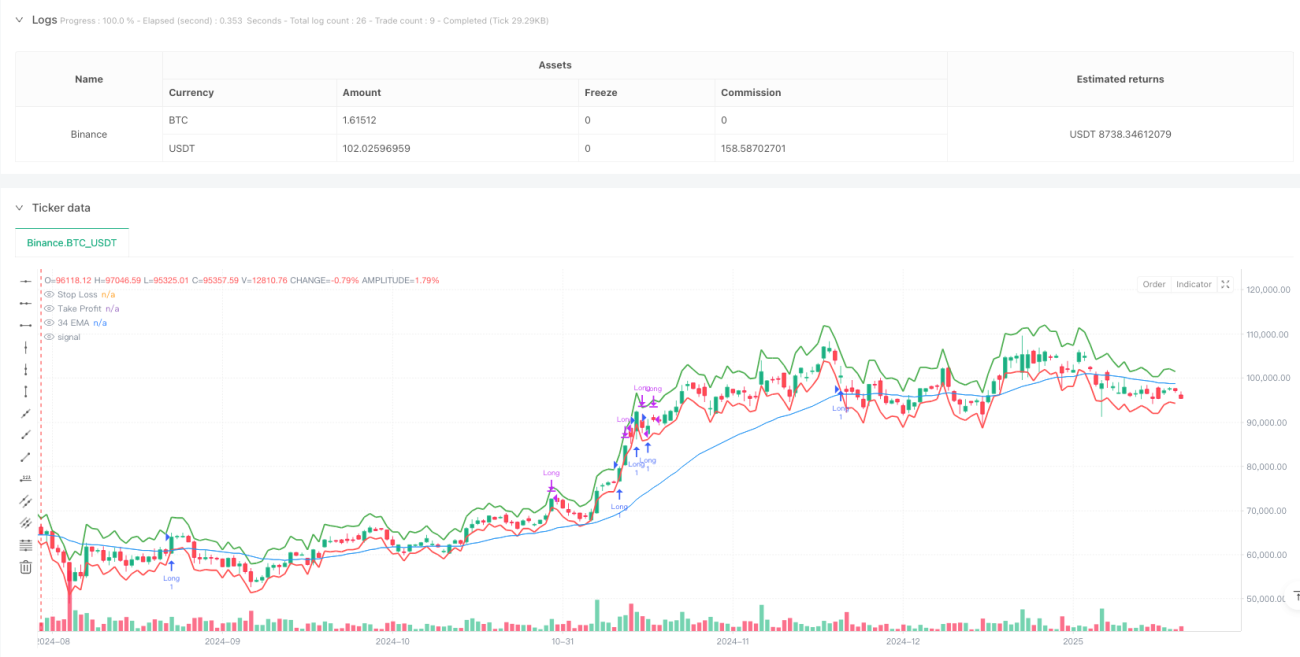

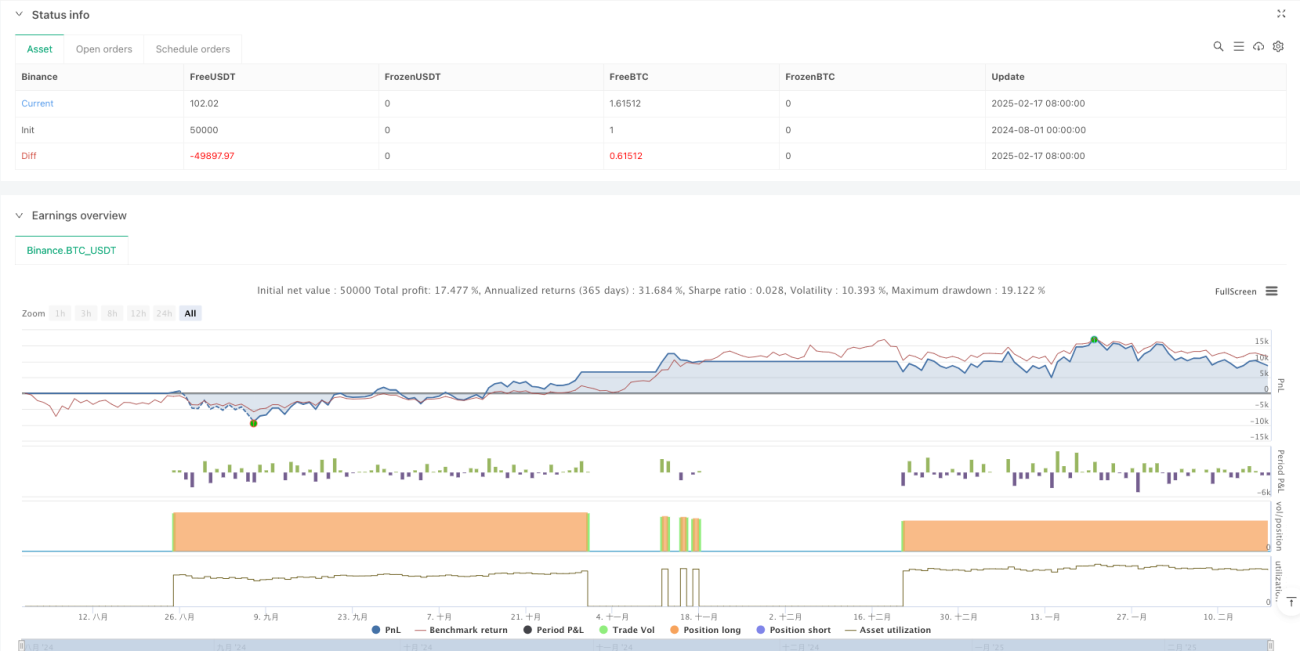

Resumen

Esta estrategia es un sistema de trading que combina seguimiento de tendencia y reversión de momento. Se basa principalmente en la media móvil exponencial de 34 períodos (EMA) para determinar la tendencia general, identifica zonas de sobrecompra y sobreventa mediante el indicador RSI, y confirma las señales de trading con patrones de velas y volumen. La estrategia utiliza un stop loss dinámico basado en ATR y toma de ganancias, adaptándose automáticamente a la volatilidad del mercado.

Principio de la Estrategia

La lógica central de la estrategia incluye los siguientes elementos clave:

- Juicio de tendencia: Utiliza la EMA de 34 períodos como indicador principal de tendencia, buscando oportunidades de compra solo cuando el precio está por encima de la EMA.

- Condición de entrada: Requiere la formación consecutiva de un patrón de velas "bajista-alcista-alcista" (una vela bajista seguida de dos velas alcistas).

- Confirmación de momento: Usa el RSI para confirmar el momento, exigiendo un valor RSI superior a 50 para indicar impulso alcista.

- Filtro de volumen: Requiere que el volumen actual sea mayor que el volumen promedio de 20 períodos, asegurando suficiente participación en el mercado.

- Gestión de riesgos: Utiliza 1.5 veces el ATR como objetivo de ganancias y 1 vez el ATR como nivel de stop loss.

Ventajas de la Estrategia

- Confirmación de múltiples señales: Al combinar tendencia, patrón, momento y volumen, se reducen eficazmente las señales falsas.

- Gestión dinámica de riesgos: El stop loss y la toma de ganancias basados en ATR se ajustan automáticamente según la volatilidad del mercado.

- Característica de seguimiento de tendencia: Garantiza operar en la dirección principal de la tendencia mediante la EMA, mejorando la tasa de aciertos.

- Parámetros flexibles: Los parámetros clave como el período de EMA, el umbral de RSI y el múltiplo de ATR son ajustables para adaptarse a diferentes entornos de mercado.

Riesgos de la Estrategia

- Riesgo de reversión de tendencia: Pueden ocurrir pérdidas consecutivas en puntos de inflexión de la tendencia.

- Riesgo de ruptura falsa: Los patrones de velas pueden generar rupturas falsas, dando lugar a señales erróneas.

- Riesgo de volatilidad del mercado: Durante períodos de alta volatilidad, el valor de ATR puede ampliarse anormalmente, afectando la configuración del stop loss.

- Sensibilidad a parámetros: Los parámetros óptimos pueden variar significativamente según el entorno del mercado.

Direcciones de Optimización

- Agregar filtro de fuerza de tendencia: Introducir el indicador ADX para medir la fuerza de la tendencia y operar solo en tendencias fuertes.

- Mejorar el mecanismo de salida: Incorporar un stop loss móvil para proteger las ganancias acumuladas.

- Optimizar el indicador de volumen: Considerar el uso de volumen relativo o indicadores de ruptura de volumen.

- Añadir filtro temporal: Incluir ventanas de horario de trading para evitar períodos de alta volatilidad.

- Clasificación del entorno de mercado: Ajustar dinámicamente los parámetros de la estrategia según las diferentes condiciones del mercado.

Conclusión

Esta estrategia construye un sistema de trading completo mediante la combinación de múltiples indicadores técnicos, ofreciendo buena adaptabilidad y escalabilidad. Su principal ventaja radica en la confirmación de señales multidimensionales y la gestión dinámica de riesgos, aunque se debe prestar atención a la optimización de parámetros y la adaptabilidad al entorno del mercado. Con una optimización y mejora continuas, esta estrategia tiene el potencial de mantener un rendimiento estable en diferentes condiciones de mercado.

- 1