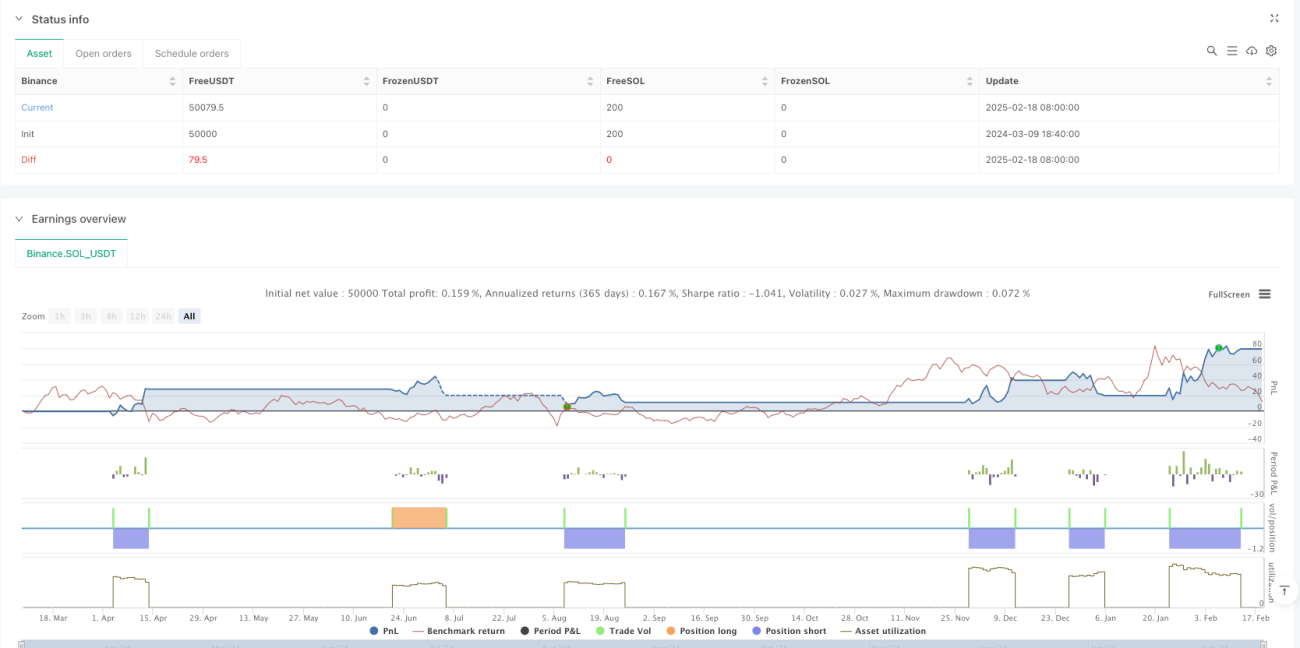

Resumen

Esta estrategia analiza el sentimiento del mercado basándose en patrones de velas japonesas, cuantificando la psicología del mercado a través de tres osciladores centrales: el oscilador de indecisión, el oscilador de miedo y el oscilador de codicia. La estrategia integra indicadores de momentum y tendencia, combinados con confirmación de volumen, para construir un sistema de trading completo. Está diseñada para traders que buscan identificar oportunidades de alta probabilidad mediante el análisis del sentimiento del mercado.

Principio de la estrategia

El núcleo de la estrategia consiste en construir tres osciladores de sentimiento analizando diferentes patrones de velas:

- Oscilador de indecisión – mide la incertidumbre del mercado a través de patrones Doji y Spinning Top.

- Oscilador de miedo – rastrea el sentimiento bajista mediante patrones como Estrella Fugaz, Hombre Colgado y Engulfing Bajista.

- Oscilador de codicia – detecta el sentimiento alcista a través de velas sin sombra superior, Martillo, Engulfing Alcista y Tres Soldados Blancos.

El promedio de estos tres osciladores constituye el Índice de Emoción de Velas (CEI, por sus siglas en inglés). Cuando el CEI supera diferentes umbrales, se generan señales de compra o venta, confirmadas por el volumen.

Ventajas de la estrategia

- Análisis de sentimiento sistematizado – convierte el análisis subjetivo de patrones de velas en indicadores objetivos.

- Gestión de riesgos completa – incluye mecanismos como período máximo de retención, stop-loss y take-profit, así como períodos de enfriamiento.

- Mecanismo de recuperación flexible – cuando una operación entra en pérdidas, la estrategia intenta recuperarse mediante la ruptura del punto de equilibrio.

- Aplicabilidad multi-mercado – puede aplicarse a acciones, divisas, criptomonedas y otros mercados.

- Alta fiabilidad de las señales – la confirmación por volumen y la validación de múltiples indicadores técnicos mejoran la precisión.

Riesgos de la estrategia

- Sensibilidad a parámetros – los diferentes umbrales requieren pruebas y optimización exhaustivas.

- Dependencia del entorno de mercado – puede generar señales falsas en mercados laterales o de rango.

- Riesgo de deslizamiento – en mercados con baja liquidez, puede enfrentar riesgos de ejecución.

- Riesgo de sobreoperación – es necesario establecer períodos de enfriamiento razonables para evitar operaciones frecuentes.

- Riesgo sistémico – puede sufrir pérdidas significativas durante eventos importantes del mercado.

Direcciones de optimización de la estrategia

- Umbrales dinámicos – ajustar automáticamente los umbrales según la volatilidad del mercado.

- Clasificación del estado del mercado – añadir mecanismos para identificar mercados en tendencia o laterales.

- Optimización mediante machine learning – utilizar algoritmos de aprendizaje automático para optimizar combinaciones de parámetros.

- Mejora de la gestión de riesgos – incorporar módulos de gestión de capital y control de posiciones.

- Filtrado de señales – integrar más indicadores técnicos para filtrar señales falsas.

Conclusión

Se trata de una estrategia innovadora que combina el análisis técnico con el trading cuantitativo. Mediante un análisis de sentimiento sistematizado y una estricta gestión de riesgos, esta estrategia puede proporcionar señales de trading fiables a los traders. Aunque tiene cierto margen de optimización, su marco básico es sólido y adecuado para un mayor desarrollo y aplicación en entornos reales.

- 1