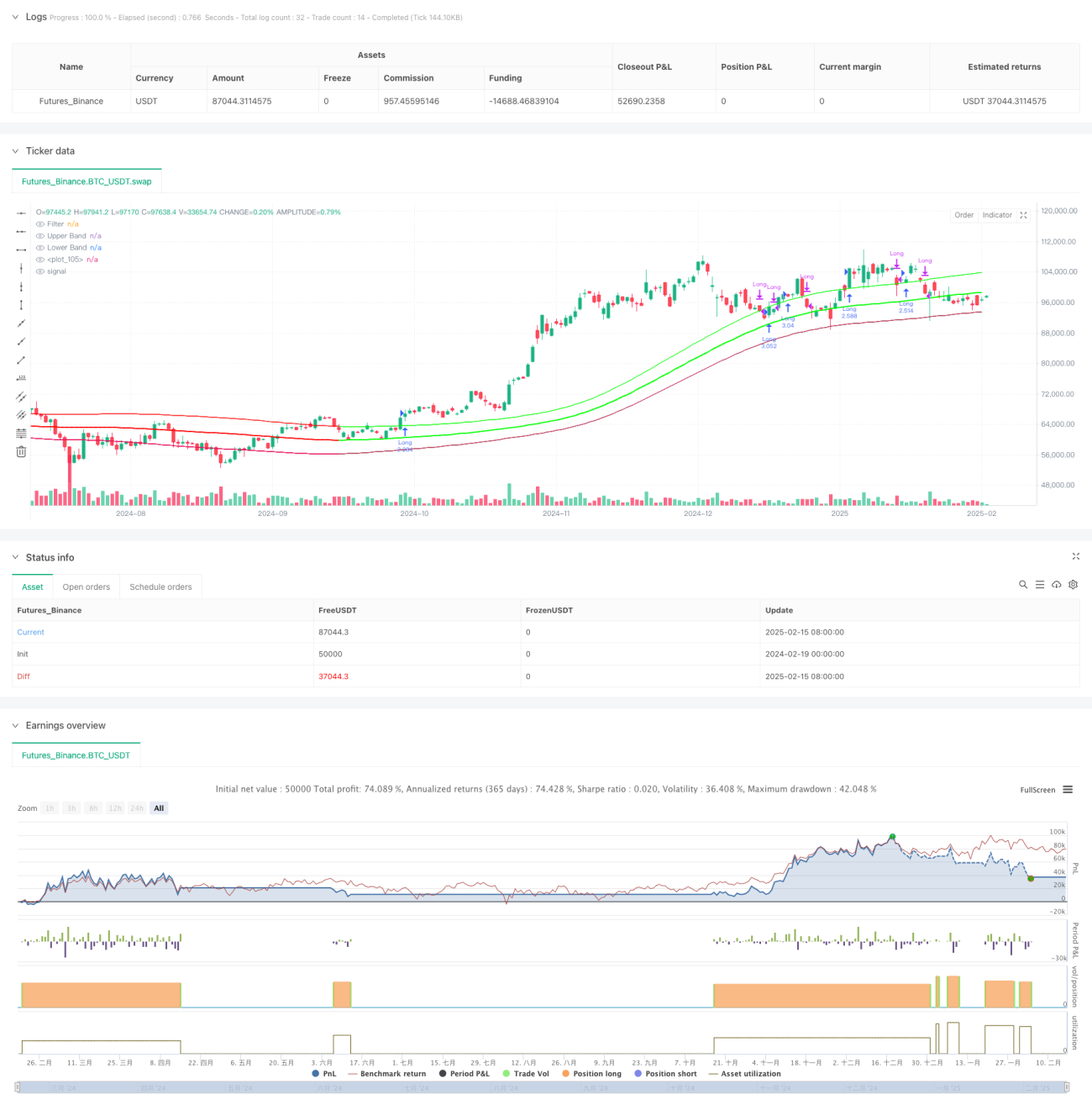

Resumen

Esta estrategia es un sistema de trading de seguimiento de tendencia basado en el filtro gaussiano y el indicador StochRSI. Utiliza un canal gaussiano para identificar la tendencia del mercado y combina las zonas de sobrecompra y sobreventa del StochRSI para optimizar los momentos de entrada. El sistema construye el canal gaussiano mediante un método de ajuste polinómico, ajustando dinámicamente las bandas superior e inferior para seguir la tendencia del precio, logrando un seguimiento preciso de la evolución del mercado.

Principio de la estrategia

El núcleo de la estrategia es un canal de precios basado en el algoritmo de filtro gaussiano. La implementación específica incluye los siguientes pasos clave:

- Utilizar la función polinómica f_filt9x para implementar un filtro gaussiano de orden 9, optimizando los polos para mejorar el efecto de filtrado.

- Calcular la línea de filtro principal y el canal de volatilidad basándose en el precio HLC3.

- Introducir el modo reducedLag para reducir el retardo del filtro y el modo fastResponse para mejorar la velocidad de respuesta.

- Utilizar las zonas de sobrecompra y sobreventa (80/20) del indicador StochRSI para determinar las señales de trading.

- Cuando el canal gaussiano está en tendencia alcista y el precio supera la banda superior, combinado con el StochRSI, se genera una señal de compra.

- Cuando el precio cae por debajo de la banda superior, se cierra la posición.

Ventajas de la estrategia

- El filtro gaussiano tiene una excelente capacidad de reducción de ruido, filtrando eficazmente el ruido del mercado.

- El ajuste polinómico permite un seguimiento suave de la tendencia, reduciendo las señales falsas.

- Soporta modos de optimización de retardo y respuesta rápida, adaptándose flexiblemente a las características del mercado.

- Combina el StochRSI para optimizar los momentos de entrada, mejorando la tasa de éxito de las operaciones.

- Utiliza un ancho de canal dinámico, adaptándose automáticamente a los cambios de volatilidad del mercado.

Riesgos de la estrategia

- El filtro gaussiano presenta cierto retardo, lo que puede provocar entradas o salidas poco oportunas.

- En mercados laterales puede generar señales de trading frecuentes, aumentando los costes de transacción.

- El StochRSI puede generar señales retardadas en determinadas condiciones del mercado.

- El proceso de optimización de parámetros es complejo y requiere reajustes según las diferentes condiciones del mercado.

- El sistema exige altos recursos computacionales, lo que puede provocar retrasos en el cálculo en tiempo real.

Direcciones de optimización de la estrategia

- Introducir un mecanismo de optimización de parámetros adaptativos para ajustar dinámicamente los parámetros según el estado del mercado.

- Añadir un módulo de identificación del entorno de mercado para utilizar diferentes combinaciones de parámetros según las condiciones.

- Optimizar el algoritmo de filtro gaussiano para reducir aún más la latencia computacional.

- Incorporar más indicadores técnicos para validación cruzada, mejorando la fiabilidad de las señales.

- Desarrollar un mecanismo de stop-loss inteligente para mejorar el control de riesgos.

Resumen

Esta estrategia logra un seguimiento efectivo de la tendencia del mercado mediante la combinación del filtro gaussiano y el StochRSI. El sistema posee una buena capacidad de reducción de ruido e identificación de tendencias, pero también presenta cierto retardo y dificultad en la optimización de parámetros. Mediante la optimización y mejora continua, esta estrategia tiene el potencial de obtener rendimientos estables en el trading real.

/*backtest

start: 2024-02-19 00:00:00

end: 2025-02-16 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Demo GPT - Gaussian Channel Strategy v3.0", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=0, default_qty_type=strategy.percent_of_equity, default_qty_value=250)

// ============================================- 1