Se trata de una estrategia de trading de impulso integral basada en indicadores de cruce de múltiples medias móviles e indicadores de precio-volumen. Esta estrategia genera señales de trading utilizando la combinación de múltiples indicadores como el cruce de medias móviles exponenciales (EMA) rápidas y lentas, el precio promedio ponderado por volumen (VWAP) y la Súper Tendencia (SuperTrend), junto con condiciones como ventanas de tiempo de negociación intradiaria y rangos de cambio de precio para controlar la entrada y salida.

Principio de la estrategia

La estrategia utiliza EMA de 5 y 13 períodos como el principal indicador de tendencia. Cuando la EMA rápida cruza por encima de la EMA lenta y el precio de cierre está por encima del VWAP, se activa una señal larga; cuando la EMA rápida cruza por debajo de la EMA lenta y el precio de cierre está por debajo del VWAP, se activa una señal corta. Además, se introduce el indicador SuperTrend como base para la confirmación de tendencia y el stop loss. La estrategia establece diferentes condiciones de entrada para distintos días de negociación, incluyendo la variación del precio con respecto al cierre del día anterior, el rango de fluctuación entre el máximo y mínimo del día, etc.

Ventajas de la estrategia

- La combinación de múltiples indicadores técnicos mejora la fiabilidad de las señales de trading.

- Condiciones de entrada diferenciadas para distintos días de negociación, adaptándose mejor a las características del mercado.

- Mecanismo dinámico de take profit y stop loss, que permite controlar el riesgo de manera efectiva.

- Restricción de ventanas de tiempo intradiarias para evitar el riesgo en períodos de alta volatilidad.

- Restricciones basadas en máximos/mínimos previos y rangos de fluctuación de precio reducen el riesgo de comprar en techos o vender en suelos.

Riesgos de la estrategia

- Pueden aparecer señales falsas en mercados con movimientos rápidos.

- Puede haber rezago en las primeras etapas de una reversión de tendencia.

- La optimización de parámetros puede conllevar riesgo de sobreajuste.

- Los costos de transacción pueden afectar la rentabilidad de la estrategia.

- En períodos de alta volatilidad del mercado, pueden producirse retrocesos significativos.

Direcciones de optimización

- Se podría considerar la incorporación de indicadores de análisis de volumen para confirmar la fuerza de la tendencia.

- Optimizar la configuración de parámetros para diferentes días de negociación, mejorando la adaptabilidad de la estrategia.

- Añadir más indicadores de sentimiento del mercado para mejorar la precisión de las predicciones.

- Perfeccionar el mecanismo de take profit y stop loss para aumentar la eficiencia en el uso del capital.

- Considerar la inclusión de indicadores de volatilidad para optimizar la gestión del tamaño de la posición.

Resumen

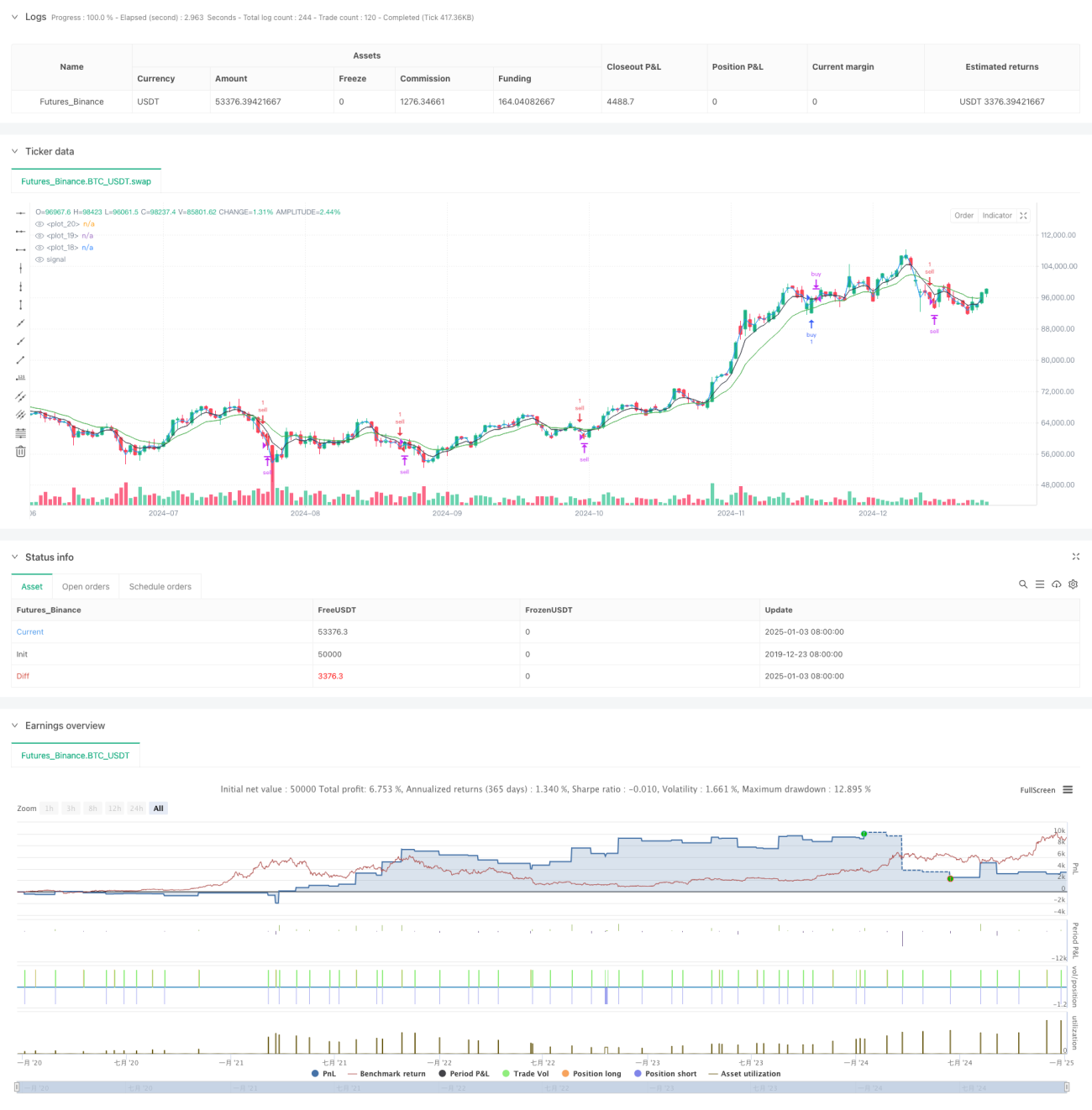

Esta estrategia combina el seguimiento de tendencias con el trading de impulso mediante el uso integral de múltiples indicadores técnicos. Su diseño considera la diversidad del mercado, adoptando reglas de trading diferenciadas para distintos días de negociación. Con un estricto control de riesgos y un mecanismo flexible de take profit y stop loss, la estrategia demuestra un buen valor práctico. En el futuro, se puede mejorar su estabilidad y rentabilidad incorporando más indicadores técnicos y optimizando la configuración de parámetros.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=6

strategy("S1", overlay=true)

fastEMA = ta.ema(close, 5)- 1