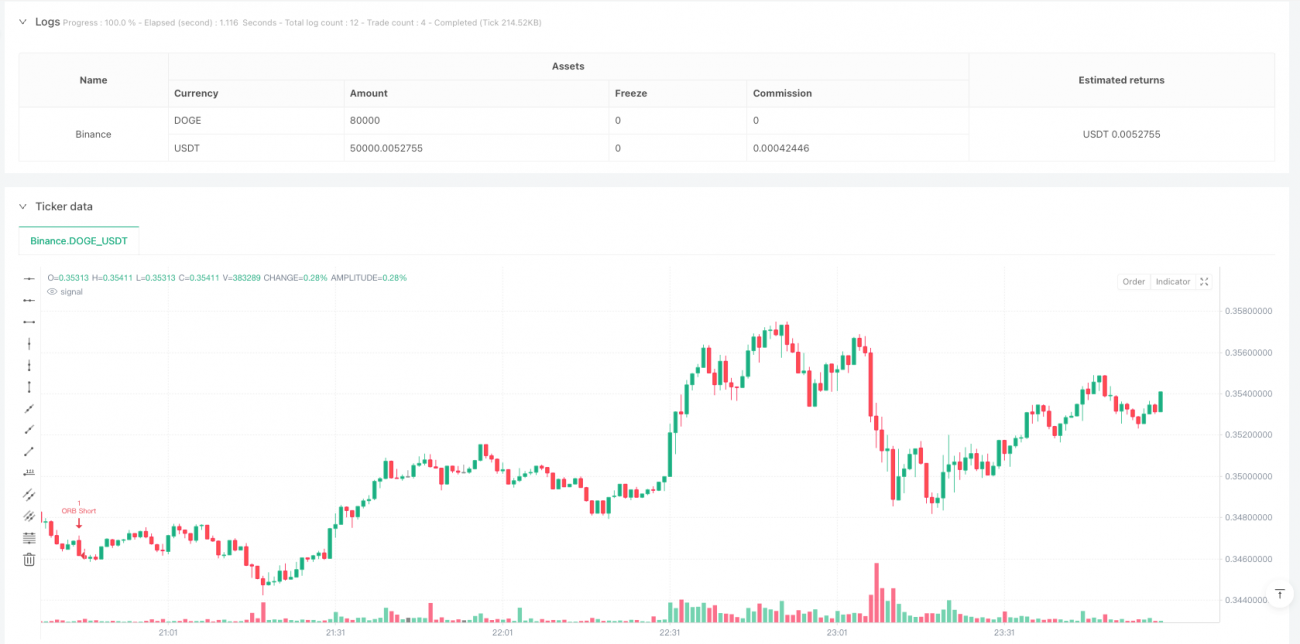

Resumen

Esta estrategia es un sistema de trading de alta frecuencia basado en la ruptura del rango de apertura, centrado en el rango de precios formado durante el periodo de 9:30 a 9:45 en la mañana de la sesión de negociación. La estrategia toma decisiones de trading observando si el precio rompe este rango de 15 minutos, combinando al mismo tiempo configuraciones dinámicas de stop-loss y take-profit para lograr una relación óptima entre riesgo y rendimiento. El sistema también incluye una función de selección de días de negociación, que permite operar selectivamente según las características del mercado en diferentes períodos.

Principio de la estrategia

La lógica central de la estrategia es establecer un rango de precios durante los primeros 15 minutos posteriores a la apertura de cada día de negociación (9:30-9:45 EST), registrando el precio más alto y el más bajo durante este período. Una vez formado el rango, la estrategia monitorea las rupturas de precio antes de las 12:00 del mismo día:

- Cuando el precio supera el límite superior del rango, se abre una posición larga, con un stop-loss de 0.5 veces el tamaño del rango y un take-profit de 3 veces el stop-loss.

- Cuando el precio rompe el límite inferior del rango, se abre una posición corta, con la misma configuración de stop-loss y take-profit.

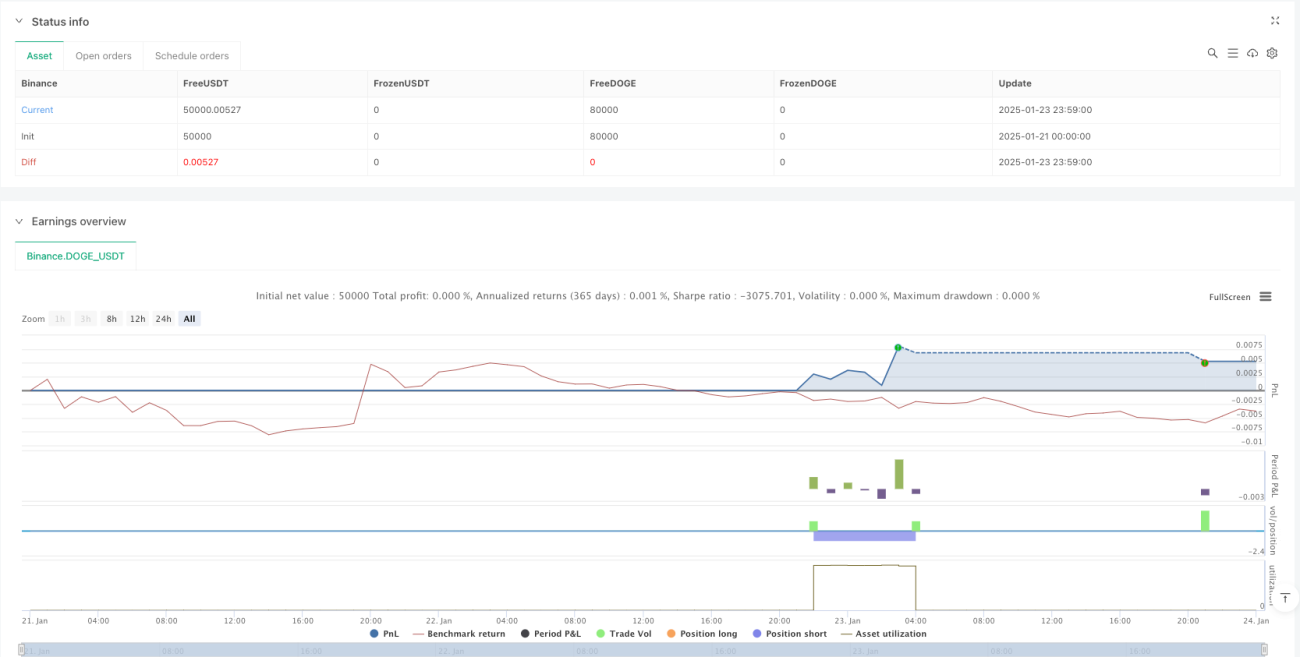

La estrategia también incluye un mecanismo para evitar operaciones repetidas, asegurando que solo se ejecute una operación por día, y cierra todas las posiciones al final de la sesión.

Ventajas de la estrategia

- Eficiencia temporal: La estrategia se centra en el período más activo después de la apertura, capturando oportunidades de grandes movimientos en la mañana.

- Control de riesgos: Utiliza configuraciones dinámicas de stop-loss y take-profit, determinando los parámetros de gestión de riesgos según la volatilidad real.

- Flexibilidad de trading: Ofrece la opción de seleccionar días de negociación por semana, evitando días desfavorables en entornos de mercado específicos.

- Ejecución clara: Las señales de trading son claras, las condiciones de entrada y salida están bien definidas, sin verse afectadas por juicios subjetivos.

- Alto nivel de automatización: Ejecución completamente automatizada, reduciendo la influencia emocional de la intervención humana.

Riesgos de la estrategia

- Riesgo de ruptura falsa: La primera ruptura después de la formación del rango de apertura podría ser una ruptura falsa, lo que lleva a una salida por stop-loss.

- Decaimiento temporal: La estrategia solo opera durante la mañana, perdiendo potencialmente buenas oportunidades en otros horarios.

- Dependencia de la volatilidad: En días de baja volatilidad del mercado, la estrategia podría tener dificultades para obtener suficiente espacio de ganancias.

- Impacto del deslizamiento: Como estrategia de alta frecuencia, puede enfrentar pérdidas significativas por deslizamiento durante la ejecución.

- Dependencia del entorno de mercado: El rendimiento de la estrategia puede verse afectado significativamente por las condiciones generales del mercado.

Direcciones de optimización de la estrategia

- Incorporar indicadores de volumen: Se puede filtrar señales de ruptura falsa observando el volumen en el momento de la ruptura.

- Ajustar dinámicamente el horario de trading: Optimizar la ventana de tiempo de trading según las características del período activo de diferentes instrumentos.

- Agregar filtro de tendencia: Combinar el juicio de tendencia de marcos temporales más grandes para mejorar la precisión de la dirección de trading.

- Optimizar la configuración de stop-loss: Se puede considerar el uso de indicadores dinámicos de ATR para establecer la distancia del stop-loss.

- Incluir filtro de volatilidad: Evaluar el nivel de volatilidad antes de la apertura para decidir si ejecutar la operación del día.

Resumen

Esta es una estrategia de ruptura de rango de apertura bien diseñada y lógicamente rigurosa, que captura oportunidades de trading al enfocarse en el período más activo del mercado. Sus ventajas radican en una lógica de trading clara y un mecanismo completo de control de riesgos, pero también se deben considerar riesgos potenciales como rupturas falsas y dependencia del entorno de mercado. Mediante una optimización y mejora continuas, esta estrategia tiene el potencial de obtener ganancias estables en el trading real.

/*backtest

start: 2025-01-21 00:00:00

end: 2025-01-24 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"DOGE_USDT"}]

args: [["MaxCacheLen",580,358374]]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © UKFLIPS69

- 1