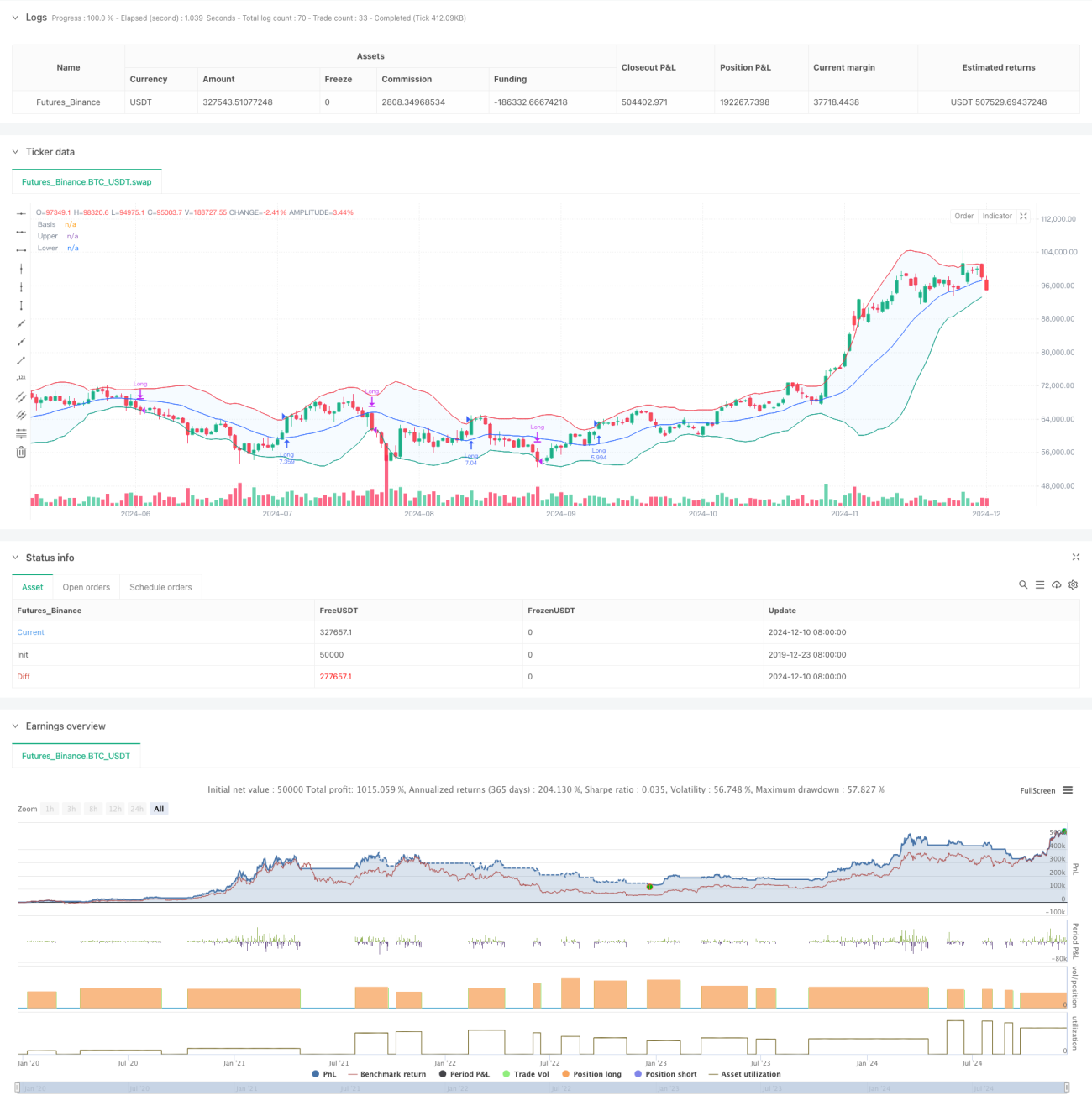

Resumen

Esta estrategia es un sistema de trading de ruptura de momentum basado en las Bandas de Bollinger, que captura principalmente oportunidades de tendencia a través de la relación entre el precio y la banda superior de Bollinger. La estrategia emplea un mecanismo de selección de tipo de media móvil adaptativa, combinada con un canal de desviación estándar para identificar las características de la volatilidad del mercado, siendo especialmente adecuada para entornos de mercado con alta volatilidad.

Principio de la Estrategia

La lógica central de la estrategia se basa en los siguientes elementos clave:

- Utilizar una media móvil personalizable (incluyendo SMA, EMA, SMMA, WMA, VWMA) para calcular la banda media de Bollinger.

- Determinar dinámicamente la posición de las bandas superior e inferior mediante un múltiplo de la desviación estándar (por defecto 2.0).

- Entrar en largo cuando el precio supera la banda superior, indicando la formación de una ruptura alcista fuerte.

- Salir de la posición cuando el precio cae por debajo de la banda inferior, señalando que la tendencia alcista podría haber terminado.

- El sistema incorpora consideraciones sobre costos de transacción (0.1%) y deslizamiento (3 ticks), lo que lo hace más acorde con el entorno real de trading.

Ventajas de la Estrategia

- Alta adaptabilidad: al ofrecer múltiples tipos de medias móviles, la estrategia puede adaptarse a diferentes condiciones del mercado.

- Control de riesgos sólido: al utilizar la banda inferior de Bollinger como punto de stop loss, proporciona un control de riesgos claro.

- Gestión de capital razonable: emplea una gestión basada en el porcentaje de la posición, evitando los riesgos derivados del uso de un número fijo de contratos.

- Consideración exhaustiva de costos de transacción: incluye comisiones y deslizamiento, por lo que los resultados del backtest se acercan más a la realidad.

- Flexibilidad en marcos temporales: permite seleccionar un rango de tiempo de transacción específico mediante la configuración de parámetros.

Riesgos de la Estrategia

- Riesgo de falsas rupturas: en mercados laterales pueden aparecer señales de ruptura falsas con frecuencia.

Solución: se pueden agregar indicadores de confirmación o un mecanismo de entrada retardada. - Riesgo de reversión de tendencia: en caso de una reversión repentina en un mercado con tendencia fuerte, podrían generarse pérdidas significativas.

Solución: se puede añadir un filtro de fortaleza de tendencia. - Sensibilidad a parámetros: diferentes combinaciones de parámetros pueden dar lugar a variaciones considerables en el rendimiento de la estrategia.

Solución: es necesario realizar una optimización exhaustiva de parámetros y pruebas de robustez.

Direcciones de Optimización de la Estrategia

- Introducir indicadores de fortaleza de tendencia:

- Se puede agregar ADX o indicadores similares para filtrar señales en mercados con tendencia débil.

- Esto ayuda a reducir las pérdidas causadas por falsas rupturas.

- Optimizar el mecanismo de stop loss:

- Se puede implementar un stop loss dinámico, como un trailing stop.

- Ayuda a obtener mayores ganancias cuando la tendencia se mantiene.

- Añadir filtros de transacciones:

- Señales de confirmación basadas en el volumen.

- Evitar operar en entornos de baja liquidez.

- Mejorar el mecanismo de entrada:

- Se puede agregar un mecanismo de entrada en retrocesos.

- Ayuda a obtener un mejor precio de entrada.

Resumen

Se trata de una estrategia de seguimiento de tendencia bien diseñada y con una lógica clara. Captura el momentum del mercado mediante las propiedades dinámicas de las Bandas de Bollinger y cuenta con un buen mecanismo de control de riesgos. La estrategia es altamente personalizable y, mediante el ajuste de parámetros, puede adaptarse a diferentes entornos de mercado. Se recomienda realizar una optimización exhaustiva de parámetros y una validación mediante backtesting antes de su aplicación en trading real, así como incorporar las direcciones de optimización sugeridas para mejorar la estrategia.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-11 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Demo GPT - Bollinger Bands", overlay=true, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.1, slippage=3, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Inputs- 1