Sistema de seguimiento de señales de trading cuantitativo y optimización de estrategias de salida diversificadas

Resumen

Esta estrategia es un sistema de trading cuantitativo basado en señales de LuxAlgo® e indicadores superpuestos. Principalmente abre posiciones largas capturando condiciones de alerta personalizadas y gestiona las posiciones mediante múltiples señales de salida. El sistema adopta un diseño modular que permite combinar diversas condiciones de salida, incluyendo un trailing stop inteligente, confirmación de reversión de tendencia y stops porcentuales tradicionales. Además, el sistema permite agregar posiciones sobre las existentes, lo que brinda una mayor flexibilidad en la gestión del capital.

Principio de la estrategia

La lógica central de la estrategia comprende las siguientes partes clave:

- Sistema de señales de entrada: se activa una señal de entrada larga mediante condiciones de alerta personalizadas de LuxAlgo®.

- Gestión de adición de posiciones: opcionalmente, se puede habilitar la función de agregar posiciones sobre las ya existentes.

- Mecanismo de salida multinivel:

- Trailing stop inteligente: monitorea la relación entre el precio y la línea de trailing inteligente.

- Salida por confirmación de tendencia: incluye señales de confirmación bajista básica y mejorada.

- Señales de salida integradas: utiliza múltiples condiciones de salida propias del indicador.

- Stop loss tradicional: admite un stop loss fijo basado en porcentaje.

- Gestión del ventana temporal: ofrece una función flexible para establecer el rango de fechas de backtesting.

Ventajas de la estrategia

- Gestión de riesgos sistematizada: mediante un mecanismo de salida multinivel, se controla eficazmente el riesgo a la baja.

- Gestión flexible de posiciones: admite múltiples estrategias de adición y reducción de posiciones, ajustables dinámicamente según las condiciones del mercado.

- Alta personalización: el usuario puede combinar libremente diferentes condiciones de salida para crear un sistema de trading a medida.

- Diseño modular: cada módulo funcional es relativamente independiente, facilitando el mantenimiento y la optimización.

- Soporte completo de backtesting: proporciona parámetros detallados de backtesting y admite la validación con datos históricos.

Riesgos de la estrategia

- Riesgo de dependencia de señales: la estrategia depende en gran medida de la calidad de las señales del indicador LuxAlgo®.

- Riesgo de adaptabilidad al entorno de mercado: el rendimiento de la estrategia puede variar significativamente en diferentes condiciones de mercado.

- Riesgo de sensibilidad a parámetros: la combinación de múltiples condiciones de salida puede provocar salidas prematuras o pérdida de oportunidades.

- Riesgo de liquidez: en condiciones de baja liquidez, la ejecución de entradas y salidas puede verse afectada.

- Riesgo de implementación técnica: es necesario garantizar el funcionamiento estable del indicador y la estrategia para evitar fallos técnicos.

Direcciones de optimización de la estrategia

- Optimización del sistema de señales:

- Incorporar más indicadores técnicos para la confirmación de señales.

- Desarrollar mecanismos de ajuste adaptativo de umbrales de señal.

- Mejora del control de riesgos:

- Agregar un mecanismo de stop loss adaptativo a la volatilidad.

- Desarrollar un sistema dinámico de gestión de posiciones.

- Optimización del rendimiento:

- Mejorar la eficiencia computacional para reducir el consumo de recursos.

- Refinar la lógica de procesamiento de señales para disminuir la latencia.

- Ampliación de funcionalidades:

- Incorporar más herramientas de análisis del entorno de mercado.

- Desarrollar un marco de optimización de parámetros más flexible.

Resumen

Esta estrategia ofrece una solución completa para el trading cuantitativo al combinar señales de alta calidad de LuxAlgo® con un sistema de gestión de riesgos multinivel. Su diseño modular y opciones de configuración flexibles le otorgan una gran adaptabilidad y escalabilidad. Aunque existen algunos riesgos inherentes, mediante la optimización y el perfeccionamiento continuos, el rendimiento general de la estrategia aún tiene un amplio margen de mejora. Se recomienda que los usuarios presten atención a los cambios en el entorno del mercado en aplicaciones reales, ajusten oportunamente los parámetros y mantengan un monitoreo constante de los riesgos.

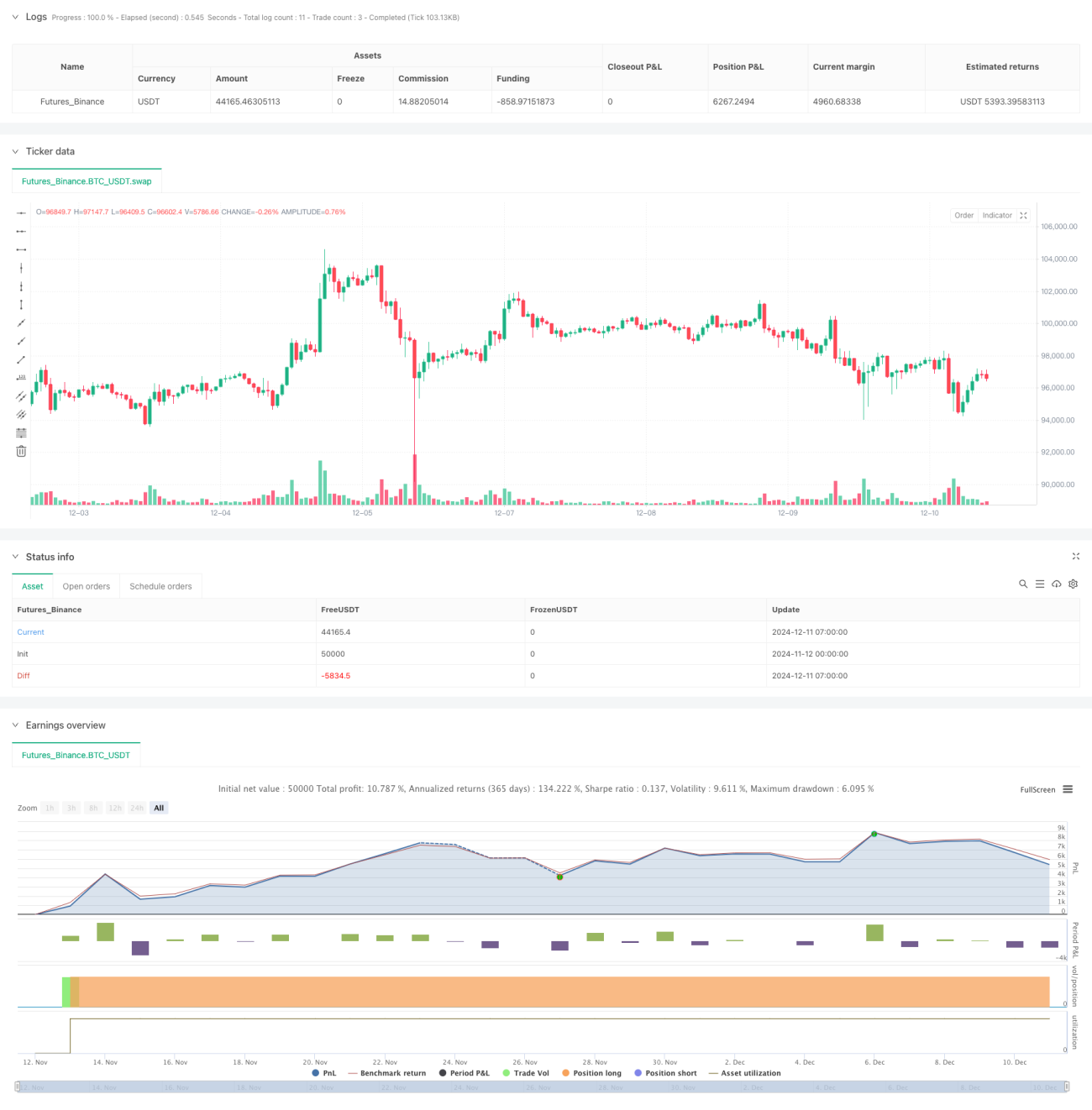

/*backtest

start: 2024-11-12 00:00:00

end: 2024-12-11 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

// This strategy is NOT from the LuxAlgo® developers. We created this to compliment their hard work. No association with LuxAlgo® is intended nor implied.

- 1