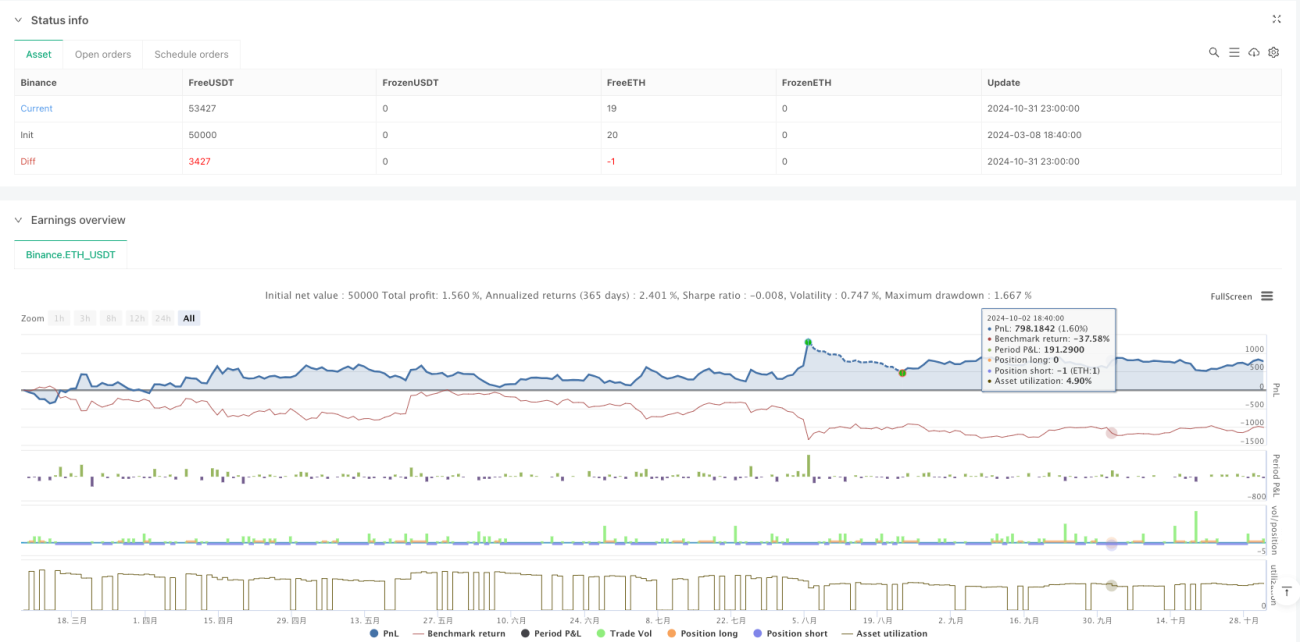

Estrategia de Trading de Momento Multidimensional Basada en Análisis Espectral Cuántico

Resumen

Esta estrategia es un innovador sistema de trading cuantitativo que integra principios de mecánica cuántica, estadística y economía. Construye un marco integral de análisis de mercado combinando la Media Móvil Simple (SMA), el análisis estadístico Z-Score, componentes de fluctuación cuántica, indicadores de impulso económico y el índice de estabilidad de Lyapunov. El núcleo de la estrategia es generar un Índice de Perspectiva de Mercado Compuesto (COI, por sus siglas en inglés) mediante la combinación ponderada de estos indicadores multidimensionales, para guiar las decisiones de trading.

Principio de la Estrategia

La estrategia se basa en cinco pilares técnicos principales:

- El módulo de análisis estadístico utiliza la SMA y la desviación estándar para calcular el Z-Score, evaluando la posición relativa del precio.

- El componente cuántico transforma el Z-Score en un oscilador, simulando las características de fluctuación de los estados cuánticos mediante funciones exponenciales y senoidales.

- El componente económico utiliza la relación logarítmica de las EMA rápidas y lentas para medir el impulso del mercado.

- El índice de Lyapunov evalúa el estado del mercado analizando la estabilidad de la combinación de los componentes cuántico y económico.

- El Índice de Perspectiva de Mercado Compuesto (COI) integra todos los componentes con diferentes pesos, formando la señal final de trading.

Ventajas de la Estrategia

- El análisis multidimensional proporciona una visión más completa del mercado, reduciendo el sesgo que podría generar un solo indicador.

- La introducción del componente cuántico aporta una perspectiva única sobre las fluctuaciones del mercado, ayudando a capturar oportunidades a corto plazo.

- La aplicación del índice de Lyapunov evalúa eficazmente la estabilidad del mercado, mejorando la capacidad de gestión de riesgos.

- El diseño ajustable de pesos permite que la estrategia se adapte de manera flexible a diferentes entornos de mercado.

- El diseño de la línea neutra del índice compuesto proporciona límites claros para las señales de trading.

Riesgos de la Estrategia

- Múltiples indicadores pueden provocar un retraso en las señales, afectando el momento de entrada.

- Una optimización excesiva de los parámetros puede conllevar el riesgo de sobreajuste.

- En mercados de alta volatilidad, el componente cuántico puede generar señales demasiado frecuentes.

- El componente económico puede generar señales engañosas en mercados laterales.

- Es necesario establecer un stop loss adecuado para controlar el riesgo.

Direcciones de Optimización de la Estrategia

- Introducir un sistema de pesos adaptativos que ajuste dinámicamente los pesos de cada componente según el entorno del mercado.

- Añadir un filtro de volatilidad para ajustar la sensibilidad de las señales durante períodos de alta volatilidad.

- Integrar indicadores de sentimiento del mercado para proporcionar señales de confirmación adicionales.

- Desarrollar un mecanismo de stop loss dinámico que ajuste el nivel de stop loss según las condiciones del mercado.

- Agregar un filtro de tiempo para evitar abrir posiciones en momentos desfavorables de trading.

Conclusión

Esta es una estrategia de trading cuantitativa innovadora que construye un marco integral de análisis de mercado mediante la fusión de teorías multidisciplinarias. Aunque existen aspectos que requieren optimización, su enfoque de análisis multidimensional ofrece una perspectiva única para la toma de decisiones de trading. Con mejoras continuas en optimización y gestión de riesgos, esta estrategia tiene el potencial de mantener un rendimiento estable en diferentes entornos de mercado.

- 1