Resumen

Esta estrategia es un sistema de trading integral que combina múltiples indicadores, como la media móvil exponencial (EMA), el índice de fuerza relativa (RSI) y el rango verdadero medio (ATR), además de incorporar el índice direccional medio (ADX) para mejorar la precisión en la identificación de tendencias. El sistema utiliza múltiples señales de confirmación para determinar los momentos de entrada, y gestiona dinámicamente el stop loss y el take profit mediante el ATR, logrando un control eficaz del riesgo.

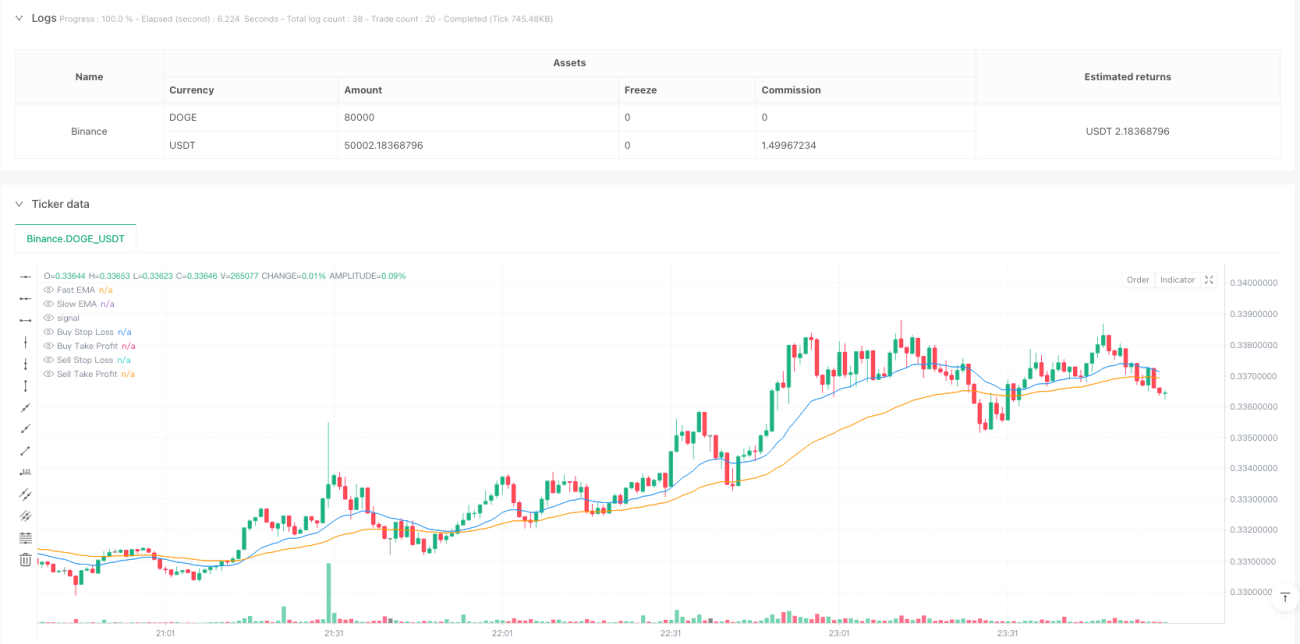

Principio de la estrategia

El núcleo de la estrategia consiste en capturar tendencias del mercado y realizar operaciones mediante la combinación de múltiples indicadores técnicos. Incluye:

- Uso de EMAs rápidas (20 períodos) y lentas (50 períodos) para determinar la dirección de la tendencia.

- Combinación con ADX (14 períodos) para confirmar la fuerza de la tendencia, requiriendo ADX > 20 para validar la tendencia.

- Empleo del RSI (14 períodos) para buscar oportunidades de sobrecompra/sobreventa: una ruptura de RSI por encima de 30 activa una compra, y una caída por debajo de 70 activa una venta.

- Cálculo de niveles dinámicos de stop loss y take profit usando ATR (14 períodos), con una relación riesgo-beneficio de 2:1.

Ventajas de la estrategia

- La confirmación de múltiples señales mejora la precisión de las operaciones y evita señales falsas.

- La inclusión del ADX aumenta la fiabilidad en la identificación de tendencias.

- El mecanismo dinámico de stop loss y take profit se adapta a los cambios en la volatilidad del mercado.

- Un estricto control de riesgo garantiza que cada operación tenga un riesgo manejable.

- La lógica de la estrategia es clara y sus parámetros son altamente ajustables.

Riesgos de la estrategia

- La multiplicidad de indicadores puede provocar un retraso en las señales, afectando los puntos de entrada.

- En mercados laterales podría generar operaciones frecuentes.

- El ADX puede producir señales tardías en ciertas condiciones del mercado.

- Los parámetros deben optimizarse según diferentes entornos de mercado.

Direcciones de optimización

- Considerar agregar indicadores de volumen para reforzar la fiabilidad de las señales.

- Introducir un filtro de volatilidad del mercado para ajustar el tamaño de las posiciones durante períodos de alta volatilidad.

- Desarrollar un mecanismo de parámetros adaptativos que se ajuste dinámicamente según las condiciones del mercado.

- Añadir una clasificación de la fuerza de la tendencia para gestionar dinámicamente el tamaño de las posiciones.

- Optimizar la lógica de stop loss y take profit incorporando un trailing stop.

Conclusión

Esta estrategia construye un sistema de trading de seguimiento de tendencias completo mediante la combinación orgánica de múltiples indicadores técnicos. Garantiza la precisión de las operaciones al mismo tiempo que asegura la seguridad mediante un estricto control de riesgo. Aunque existe cierto margen de optimización, el marco general tiene un buen valor práctico y escalabilidad.

/*backtest

start: 2025-01-20 00:00:00

end: 2025-01-31 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"DOGE_USDT"}]

*/

//@version=5

strategy("Enhanced GBP/USD Strategy with ADX", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=1)

// === Input Parameters ===- 1