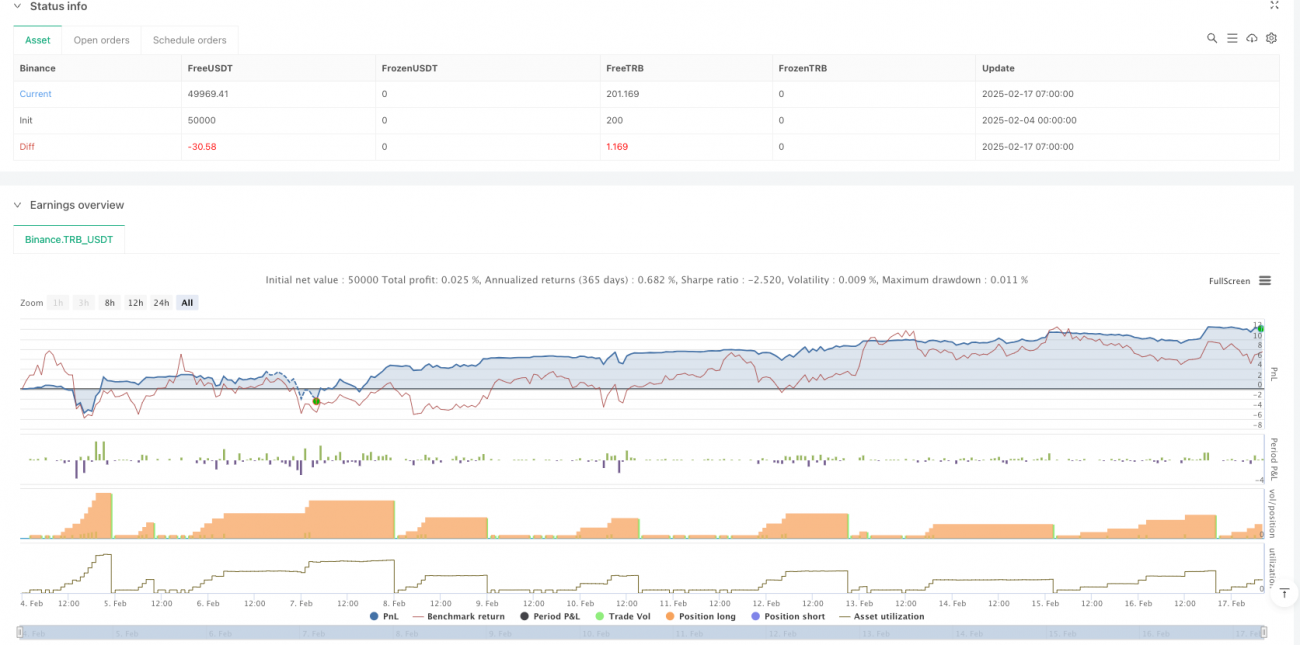

Estrategia de trading cuantitativo de criptomonedas basada en DCA dinámico

Resumen

Esta es una estrategia de trading cuantitativa diseñada específicamente para el mercado de criptomonedas, que aprovecha la alta volatilidad del mercado de criptomonedas y añade posiciones de forma dinámica durante las correcciones de precios mediante el método inteligente de promediación de costos (DCA). La estrategia opera en un marco temporal de 15 minutos, lo que permite responder eficazmente a las rápidas fluctuaciones del mercado de criptomonedas, al mismo tiempo que evita los riesgos asociados al exceso de trading.

Principio de la estrategia

La estrategia consta de cuatro módulos principales:

- Sistema de entrada inteligente: basado en el precio medio ponderado OHLC4 para la primera apertura de posición, adaptándose a la alta volatilidad del mercado de criptomonedas.

- Mecanismo dinámico de reposición: activa órdenes de seguridad durante las correcciones de precios, ampliando la cantidad de reposición a medida que aumenta la profundidad de la corrección, aprovechando al máximo la volatilidad del mercado.

- Sistema de gestión de riesgos: optimiza la relación riesgo-beneficio mediante la adición piramidal de posiciones y el ajuste flexible del apalancamiento.

- Control rápido de toma de ganancias: mecanismo de toma de ganancias diseñado para las rápidas fluctuaciones del mercado de criptomonedas, que incluye la optimización de comisiones.

Ventajas de la estrategia

- Adaptabilidad al mercado: optimizada específicamente para la alta volatilidad del mercado de criptomonedas.

- Diversificación del riesgo: reduce los riesgos repentinos del mercado de criptomonedas mediante la apertura dinámica de posiciones por lotes.

- Eficiencia en el arbitraje: aprovecha plenamente las fluctuaciones de precios del mercado de criptomonedas para obtener ganancias.

- Ejecución automatizada: compatible con API de varios exchanges de criptomonedas principales.

- Eficiencia del capital: mejora la eficiencia del uso de capital en el trading de criptomonedas mediante una gestión inteligente del apalancamiento.

Riesgos de la estrategia

- Riesgo de mercado: las fluctuaciones extremas del mercado de criptomonedas pueden provocar grandes retrocesos.

- Riesgo de liquidez: algunas criptomonedas de baja capitalización pueden enfrentar problemas de liquidez insuficiente.

- Riesgo de apalancamiento: la alta volatilidad del mercado de criptomonedas aumenta el riesgo del trading con apalancamiento.

- Riesgo técnico: depende de la estabilidad de la API del exchange y la calidad de la conexión de red.

- Riesgo regulatorio: los cambios en las políticas del mercado de criptomonedas pueden afectar la ejecución de la estrategia.

Direcciones de optimización de la estrategia

- Adaptación a la volatilidad: introducir indicadores de volatilidad propios del mercado de criptomonedas para ajustar parámetros dinámicamente.

- Sincronización entre múltiples criptomonedas: desarrollar lógica de trading conjunta para múltiples criptomonedas, dispersando el riesgo de una sola moneda.

- Filtro de sentimiento del mercado: integrar indicadores de sentimiento del mercado de criptomonedas para optimizar los puntos de entrada.

- Optimización de costos de trading: reducir costos mediante el enrutamiento inteligente y la selección de exchanges.

- Mecanismo de alerta de riesgos: establecer un sistema de alerta basado en fluctuaciones anormales del mercado.

Conclusión

Esta estrategia proporciona una solución automatizada integral para el trading de criptomonedas mediante un innovador método DCA y una gestión dinámica del riesgo. Aunque el mercado de criptomonedas presenta un alto riesgo, gracias a un cuidadoso diseño de control de riesgos y una optimización de la adaptabilidad al mercado, la estrategia puede mantener la estabilidad en la mayoría de las condiciones del mercado. Las optimizaciones futuras se centrarán en mejorar la capacidad de la estrategia para adaptarse a las particularidades del mercado de criptomonedas.

/*backtest

start: 2020-08-29 15:00:00

end: 2025-02-18 17:22:45

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"TRB_USDT"}]

*/

//@version=5

strategy('Autotrade.it DCA', overlay=true, pyramiding=999, default_qty_type=strategy.cash, initial_capital=10000, commission_value=0.02)

// Date Ranges- 1