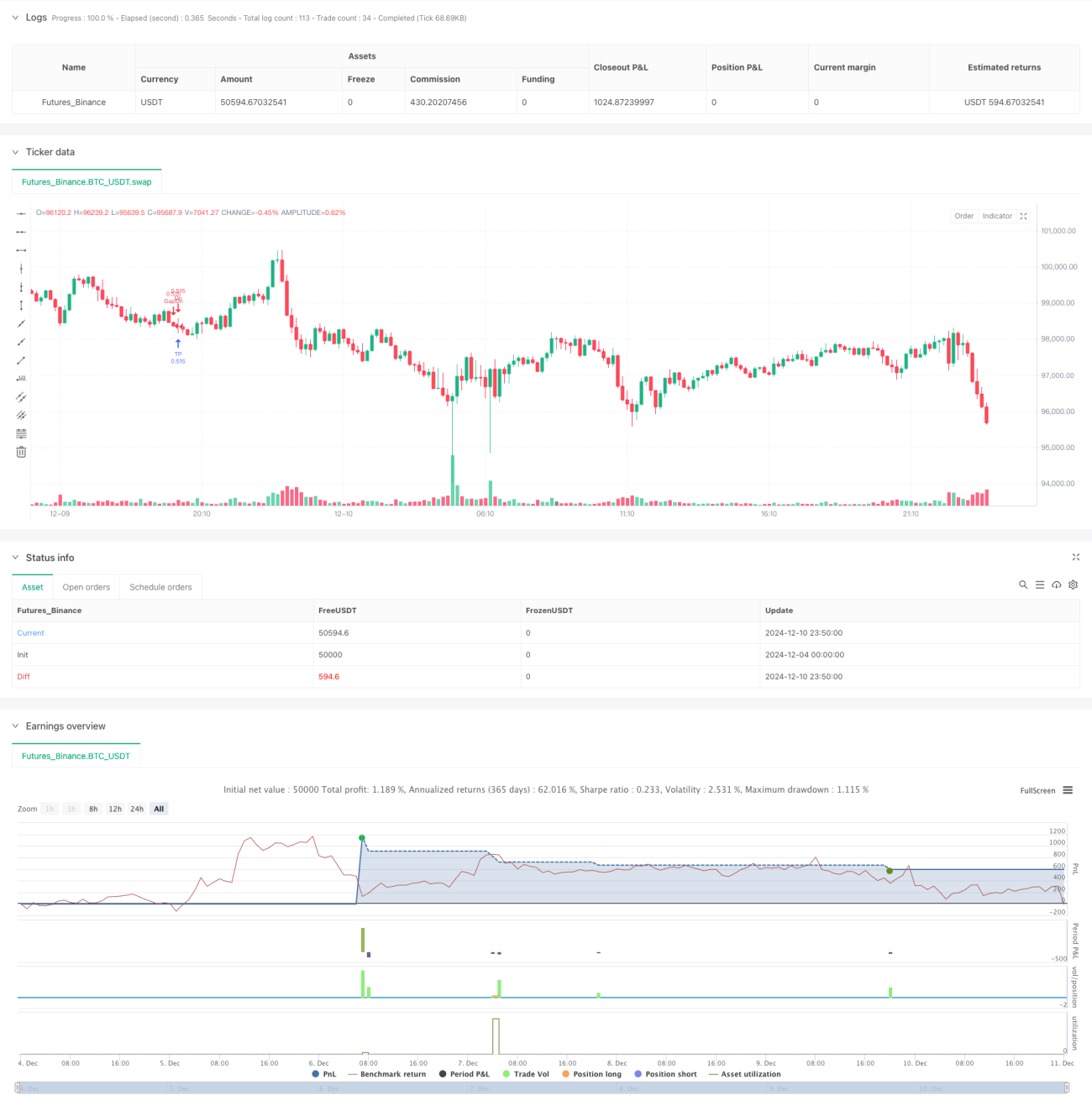

Esta estrategia es un sistema de trading adaptativo basado en gaps y movimientos de precios, que logra ganancias estables mediante puntos de entrada flexibles y una dinámica gestión de take profit y stop loss. La estrategia utiliza un método de escalado en pirámide y combina un sistema de órdenes OCA (One Cancels Other) para controlar el riesgo. El sistema ajusta automáticamente la dirección de las posiciones según la evolución del mercado, cerrando posiciones y deteniendo pérdidas cuando aparecen señales de reversión.

Principio de la estrategia

La estrategia opera principalmente a través de los siguientes mecanismos centrales:

- Mecanismo de trading de gaps: identifica gaps alcistas y bajistas, y coloca órdenes de stop loss de entrada en las posiciones del gap.

- Seguimiento de tendencia: determina la dirección de la tendencia según la relación entre el precio de apertura y el de cierre.

- Escalado en pirámide: permite mantener hasta 100 órdenes en la misma dirección.

- Take profit y stop loss dinámicos: establece niveles dinámicos de take profit y stop loss basados en el precio medio de la posición.

- Gestión de órdenes OCA: utiliza órdenes combinadas OCA para garantizar la ejecución mutuamente excluyente de las órdenes de take profit y stop loss.

- Límites intradía: controla el riesgo estableciendo un número máximo de órdenes ejecutadas en el mismo día.

Ventajas de la estrategia

- Alta adaptabilidad: la estrategia ajusta automáticamente la dirección y el tamaño de las posiciones según las condiciones del mercado.

- Riesgo controlable: gestiona el riesgo a través de múltiples mecanismos, incluyendo stop loss, órdenes OCA y límites intradía.

- Alta flexibilidad: admite el escalado en pirámide, lo que permite obtener mayores ganancias en mercados con tendencia.

- Alta eficiencia de ejecución: utiliza órdenes de stop loss para la entrada, permitiendo abrir posiciones rápidamente en niveles de precios clave.

- Alto grado de sistematización: todas las decisiones de trading son completamente sistemáticas, reduciendo la influencia emocional de la intervención humana.

Riesgos de la estrategia

- Riesgo de deslizamiento: puede enfrentar deslizamientos severos en mercados de movimientos rápidos.

- Riesgo de sobreoperación: las entradas y salidas frecuentes pueden generar altos costos de trading.

- Riesgo sistémico: en mercados de alta volatilidad, puede sufrir pérdidas significativas.

- Riesgo de gestión de capital: el escalado en pirámide puede llevar a una utilización excesiva del capital.

- Riesgo técnico: interrupciones en la ejecución del programa pueden causar problemas en la gestión de órdenes.

Direcciones de optimización de la estrategia

- Incorporar indicadores de volatilidad: ajustar dinámicamente los parámetros de take profit y stop loss según la volatilidad del mercado.

- Optimizar el mecanismo de escalado: diseñar reglas de escalado más detalladas para evitar el uso excesivo de capital.

- Mejorar el sistema de gestión de riesgos: agregar más indicadores de riesgo, como un límite máximo de retroceso intradía.

- Mejorar la ejecución de órdenes: optimizar el mecanismo de escalonamiento de órdenes para reducir el impacto del deslizamiento.

- Incorporar juicios de sentimiento del mercado: combinar indicadores como el volumen de operaciones para optimizar los momentos de entrada.

Conclusión

Se trata de una estrategia de trading bien diseñada y lógicamente sólida, que garantiza la estabilidad y seguridad de las operaciones a través de múltiples mecanismos. Su principal ventaja radica en su adaptabilidad y capacidad de control de riesgos, pero también es necesario tener en cuenta los riesgos asociados a la volatilidad del mercado. Con una optimización y mejora continuas, la estrategia tiene el potencial de mantener un rendimiento estable en diferentes entornos de mercado.

/*backtest

start: 2024-12-04 00:00:00

end: 2024-12-11 00:00:00

period: 10m

basePeriod: 10m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Greedy Strategy - maclaurin", pyramiding = 100, calc_on_order_fills=false, overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

backtestStartDate = input(timestamp("1 Jan 1990"),

title="Start Date", group="Backtest Time Period",- 1