Estrategia de ruptura de tendencia con fusión de indicadores técnicos multidimensionales

Resumen

Esta estrategia es un sistema de trading de ruptura de tendencia que combina múltiples indicadores técnicos y patrones gráficos. Identifica puntos de inflexión en el mercado mediante el reconocimiento de formaciones clave (como doble techo/doble suelo, cabeza y hombros) y rupturas de precios, mientras utiliza indicadores como EMA, ATR y volumen para filtrar señales y gestionar el riesgo, logrando un seguimiento eficiente de la tendencia y un control de riesgos.

Principio de la estrategia

La lógica central de la estrategia consta de tres partes principales:

- Reconocimiento de patrones gráficos: utiliza un método de ventana deslizante para identificar formaciones clásicas como doble techo/doble suelo, cabeza y hombros, confirmando señales de reversión mediante la comparación de máximos/mínimos y el cruce de EMAs.

- Sistema de confirmación de tendencia: emplea la EMA de 50 periodos como filtro de tendencia, junto con la ruptura de precios para confirmar la dirección, y un filtro de volumen (que exige un volumen superior al 120% del promedio de 20 días) para verificar la validez de la señal.

- Sistema de gestión de riesgos: establece stops dinámicos de ganancias y pérdidas basados en el ATR de 14 periodos, utilizando un multiplicador de 1,5 veces el ATR para controlar con precisión la relación riesgo-recompensa.

Ventajas de la estrategia

- Fusión de señales multidimensionales: combina información de patrones gráficos, medias móviles, volatilidad y volumen para mejorar la fiabilidad de las señales.

- Gestión dinámica del riesgo: ajusta los niveles de stop-loss y take-profit de forma dinámica con el ATR, adaptándose a diferentes condiciones de mercado.

- Alto grado de automatización: el sistema identifica automáticamente patrones, genera señales y ejecuta órdenes, reduciendo la intervención manual.

- Indicaciones visuales claras: mediante marcas gráficas y un sistema de alertas, las señales de trading se muestran de forma intuitiva.

Riesgos de la estrategia

- Riesgo de falsa ruptura: en mercados laterales pueden aparecer señales falsas de ruptura, que requieren una estricta confirmación mediante volumen.

- Riesgo de rezago: indicadores como la EMA y el ATR tienen cierto retraso, lo que podría hacer que se pierdan los mejores puntos de entrada.

- Sensibilidad a los parámetros: el rendimiento de la estrategia depende en gran medida de la configuración de parámetros, siendo necesario optimizarlos mediante backtesting.

- Dependencia del entorno de mercado: en mercados sin tendencia clara o en rango, el desempeño de la estrategia puede no ser óptimo.

Direcciones de optimización de la estrategia

- Introducir identificación del entorno de mercado: agregar indicadores de fuerza de tendencia (como ADX) para distinguir entre mercados con tendencia y laterales, ajustando los parámetros de forma dinámica.

- Optimizar el filtrado de señales: considerar la inclusión de osciladores como el RSI para filtrar aún más las señales falsas de ruptura.

- Mejorar el control de riesgos: implementar un sistema de gestión de posición que ajuste el tamaño de las operaciones según la volatilidad del mercado.

- Aumentar la adaptabilidad: desarrollar un sistema de parámetros adaptativos que optimice automáticamente la configuración según las condiciones del mercado.

Resumen

Esta estrategia logra capturar eficazmente los puntos de inflexión de la tendencia del mercado mediante la integración de múltiples indicadores técnicos. El diseño del sistema considera de manera integral elementos clave como la generación de señales, la confirmación de tendencia y el control de riesgos, lo que le otorga una gran utilidad práctica. Siguiendo las direcciones de optimización sugeridas, se espera mejorar aún más su estabilidad y adaptabilidad. En la aplicación en tiempo real, se recomienda a los operadores ajustar los parámetros de la estrategia según las características específicas del mercado y su tolerancia al riesgo personal.

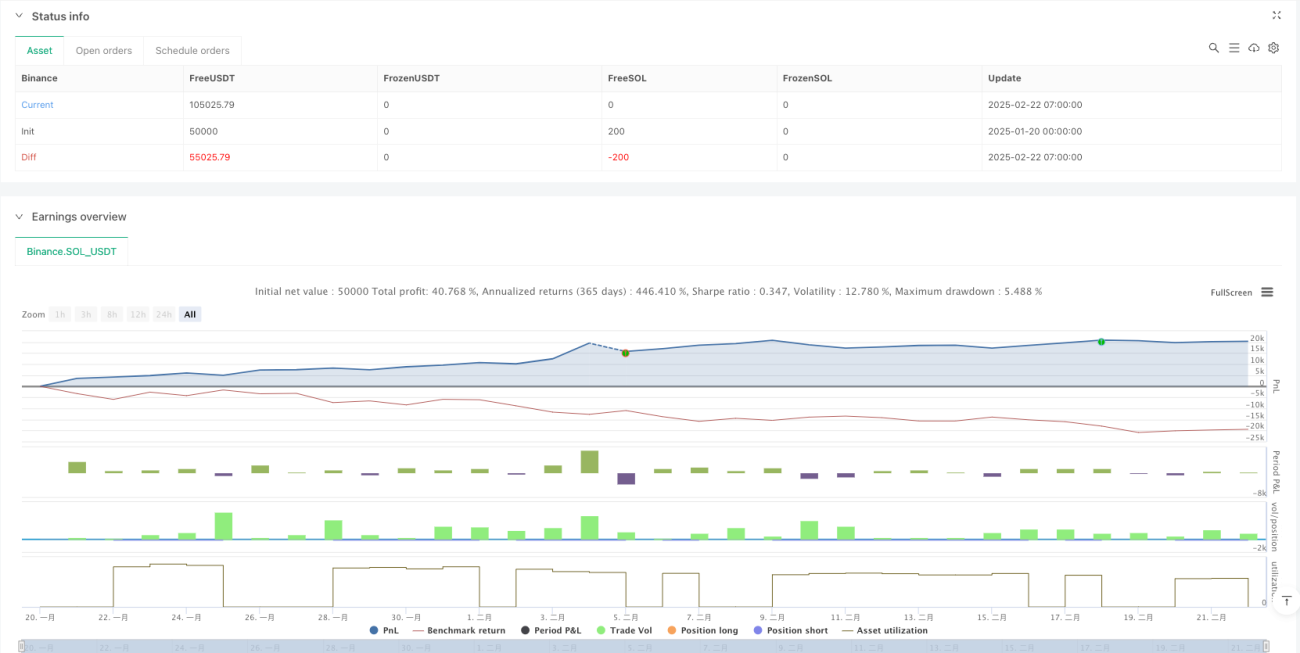

/*backtest

start: 2025-01-20 00:00:00

end: 2025-02-22 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Ultimate Pattern Finder", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// 🎯 CONFIGURABLE PARAMETERS- 1