Visión general

Esta estrategia es un sistema de trading compuesto basado en el Canal de Keltner y niveles dinámicos de soporte y resistencia. Analiza múltiples marcos temporales, combina medias móviles e indicadores de volatilidad para formar un marco completo de toma de decisiones de trading. El núcleo de la estrategia es identificar el momento en que el precio supera niveles técnicos clave, considerando al mismo tiempo la tendencia del mercado y la volatilidad, para capturar oportunidades de trading de alta probabilidad.

Principio de la estrategia

La estrategia utiliza un sistema de indicadores técnicos de múltiples capas para el análisis:

- Utiliza el Canal de Keltner de 21 períodos como herramienta principal de juicio de tendencia, con el ancho del canal determinado por el valor ATR.

- Calcula niveles clave de soporte y resistencia utilizando las 21 velas de la izquierda y las 8 velas de la derecha.

- Introduce una media móvil de un marco temporal superior como filtro de tendencia.

- Combina medias móviles de corto plazo (5 períodos) y largo plazo (30 períodos) para determinar el momento de entrada.

- Ajusta dinámicamente la posición del stop loss utilizando ATR.

Ventajas de la estrategia

- Indicadores técnicos multidimensionales se verifican mutuamente, reduciendo eficazmente las señales falsas.

- Los niveles dinámicos de soporte y resistencia se actualizan en tiempo real, adaptándose a los cambios del mercado.

- Filtra movimientos secundarios mediante el análisis de marcos temporales superiores.

- Ajusta de manera flexible los parámetros de stop loss según los diferentes marcos temporales.

- Utiliza gestión de posición basada en porcentajes, controlando eficazmente el riesgo.

Riesgos de la estrategia

- En mercados laterales puede generar señales de trading frecuentes.

- La verificación de múltiples indicadores puede llevar a perder algunas oportunidades de trading.

- La optimización de parámetros conlleva el riesgo de sobreajuste.

- En entornos de alta volatilidad, la posición del stop loss puede ser demasiado amplia.

- Cuando el mercado cambia bruscamente, los niveles de soporte y resistencia pueden perder validez.

Direcciones de optimización de la estrategia

- Introducir indicadores de volumen para ayudar a juzgar la validez de las rupturas.

- Agregar un módulo de análisis de volatilidad del mercado para ajustar parámetros dinámicamente.

- Optimizar el método de cálculo de los niveles de soporte y resistencia para mejorar la precisión.

- Añadir un juicio de la fuerza de la tendencia para refinar las condiciones de entrada.

- Mejorar el sistema de gestión de posición para lograr un control de riesgo más detallado.

Resumen

Esta es una estrategia de trading cuantitativa de estructura completa y lógica rigurosa. Mediante el uso combinado de indicadores técnicos de múltiples capas, asegura la fiabilidad de las señales de trading y logra un control efectivo del riesgo. La estrategia tiene una alta escalabilidad; mediante la optimización y mejora continuas, se espera que mantenga un rendimiento estable en diferentes entornos de mercado.

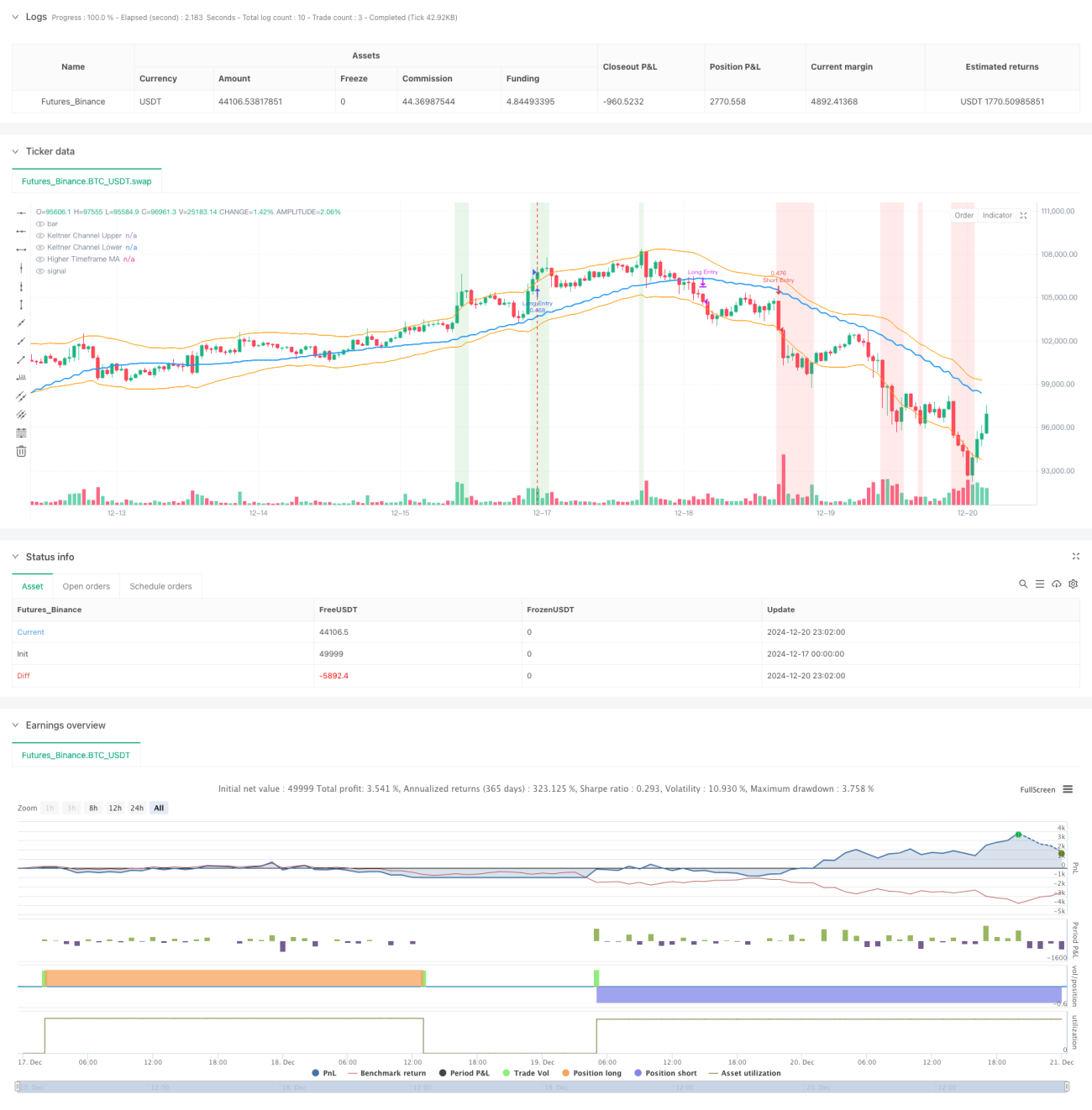

/*backtest

start: 2024-12-17 00:00:00

end: 2024-12-21 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © sathcm

//@version=5

strategy("KMS", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.05, slippage=3)- 1