Estrategia de trading piramidal dinámica con SuperTrend multiperíodo

Resumen

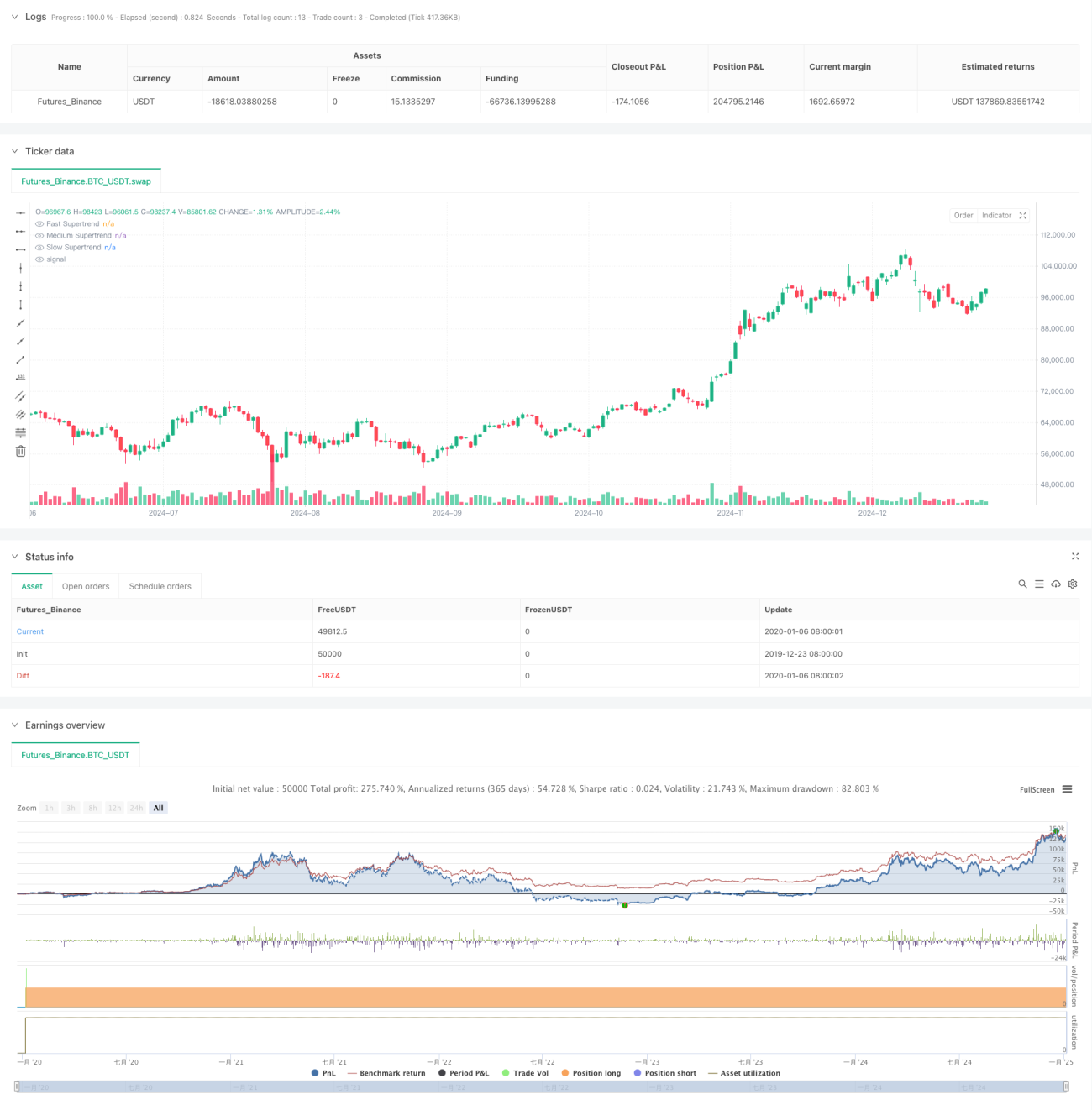

Esta es una estrategia de trading piramidal basada en múltiples indicadores Supertrend. Identifica oportunidades de trading de alta probabilidad configurando tres indicadores Supertrend con diferentes períodos y multiplicadores. La estrategia emplea un método dinámico de acumulación piramidal, permitiendo hasta tres entradas, combinado con stops dinámicos y condiciones de salida flexibles para maximizar beneficios y controlar riesgos.

Principio de la estrategia

La estrategia utiliza tres indicadores Supertrend con diferentes parámetros: rápido, medio y lento. Las señales de entrada se basan en el cruce y la dirección de tendencia de estos tres indicadores, aplicando una acumulación piramidal de tres capas: la primera capa entra cuando el indicador rápido está hacia abajo, el medio hacia arriba y el lento hacia abajo; la segunda capa entra mediante ruptura cuando tanto el rápido como el medio están hacia abajo; la tercera capa entra mediante ruptura cuando el precio alcanza un nuevo máximo. La salida utiliza mecanismos múltiples como stop dinámico, stop por precio promedio y reversión de tendencia general.

Ventajas de la estrategia

- El mecanismo de confirmación múltiple mejora la precisión de las operaciones.

- La acumulación piramidal puede amplificar significativamente las ganancias en tendencias.

- El stop dinámico protege las ganancias y da espacio suficiente para que la tendencia se desarrolle.

- El mecanismo de salida flexible se adapta bien a diferentes entornos de mercado.

- Utiliza control de tamaño de posición basado en porcentaje, adaptable a diferentes capitales.

Riesgos de la estrategia

- En mercados laterales puede generar frecuentes señales falsas.

- La acumulación piramidal puede causar grandes retrocesos en caso de reversión repentina de tendencia.

- Los múltiples indicadores pueden provocar retraso en las señales.

- La optimización de parámetros conlleva riesgo de sobreajuste.

Se recomienda una estricta gestión de capital y validación mediante backtesting para controlar estos riesgos.

Direcciones de optimización de la estrategia

- Incorporar un filtro de entorno de mercado para ajustar parámetros dinámicamente según la volatilidad.

- Optimizar el intervalo de acumulación y la proporción de asignación de posiciones.

- Introducir más indicadores técnicos para filtrar señales falsas.

- Desarrollar un mecanismo de parámetros adaptativos para cambios de mercado.

- Mejorar el mecanismo de salida, considerando agregar objetivos de beneficio y stops por tiempo.

Conclusión

Esta estrategia captura oportunidades de tendencia mediante múltiples indicadores Supertrend y acumulación piramidal, combinando stops dinámicos y mecanismos de salida flexibles para controlar el riesgo. Aunque tiene ciertas limitaciones, mediante optimización continua y un estricto control de riesgos, posee un buen valor práctico en operaciones reales.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('4Vietnamese 3x Supertrend', overlay=true, max_bars_back=1000, initial_capital = 10000000000, slippage = 2, commission_type = strategy.commission.percent, commission_value = 0.013, default_qty_type=strategy.percent_of_equity, default_qty_value = 33.33, pyramiding = 3, margin_long = 0, margin_short = 0)

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////- 1