Resumen

Esta es una estrategia de trading basada en múltiples bandas estadísticas y análisis de tendencias. Combina el uso de Bandas de Bollinger, bandas de cuantiles y bandas de ley de potencia para identificar áreas clave de soporte/resistencia, y utiliza la línea de desviación estándar inferior de la banda de cuantil superior como señal de activación para determinar los momentos de entrada y salida. El diseño de la estrategia considera plenamente la volatilidad del mercado, mejorando la fiabilidad de las señales mediante la superposición de múltiples métodos estadísticos.

Principio de la Estrategia

El principio central de la estrategia es capturar las tendencias del mercado mediante el cruce de múltiples bandas estadísticas. Incluye principalmente los siguientes componentes clave:

- Sistema de Bandas de Bollinger: se utiliza para determinar el rango de fluctuación de precios; cuando el precio supera la banda superior, cambia a una advertencia amarilla.

- Sistema de bandas de cuantiles: calcula los cuantiles superior e inferior del precio para evaluar la probabilidad de valores extremos del precio.

- Sistema de bandas de ley de potencia: calcula el nivel de significancia basado en rendimientos históricos para medir sobrecompra/sobreventa.

- Sistema de activación: utiliza la línea de desviación estándar inferior de la banda de cuantil superior como señal de activación principal; mantener el precio por encima de esta línea se considera una señal alcista.

- Sistema de confirmación: filtra señales falsas mediante el establecimiento de un número de velas consecutivas de confirmación.

Ventajas de la Estrategia

- Alta estabilidad de señales: la superposición de múltiples bandas estadísticas reduce eficazmente las señales falsas.

- Buena adaptabilidad: la estrategia puede adaptarse a diferentes marcos temporales y condiciones del mercado.

- Control de riesgos sólido: divide las zonas de riesgo mediante múltiples bandas estadísticas, y cuenta con un mecanismo de stop loss.

- Parámetros flexibles: ofrece una amplia gama de opciones de parámetros que pueden optimizarse según las características del mercado.

- Visualización clara: los colores de las líneas de los diferentes indicadores se distinguen claramente, las señales de trading son intuitivas.

Riesgos de la Estrategia

- Riesgo de rezago: los indicadores estadísticos tienen cierto retraso, lo que puede hacer que se pierdan los mejores puntos de entrada.

- Desventaja en mercados laterales: en mercados oscilantes puede generar demasiadas señales de trading.

- Sensibilidad a los parámetros: el efecto de diferentes combinaciones de parámetros varía considerablemente, requiriendo optimización repetida.

- Alta carga computacional: el cálculo en tiempo real de múltiples indicadores estadísticos requiere importantes recursos computacionales.

- Dependencia del entorno del mercado: en condiciones extremas del mercado, las regularidades estadísticas pueden fallar.

Direcciones de Optimización de la Estrategia

- Introducir parámetros dinámicos: ajustar automáticamente los parámetros según la volatilidad del mercado.

- Agregar juicio del entorno del mercado: añadir indicadores de fuerza de tendencia para filtrar señales en mercados laterales.

- Optimizar la eficiencia computacional: simplificar algunos procesos de cálculo para reducir el uso de recursos.

- Mejorar el control de riesgos: agregar más condiciones de stop loss y estrategias de gestión de posiciones.

- Aumentar la adaptabilidad: desarrollar un sistema de optimización de parámetros adaptativo.

Conclusión

Esta es una estrategia integral de seguimiento de tendencias que combina múltiples métodos estadísticos. Mediante la sinergia de las Bandas de Bollinger, las bandas de cuantiles y las bandas de ley de potencia, puede captar bien las tendencias del mercado, al mismo tiempo que cuenta con una buena capacidad de control de riesgos. Aunque existen ciertos problemas de rezago y dificultades en la optimización de parámetros, a través de la mejora continua y la optimización, esta estrategia tiene un buen valor práctico y perspectivas de desarrollo.

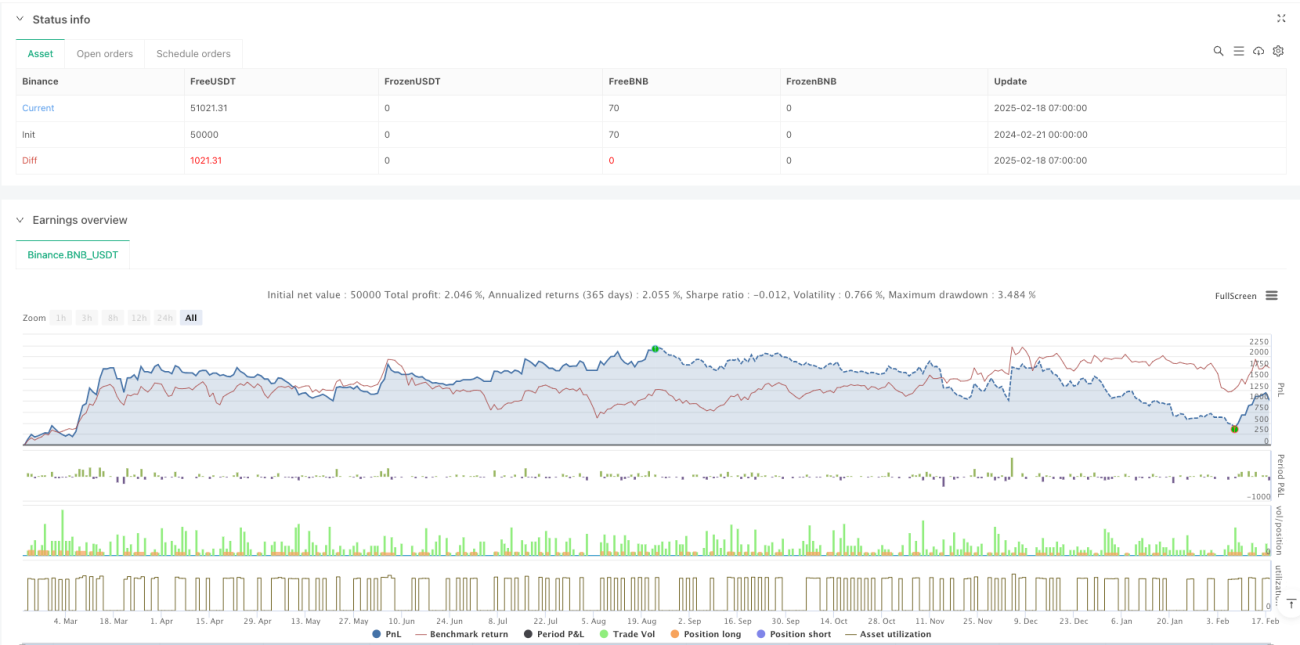

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BNB_USDT"}]

*/

//@version=6

strategy("Multi-Band Comparison Strategy with Separate Entry/Exit Confirmation", overlay=true,

default_qty_type=strategy.percent_of_equity, default_qty_value=10,

initial_capital=5000, currency=currency.USD)- 1