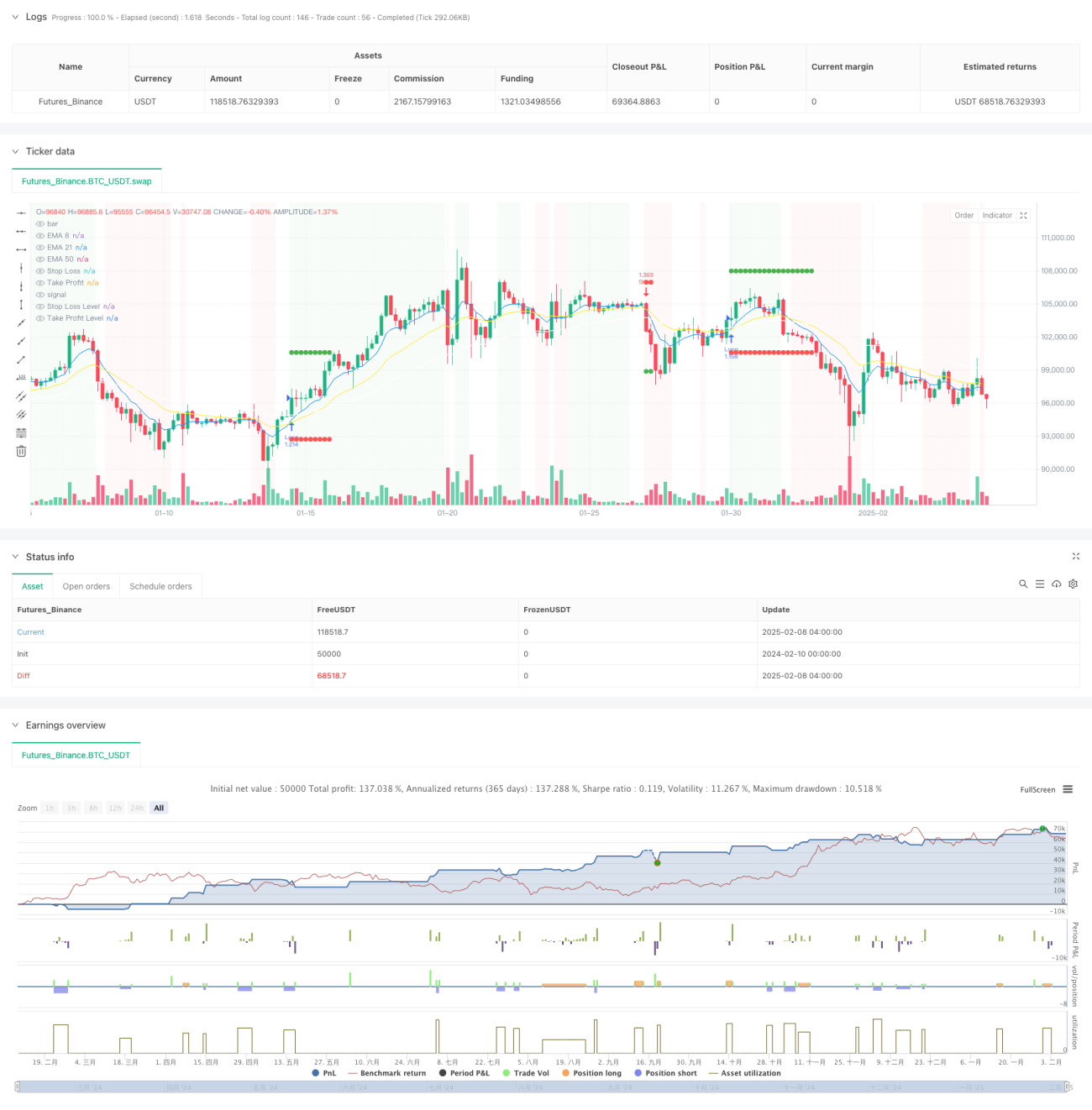

Resumen

Esta es una estrategia de seguimiento de tendencias basada en múltiples indicadores técnicos y gestión de riesgos. La estrategia combina diversos indicadores técnicos como medias móviles, el índice de fuerza relativa (RSI) y el indicador de movimiento direccional (DMI) para identificar las tendencias del mercado, y protege el capital mediante stop-loss dinámico, gestión de posiciones y límites mensuales de drawdown máximo. El núcleo de la estrategia radica en confirmar la validez de la tendencia a través de múltiples dimensiones de indicadores técnicos, mientras controla estrictamente la exposición al riesgo.

Principios de la Estrategia

La estrategia adopta un mecanismo de confirmación de tendencia de múltiples niveles:

- Utiliza medias móviles exponenciales (EMA) de períodos 8/21/50 para determinar la dirección de la tendencia.

- Emplea la línea media del canal de precios como filtro de tendencia.

- Combina el movimiento de la media móvil del RSI (período 5) dentro del rango 35-65 para filtrar falsos rompimientos.

- Confirma la fuerza de la tendencia mediante el indicador DMI (período 14).

- Utiliza el indicador de momentum (período 8) y el aumento de volumen para validar la continuidad de la tendencia.

- Implementa un stop-loss dinámico basado en ATR para controlar el riesgo.

- Aplica una gestión de posiciones con riesgo fijo, con un límite de riesgo por operación del 5% del capital inicial.

- Establece un límite máximo de drawdown mensual del 10% para evitar pérdidas excesivas.

Ventajas de la Estrategia

- La validación cruzada de múltiples indicadores técnicos mejora la precisión en la identificación de tendencias.

- El mecanismo de stop-loss dinámico controla eficazmente el riesgo de cada operación individual.

- La gestión de posiciones con riesgo fijo optimiza el uso del capital.

- El límite de drawdown mensual proporciona una protección sistemática contra el riesgo.

- La inclusión del indicador de volumen incrementa la fiabilidad de la confirmación de tendencia.

- La relación riesgo-beneficio de 2:1 mejora la rentabilidad a largo plazo.

Riesgos de la Estrategia

- El uso de múltiples indicadores puede provocar retrasos en las señales.

- En mercados laterales, puede generar señales falsas frecuentes.

- El modelo de riesgo fijo puede no ser lo suficientemente flexible ante cambios bruscos de volatilidad.

- El límite de drawdown mensual podría hacer que se pierdan oportunidades de trading importantes.

- Durante los cambios de tendencia, podría experimentar un drawdown significativo.

Direcciones de Optimización de la Estrategia

- Introducir parámetros de indicadores adaptativos para diferentes entornos de mercado.

- Desarrollar un esquema de gestión de posiciones más flexible que considere los cambios en la volatilidad del mercado.

- Agregar una evaluación cuantitativa de la fuerza de la tendencia para optimizar el momento de entrada.

- Diseñar un mecanismo de límite de riesgo mensual más inteligente.

- Incorporar un módulo de identificación del entorno de mercado para ajustar los parámetros de la estrategia según las diferentes condiciones del mercado.

Resumen

Esta estrategia establece un sistema completo de trading de seguimiento de tendencias mediante la integración de múltiples indicadores técnicos. Su ventaja radica en un marco integral de gestión de riesgos que incluye stop-loss dinámico, gestión de posiciones y control de drawdown. Aunque existe cierto riesgo de retraso en las señales, mediante optimización y mejoras, la estrategia tiene el potencial de mantener un rendimiento estable en diferentes entornos de mercado. La clave es mejorar su capacidad de adaptación al entorno del mercado sin perder la lógica central de la estrategia.

/*backtest

start: 2024-02-10 00:00:00

end: 2025-02-08 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("High Win-Rate Crypto Strategy with Drawdown Limit", overlay=true, initial_capital=10000, default_qty_type=strategy.fixed, process_orders_on_close=true)

// Moving Averages- 1