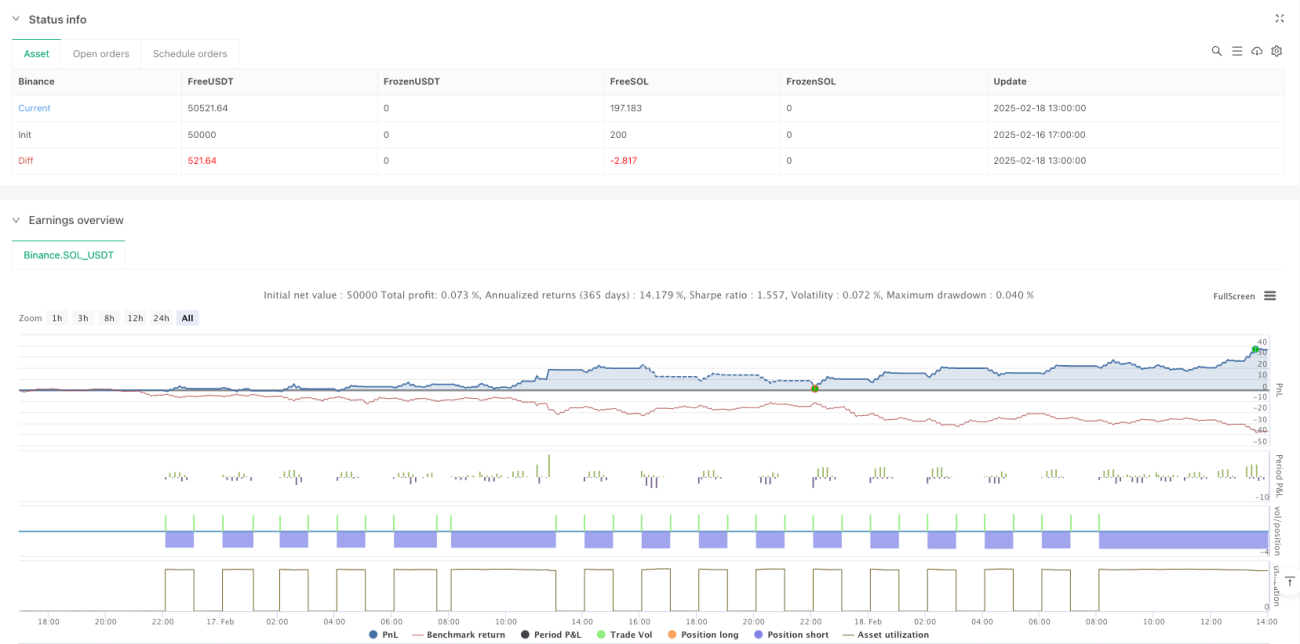

Resumen

Esta estrategia es una estrategia de trading intradía que combina la ruptura del rango de precio del día anterior y las medias móviles exponenciales (EMAs). La estrategia identifica los momentos en que el precio supera el máximo o mínimo del día de negociación anterior, combinándolos con señales de confirmación de EMAs rápidas y lentas para operar. Se centra en capturar el impulso del precio a corto plazo, gestionando el riesgo mediante un stop loss fijo y una relación riesgo-beneficio.

Principio de la estrategia

El núcleo de la estrategia se basa en los siguientes elementos clave:

- Usar la función

request.securitypara obtener el máximo y mínimo del día de negociación anterior como rango de precio clave. - Calcular las EMAs de 9 y 21 períodos como indicadores de confirmación de tendencia.

- Cuando el precio supera el máximo del día anterior y la EMA rápida está por encima de la EMA lenta, se genera una señal larga.

- Cuando el precio supera el mínimo del día anterior y la EMA rápida está por debajo de la EMA lenta, se genera una señal corta.

- Gestionar el riesgo de cada operación estableciendo un stop loss fijo (30 puntos) y una relación riesgo-beneficio (2.0).

- Filtro opcional de horario de negociación, que permite operar en un período específico (zona horaria SAST).

Ventajas de la estrategia

- Estructura clara y lógica simple: la estrategia utiliza una lógica de ruptura de precio fácil de entender y ejecutar.

- Gestión de riesgos completa: mediante la configuración de un stop loss fijo y una relación riesgo-beneficio, se logra un control de riesgos estricto.

- Gestión de tiempo flexible: el filtro opcional de horario de negociación permite operar en los períodos de mayor actividad del mercado.

- Mecanismo de confirmación múltiple: la combinación de ruptura de precio y confirmación de EMAs reduce el riesgo de señales falsas.

- Alto nivel de automatización: la estrategia se puede ejecutar completamente de forma automatizada, reduciendo la intervención humana.

Riesgos de la estrategia

- Riesgo de ruptura falsa: el precio puede retroceder rápidamente después de la ruptura, lo que provoca una salida por stop loss.

- Riesgo de deslizamiento: en períodos de alta volatilidad, el precio de ejecución real puede desviarse significativamente del precio de la señal.

- Riesgo de stop loss fijo: un stop loss basado en un número fijo de puntos puede no adaptarse a todas las condiciones del mercado.

- Riesgo de volatilidad del mercado: en períodos de baja volatilidad, se pueden generar demasiadas señales de negociación.

Direcciones de optimización de la estrategia

- Optimización del stop loss dinámico: se puede considerar ajustar el número de puntos del stop loss según la volatilidad del mercado.

- Optimización del horario de negociación: mediante el análisis de datos históricos, optimizar la configuración de la ventana de tiempo de negociación.

- Mejora del filtro de señales: agregar indicadores de volumen o volatilidad como condiciones de filtro adicionales.

- Optimización de parámetros de EMAs: determinar la configuración óptima del período de EMAs mediante backtesting.

- Optimización de la gestión de posiciones: introducir un mecanismo de gestión de posiciones dinámico basado en la volatilidad.

Resumen

Esta estrategia logra un sistema de trading intradía confiable al combinar la ruptura de precio y la confirmación de tendencia mediante EMAs. Su principal ventaja radica en su estructura lógica clara y su completo mecanismo de gestión de riesgos. A través de las direcciones de optimización sugeridas, la estrategia puede mejorar aún más su estabilidad y rentabilidad. En la operación real, se debe prestar especial atención a los riesgos de ruptura falsa y deslizamiento, y ajustar los parámetros según las condiciones reales del mercado.

/*backtest

start: 2025-02-16 17:00:00

end: 2025-02-18 14:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("GER40 Momentum Breakout Scalping", overlay=true, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=1)

//———— Input Parameters —————- 1