Sistema de trading de seguimiento de tendencia con stop loss dinámico basado en ATR

Resumen

Esta estrategia es un sistema de seguimiento de tendencia basado en un trailing stop dinámico calculado con ATR (Average True Range). Combina una media móvil EMA como filtro de tendencia y ajusta la generación de señales mediante un parámetro de sensibilidad y el período del ATR. El sistema soporta tanto operaciones largas como cortas, e incluye un completo mecanismo de gestión de ganancias.

Principio de la estrategia

- Utiliza el indicador ATR para calcular la amplitud de la volatilidad del precio y, según el coeficiente de sensibilidad (Key Value) establecido, determina la distancia del trailing stop.

- Emplea la media móvil EMA para determinar la dirección de la tendencia del mercado: solo abre posiciones largas cuando el precio está por encima de la media, y posiciones cortas cuando está por debajo.

- Cuando el precio supera la línea de trailing stop y coincide con la dirección de la tendencia, se activa la señal de trading.

- El sistema gestiona las posiciones mediante una estrategia de obtención de beneficios por tramos:

- Cuando la ganancia es del 20%-50%, eleva el stop loss al precio de coste para proteger el capital.

- Cuando la ganancia es del 50%-80%, cierra parcialmente la posición y ajusta el stop loss más cerca.

- Cuando la ganancia es del 80%-100%, ajusta aún más el stop loss para proteger las ganancias.

- Cuando la ganancia supera el 100%, cierra toda la posición para asegurar el beneficio.

Ventajas de la estrategia

- El trailing stop dinámico permite seguir la tendencia de forma efectiva, protegiendo las ganancias sin salir prematuramente del mercado.

- El filtro de tendencia mediante EMA reduce eficazmente el riesgo de falsas rupturas.

- El mecanismo de obtención de beneficios por tramos garantiza la realización de ganancias al tiempo que da espacio suficiente para el desarrollo de la tendencia.

- Soporta operaciones tanto largas como cortas, lo que permite aprovechar las oportunidades del mercado en ambas direcciones.

- Los parámetros son altamente ajustables, adaptándose a diferentes entornos de mercado.

Riesgos de la estrategia

- En mercados laterales, puede generar operaciones frecuentes que resulten en pérdidas.

- Al inicio de una reversión de tendencia, pueden producirse grandes retrocesos.

- Una configuración incorrecta de los parámetros puede afectar el rendimiento de la estrategia.

Recomendaciones para la gestión de riesgos:

- Se recomienda utilizar la estrategia en mercados con tendencia clara.

- Elegir los parámetros con cuidado, idealmente mediante optimización con backtesting.

- Establecer un límite máximo de retroceso.

- Considerar añadir filtros de entorno de mercado.

Direcciones de optimización

- Incorporar un mecanismo de identificación del entorno de mercado para usar diferentes parámetros según las condiciones.

- Introducir indicadores auxiliares como el volumen para aumentar la fiabilidad de las señales.

- Optimizar el mecanismo de obtención de beneficios, ajustando dinámicamente los objetivos según la volatilidad.

- Añadir filtros temporales para evitar operar en periodos desfavorables.

- Considerar la inclusión de un filtro de volatilidad para reducir la frecuencia de trading en momentos de excesiva volatilidad.

Conclusión

Se trata de un sistema de seguimiento de tendencia con una estructura completa y una lógica clara. Mediante la combinación del trailing stop dinámico basado en ATR y el filtro de tendencia con EMA, controla bien el riesgo mientras captura las tendencias. El diseño del mecanismo de obtención de beneficios por tramos refleja una mentalidad de trading madura. La estrategia tiene una gran practicidad y escalabilidad, y mediante una optimización y mejora continuas, puede lograr mejores resultados de trading.

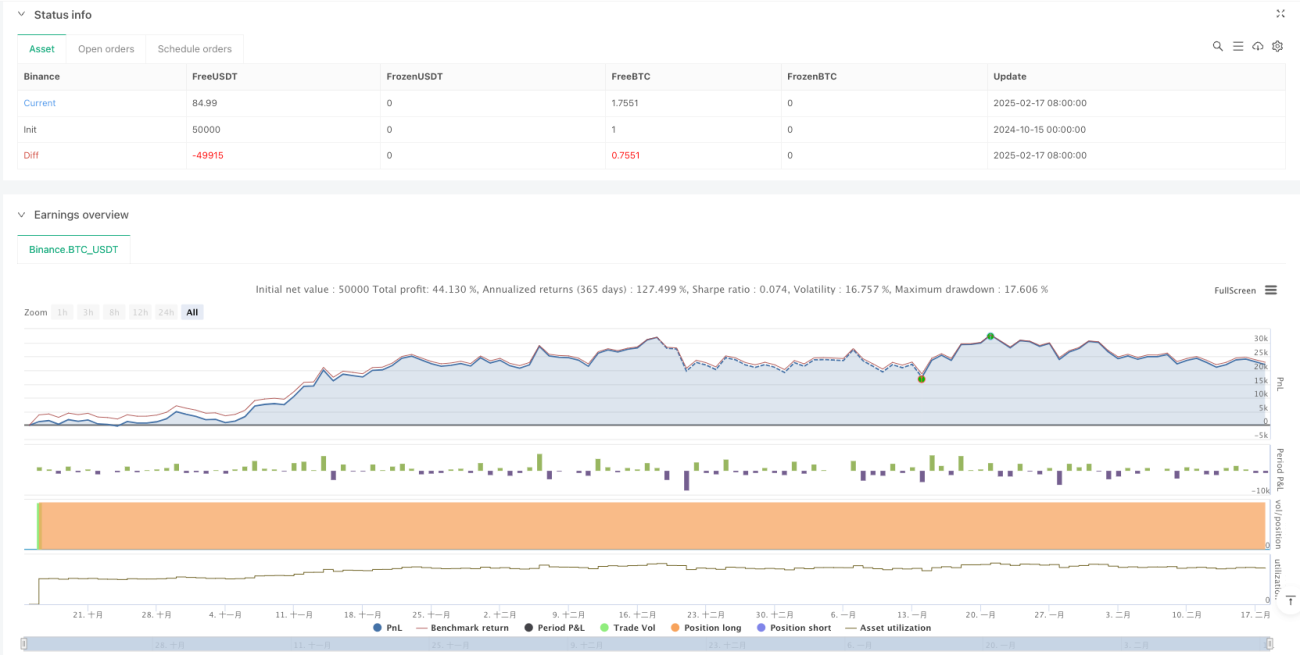

/*backtest

start: 2024-10-15 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Enhanced UT Bot with Long & Short Trades", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input Parameters- 1