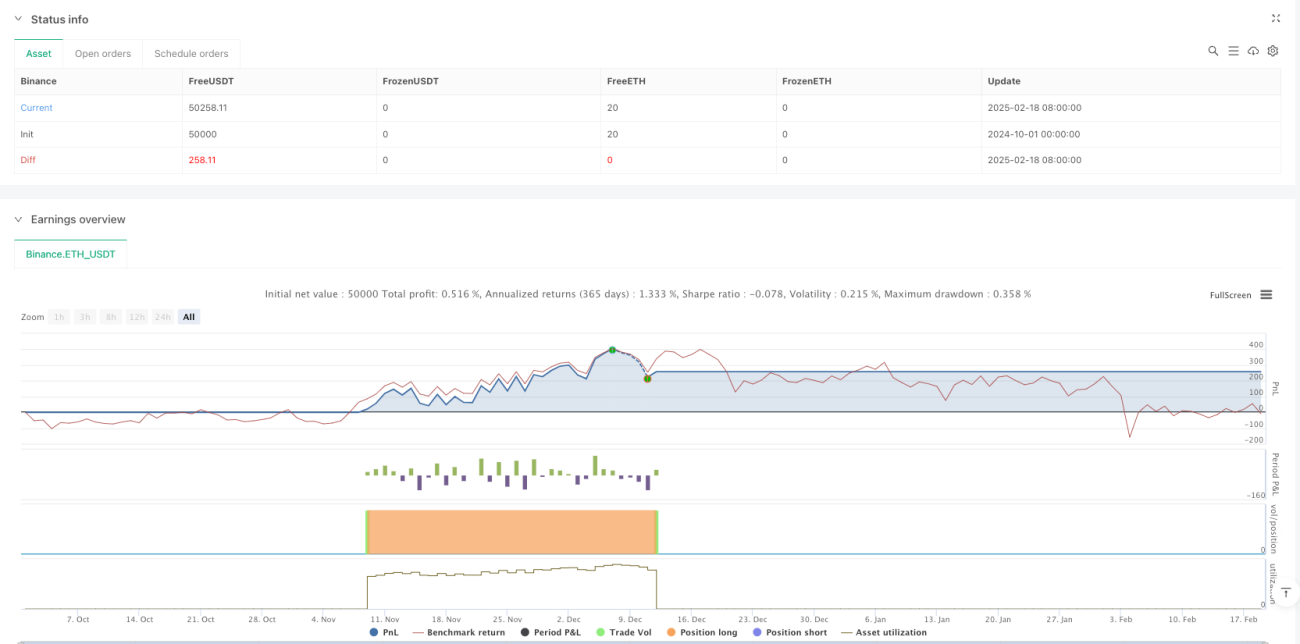

Resumen

Esta estrategia es un sistema de trading de seguimiento de tendencia basado en la ruptura del Canal de Donchian, que combina el indicador SuperTrend y un filtro de volumen para mejorar la fiabilidad de las señales de trading. La estrategia identifica principalmente oportunidades de trading en largo capturando rupturas de precios por encima de máximos históricos, al mismo tiempo que utiliza la confirmación de volumen y un indicador de seguimiento de tendencia para filtrar señales falsas. El diseño de la estrategia es flexible y permite optimizar los parámetros según diferentes entornos de mercado y activos.

Principio de la Estrategia

La lógica central de la estrategia se basa en los siguientes componentes clave:

- Canal de Donchian: Calcula el precio máximo y mínimo dentro de un período definido por el usuario, formando bandas superior, inferior y media. Cuando el precio supera la banda superior, se genera una señal de entrada en largo.

- Filtro de volumen: Compara el volumen actual con la media móvil de 20 períodos para asegurar que la entrada ocurre solo cuando el volumen aumenta, mejorando así la fiabilidad de la ruptura.

- SuperTrend: Actúa como herramienta de confirmación de tendencia, mostrándose verde en tendencia alcista y rojo en tendencia bajista.

- Stop loss flexible: Ofrece cuatro opciones diferentes de stop loss, incluyendo stop loss por banda inferior, banda media, SuperTrend y stop loss porcentual basado en seguimiento.

Ventajas de la Estrategia

- Confirmación múltiple de señales: Combinando ruptura de precio, confirmación de volumen e indicadores de tendencia, se reduce significativamente el riesgo de rupturas falsas.

- Alta adaptabilidad: Los parámetros pueden ajustarse para adaptarse a diferentes entornos de mercado y marcos temporales.

- Gestión de riesgos completa: Ofrece múltiples opciones de stop loss que permiten elegir el método más adecuado según las características del mercado.

- Visualización clara: La interfaz de la estrategia muestra de forma intuitiva los indicadores, facilitando la comprensión del estado del mercado.

- Backtesting flexible: Permite definir rangos de tiempo personalizados para el backtesting, facilitando la optimización.

Riesgos de la Estrategia

- Riesgo en mercados laterales: Pueden generarse señales de ruptura falsas frecuentes en condiciones de mercado sin tendencia definida.

- Riesgo de deslizamiento: En mercados con baja liquidez, las señales de ruptura pueden sufrir desviaciones en el precio de entrada debido al deslizamiento.

- Riesgo de sobrefiltrado: La activación del filtro de volumen puede hacer que se pierdan algunas oportunidades de trading válidas.

- Sensibilidad a parámetros: El rendimiento de la estrategia es sensible a la configuración de parámetros, requiriendo una optimización cuidadosa.

Direcciones de Optimización de la Estrategia

- Agregar filtro de fuerza de tendencia: Se puede incorporar un indicador de fuerza de tendencia como ADX para entrar solo cuando la tendencia sea fuerte.

- Optimizar el indicador de volumen: Podría considerarse usar un indicador de volumen relativo o de ruptura de volumen en lugar de una simple media móvil.

- Añadir filtro temporal: Incluir una ventana de horario de trading para evitar periodos de alta volatilidad.

- Optimización dinámica de parámetros: Ajustar automáticamente los períodos del canal y los parámetros del SuperTrend según la volatilidad del mercado.

- Introducir aprendizaje automático: Utilizar algoritmos de machine learning para optimizar la selección de parámetros y el filtrado de señales.

Resumen

Esta estrategia construye un sistema de trading de seguimiento de tendencia relativamente completo mediante el uso combinado de múltiples indicadores técnicos. Su ventaja radica en la alta fiabilidad de las señales y la flexibilidad en la gestión de riesgos, aunque requiere que el trader optimice los parámetros según las características específicas del mercado. Con mejoras y optimizaciones continuas, esta estrategia tiene el potencial de obtener resultados de trading estables en mercados con tendencia definida.

- 1