Estrategia de trading cuantitativo multi-temporal basada en RSI suavizado por EMA y stop-loss/take-profit dinámico con ATR

Resumen

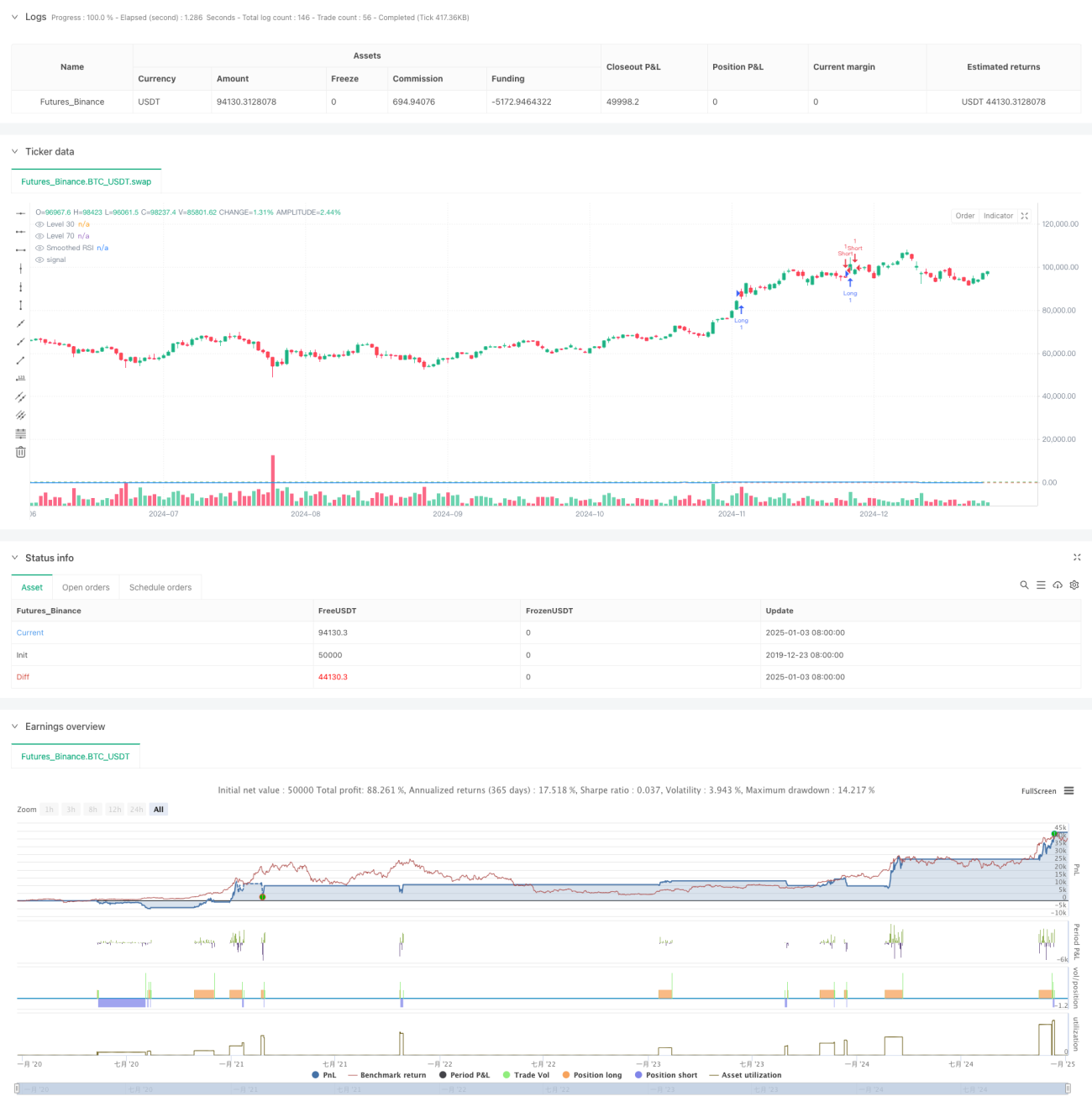

Esta estrategia es un sistema de trading cuantitativo integral basado en el Índice de Fuerza Relativa (RSI), la Media Móvil Exponencial (EMA) y el Rango Verdadero Promedio (ATR). Utiliza la EMA para suavizar el RSI, genera señales de trading con la ruptura de niveles clave del RSI y emplea el ATR para establecer dinámicamente niveles de stop loss y take profit, logrando un control eficaz del riesgo. Además, incluye funciones de conteo y registro de señales de trading, lo que facilita el backtesting y la optimización de la estrategia.

Principio de la Estrategia

La lógica central de la estrategia consta de las siguientes partes clave:

- Utiliza el RSI de 14 períodos para evaluar las condiciones de sobrecompra/sobreventa del mercado.

- Suaviza el RSI mediante EMA para reducir señales falsas.

- Genera señales de trading cuando el RSI supera los niveles clave de 70 y 30.

- Usa el ATR para calcular dinámicamente las posiciones de stop loss y take profit, mejorando la flexibilidad en la gestión del riesgo.

- Establece una tabla de conteo de señales de trading que registra la información de cada operación.

Ventajas de la Estrategia

- Alta suavidad de señales: Al suavizar el RSI con EMA, reduce eficazmente la interferencia de falsas rupturas.

- Control de riesgo completo: Emplea un esquema de stop loss dinámico basado en ATR, que se adapta automáticamente a la volatilidad del mercado.

- Mecanismo de trading bidireccional: Soporta operaciones tanto en largo como en corto, aprovechando las oportunidades del mercado.

- Parámetros ajustables: Todos los parámetros clave son personalizables, facilitando la optimización según las características del mercado.

- Monitoreo visual: Registra las señales de trading en una tabla, facilitando el monitoreo y el análisis de backtesting.

Riesgos de la Estrategia

- Riesgo de falsa ruptura del RSI: Incluso después del suavizado con EMA, el RSI puede generar señales de ruptura falsas.

- Stop loss insuficiente del ATR: En condiciones de alta volatilidad, un multiplicador del ATR inadecuado puede resultar en stops demasiado amplios o ajustados.

- Riesgo de sobreoptimización: La optimización excesiva de los parámetros puede llevar a un sobreajuste de la estrategia.

- Dependencia del entorno de mercado: El rendimiento puede diferir significativamente en mercados con tendencia frente a mercados laterales.

Direcciones de Optimización de la Estrategia

- Introducir análisis de múltiples marcos temporales: Combinar señales de RSI de plazos más largos para confirmar las operaciones.

- Optimizar el mecanismo de stop loss: Considerar ajustar dinámicamente el multiplicador del ATR con niveles de soporte/resistencia.

- Añadir juicio del entorno de mercado: Incorporar indicadores de tendencia y ajustar los parámetros de la estrategia según las condiciones del mercado.

- Mejorar el filtrado de señales: Considerar agregar indicadores auxiliares como el volumen para filtrar señales de ruptura falsas.

- Implementar gestión de posición: Ajustar dinámicamente el tamaño de la posición según la fuerza de la señal y la volatilidad del mercado.

Conclusión

Esta estrategia construye un sistema de trading cuantitativo completo combinando tres indicadores técnicos clásicos: RSI, EMA y ATR. Muestra una gran practicidad en la generación de señales, el control de riesgos y la ejecución de operaciones. Mediante una optimización y mejora continuas, la estrategia tiene el potencial de lograr un rendimiento estable en el trading real. Sin embargo, el usuario debe tener en cuenta el impacto del entorno de mercado en el rendimiento de la estrategia, configurar los parámetros de manera razonable y garantizar una gestión de riesgos adecuada.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("RSI Trading Strategy with EMA and ATR Stop Loss/Take Profit", overlay=true)

length = input.int(14, minval=1, title="RSI Length")

src = input(close, title="Source")- 1