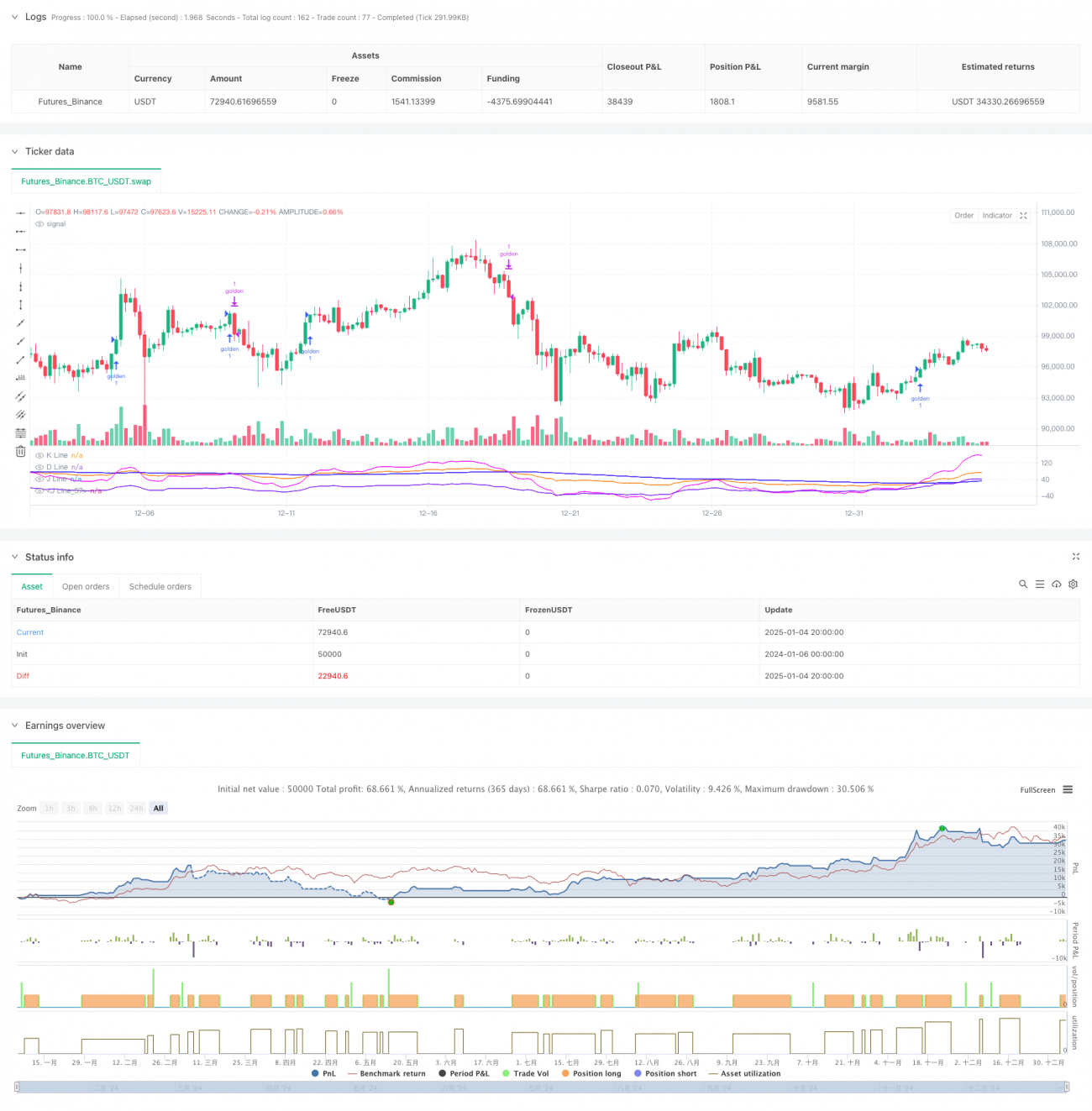

Resumen

Esta estrategia es un sistema de trading avanzado basado en el indicador KDJ, que captura las tendencias del mercado mediante un análisis profundo de los patrones de cruce entre las líneas K, D y J. El sistema integra un algoritmo de suavizado personalizado BCWSMA, mejorando la fiabilidad de las señales mediante el cálculo optimizado del oscilador estocástico. Incorpora un estricto mecanismo de control de riesgos, incluyendo funciones de stop loss fijo y trailing stop, para lograr una gestión de capital sólida.

Principio de la Estrategia

La lógica central de la estrategia se basa en los siguientes elementos clave:

- Utiliza el algoritmo personalizado BCWSMA (media móvil ponderada) para calcular el indicador KDJ, mejorando la suavidad y estabilidad del indicador.

- Mediante el cálculo del RSV (valor estocástico inmaduro), convierte los precios en valores dentro del rango 0-100, reflejando mejor la posición del precio entre los máximos y mínimos.

- Diseña un mecanismo único de verificación cruzada entre la línea J y la línea J5 (indicador derivado), aumentando la precisión de las señales de trading mediante múltiples confirmaciones.

- Establece un mecanismo de confirmación de tendencia basado en la persistencia, que requiere que la línea J se mantenga por encima de la línea D durante 3 días consecutivos para validar la tendencia.

- Integra un sistema compuesto de control de riesgos que combina stop loss porcentual y trailing stop.

Ventajas de la Estrategia

- Mecanismo avanzado de generación de señales: mediante la verificación cruzada de múltiples indicadores técnicos, reduce significativamente el impacto de las señales falsas.

- Control de riesgos completo: emplea un control de riesgos de múltiples niveles, incluyendo stop loss fijo y trailing stop, gestionando eficazmente el riesgo a la baja.

- Alta flexibilidad de parámetros: los parámetros clave como el período KDJ y el coeficiente de suavizado de señales se pueden ajustar según las condiciones del mercado.

- Alta eficiencia computacional: utiliza el algoritmo optimizado BCWSMA, reduciendo la complejidad de cálculo y mejorando la eficiencia de ejecución de la estrategia.

- Buena adaptabilidad: puede adaptarse a diferentes entornos de mercado, optimizando el rendimiento de la estrategia mediante el ajuste de parámetros.

Riesgos de la Estrategia

- Riesgo de mercado lateral: en mercados laterales o de rango, puede generar señales falsas frecuentes, aumentando los costos de trading.

- Riesgo de rezago: debido al uso de suavizado de medias móviles, las señales pueden presentar cierto retraso.

- Sensibilidad a los parámetros: el rendimiento de la estrategia es sensible a la configuración de parámetros; una configuración inadecuada puede reducir significativamente la efectividad.

- Dependencia del entorno de mercado: en ciertas condiciones de mercado específicas, el rendimiento de la estrategia puede no ser óptimo.

Direcciones de Optimización

- Optimización del filtro de señales: se pueden incorporar indicadores auxiliares como volumen y volatilidad para mejorar la fiabilidad de las señales.

- Ajuste dinámico de parámetros: ajustar dinámicamente los parámetros KDJ y los parámetros de stop loss según la volatilidad del mercado.

- Identificación del entorno de mercado: añadir un módulo de juicio del entorno de mercado para aplicar diferentes estrategias en distintas condiciones.

- Refuerzo del control de riesgos: agregar medidas adicionales como control de drawdown máximo y límite de tiempo de posición.

- Optimización del rendimiento: mejorar aún más el algoritmo BCWSMA para aumentar la eficiencia computacional.

Conclusión

Esta estrategia construye un sistema de trading completo mediante una combinación innovadora de indicadores técnicos y un estricto control de riesgos. Su principal fortaleza radica en el mecanismo de confirmación de señales múltiples y el sistema integral de gestión de riesgos, aunque también es importante prestar atención a la optimización de parámetros y la adaptabilidad al entorno del mercado. Con una optimización y mejora continuas, la estrategia tiene el potencial de mantener un rendimiento estable en diferentes condiciones de mercado.

- 1