Sistema inteligente de control de riesgos que combina una estrategia de cruce de múltiples indicadores adaptativos dinámicos con SRSI y MACD

Resumen

Esta estrategia es un sistema de trading dinámico que combina el Índice de Fuerza Relativa Estocástico (SRSI) y el MACD (Moving Average Convergence Divergence). Utiliza el indicador ATR para ajustar dinámicamente los niveles de stop-loss y take-profit, logrando una gestión inteligente del riesgo. El núcleo de la estrategia radica en generar señales de trading mediante la confirmación cruzada de múltiples indicadores técnicos, combinada con la gestión de posiciones basada en la volatilidad del mercado.

Principio de la Estrategia

La operativa de la estrategia se basa en los siguientes mecanismos centrales:

- Calcular la diferencia entre la línea K y la línea D del indicador SRSI, así como la diferencia entre la línea K y el MACD normalizado para evaluar la tendencia del mercado.

- La condición de compra requiere que se cumplan simultáneamente: la diferencia K-D sea positiva, la diferencia K-MACD sea positiva, y el MACD no esté en una tendencia bajista.

- La condición de venta requiere que se cumplan simultáneamente: la diferencia K-D sea negativa, la diferencia K-MACD sea negativa, y el MACD no esté en una tendencia alcista.

- Se utiliza el ATR multiplicado por un coeficiente de riesgo para calcular dinámicamente las distancias de stop-loss y take-profit, ajustándose de forma adaptativa según la volatilidad del mercado.

Ventajas de la Estrategia

- El mecanismo de confirmación de múltiples señales mejora significativamente la fiabilidad de las operaciones, evitando las señales falsas que podría generar un solo indicador.

- La configuración dinámica de stop-loss y take-profit se ajusta automáticamente según la volatilidad del mercado, ofreciendo una mejor relación riesgo-beneficio.

- La estrategia tiene una buena adaptabilidad, manteniendo un rendimiento estable en diferentes condiciones de mercado.

- Alta capacidad de ajuste de parámetros, permitiendo a los traders optimizarla según su tolerancia al riesgo personal.

Riesgos de la Estrategia

- En mercados laterales o de rango puede generar demasiadas señales de trading, provocando entradas y salidas frecuentes.

- El uso de múltiples indicadores puede causar un retraso en las señales, perdiendo el mejor momento de entrada en mercados de cambios rápidos.

- El ATR se calcula basándose en la volatilidad histórica, por lo que puede no adaptarse a tiempo ante cambios repentinos en la volatilidad del mercado.

- Es necesario establecer un coeficiente de riesgo adecuado; valores demasiado altos o demasiado bajos pueden afectar el rendimiento de la estrategia.

Direcciones de Optimización

- Agregar un filtro de tendencia para aplicar diferentes criterios de confirmación de señales en mercados laterales y con tendencia.

- Incorporar indicadores de volumen como confirmación auxiliar para aumentar la fiabilidad de las señales.

- Optimizar el método de cálculo de stop-loss y take-profit, considerando la combinación con niveles de soporte y resistencia.

- Integrar modelos de predicción de volatilidad del mercado para ajustar los parámetros de riesgo de forma anticipada.

- Considerar la confirmación de señales en diferentes marcos temporales para aumentar la solidez de la estrategia.

Conclusión

Esta estrategia construye un sistema de trading robusto al combinar las fortalezas del SRSI y el MACD. Su mecanismo dinámico de gestión de riesgos le otorga una buena adaptabilidad, aunque sigue siendo necesario que el trader optimice los parámetros según las condiciones reales del mercado. El éxito de la estrategia requiere un conocimiento profundo del mercado, así como una gestión adecuada de las posiciones en función de la tolerancia al riesgo personal.

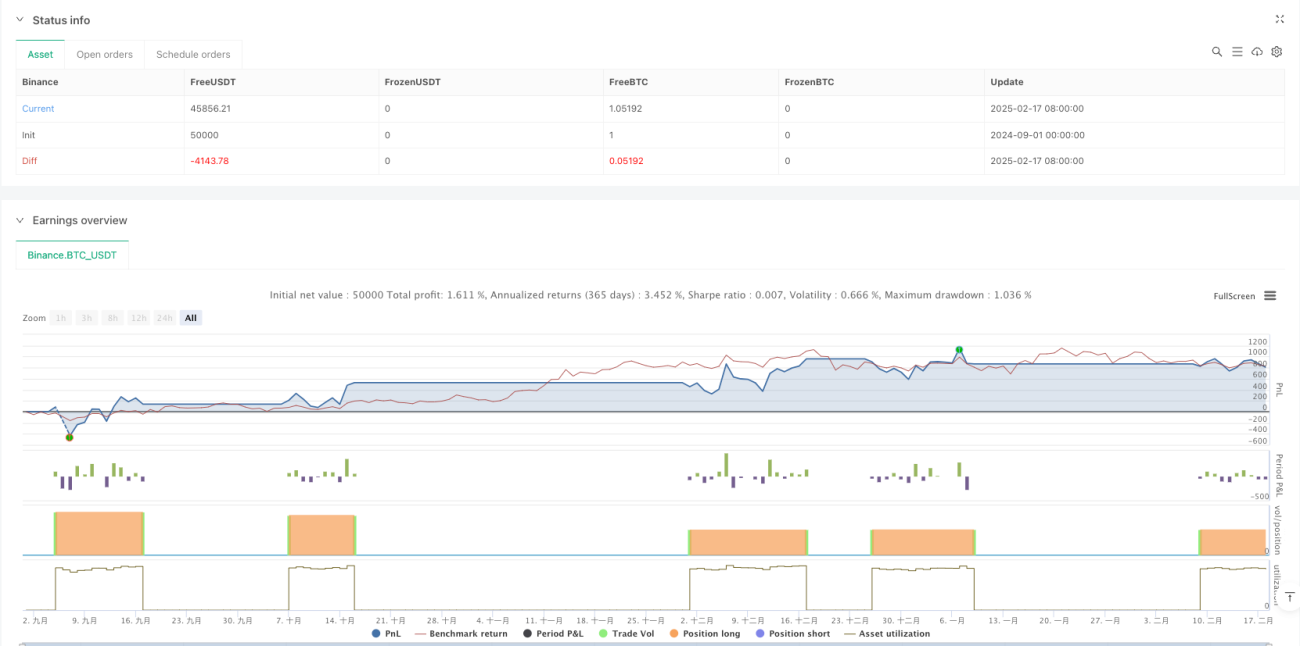

/*backtest

start: 2024-09-01 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy(title="SRSI + MACD Strategy with Dynamic Stop-Loss and Take-Profit", shorttitle="SRSI + MACD Strategy", overlay=false, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// User Inputs- 1