Estrategia de seguimiento de tendencia ATR dinámico basada en la ruptura del nivel de soporte

Resumen

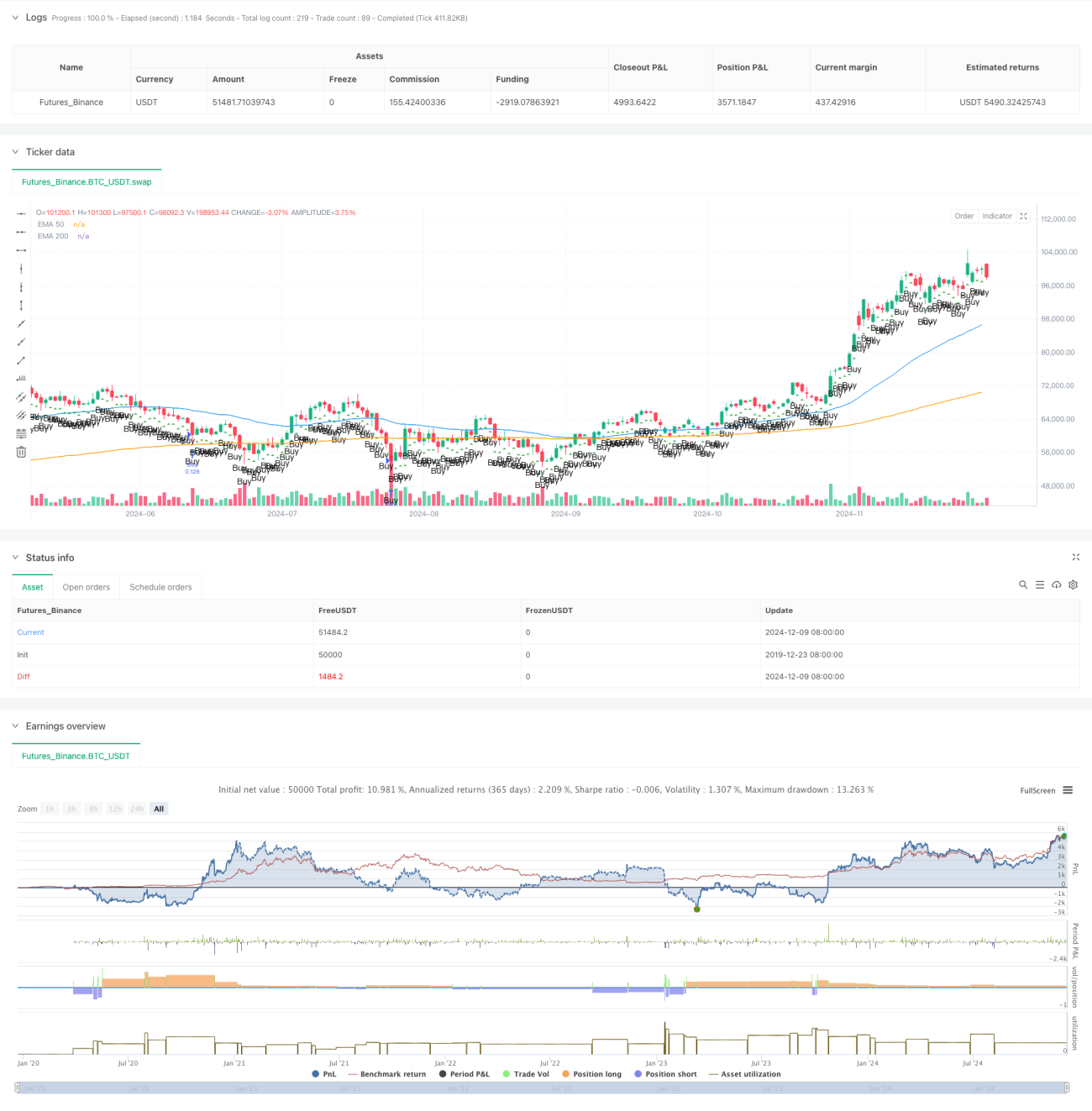

Se trata de una estrategia de seguimiento de tendencia basada en la ruptura de soporte con ATR dinámico. La estrategia combina el sistema de medias móviles EMA, el indicador de volatilidad ATR y el concepto de dinero inteligente (SMC) para capturar las tendencias del mercado. Mediante el cálculo dinámico del tamaño de la posición y de los niveles de stop loss y take profit, logra una buena gestión del riesgo.

Principio de la estrategia

La estrategia se basa principalmente en los siguientes componentes clave:

- Utilizar el sistema de medias móviles EMA de 50 y 200 periodos para confirmar la dirección de la tendencia del mercado.

- Aprovechar el indicador ATR para ajustar dinámicamente el stop loss y el objetivo de ganancias.

- Analizar los bloques de órdenes (Order Block) y las zonas de desequilibrio (Imbalance Zone) para encontrar los mejores puntos de entrada.

- Calcular automáticamente el volumen de apertura basándose en el porcentaje de riesgo de la cuenta.

- Observar el rango de fluctuación de las últimas 20 velas para determinar si el mercado se encuentra en un estado de consolidación.

Ventajas de la estrategia

- Gestión de riesgo completa: mediante el cálculo dinámico se garantiza que cada operación tenga un riesgo controlable.

- Sistema de determinación de tendencia fiable: evita operar en mercados en consolidación.

- Configuración razonable de stop loss y take profit: relación riesgo-beneficio de 1:3.

- Consideración completa de la volatilidad del mercado: se adapta a diferentes entornos de mercado.

- Código claro y bien estructurado: fácil de mantener y optimizar.

Riesgos de la estrategia

- El indicador EMA tiene un rezago, lo que puede provocar retrasos en el momento de entrada.

- En mercados con movimientos bruscos puede generar señales falsas.

- La estrategia depende de la continuidad de la tendencia; en mercados laterales podría tener un rendimiento deficiente.

- El stop loss es relativamente amplio, lo que en algunos casos podría conllevar pérdidas considerables.

Direcciones de optimización de la estrategia

- Se puede introducir el análisis de la relación precio-volumen para mejorar la precisión en la determinación de la tendencia.

- Se puede agregar un indicador de sentimiento del mercado para optimizar el momento de entrada.

- Considere añadir un análisis de múltiples marcos temporales para mejorar la estabilidad del sistema.

- Se pueden refinar los criterios de identificación de los bloques de órdenes y las zonas de desequilibrio.

- Optimizar el método de stop loss, considerando el uso de stop loss dinámico.

Conclusión

Esta estrategia constituye un sistema de seguimiento de tendencia bastante completo, que mejora la estabilidad de las operaciones mediante una gestión de riesgo razonable y la confirmación de múltiples señales. Aunque presenta cierto rezago, en general es un sistema de trading fiable. Se recomienda realizar una validación retrospectiva exhaustiva antes de usarlo en operaciones reales, y ajustar los parámetros según el instrumento de trading y las condiciones del mercado.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// TradingView Pine Script strategy for Smart Money Concept (SMC)

//@version=5

strategy("Smart Money Concept Strategy", overlay=true, default_qty_type=strategy.fixed, default_qty_value=100)

- 1