Resumen

La estrategia de trading inteligente con múltiples indicadores ponderados es un sistema de trading cuantitativo integral que genera decisiones de trading mediante la integración de señales de múltiples indicadores técnicos, asignándoles diferentes pesos. Esta estrategia combina diversas herramientas de análisis técnico como MACD, RSI estocástico, EMA, Súper Tendencia y cruce de medias móviles, formando un marco de trading completo. El sistema no solo admite mecanismos de take profit multinivel y stop loss dinámico, sino que también ajusta automáticamente los parámetros de trading según las condiciones del mercado, manteniendo una alta adaptabilidad en diferentes entornos de mercado. Esta estrategia es especialmente adecuada para traders de medio y largo plazo, ya que el sistema de asignación de pesos hace que las decisiones de trading sean más sólidas y fiables.

Principio de la estrategia

El núcleo de la estrategia reside en su sistema de señales ponderadas, que genera señales de trading a través de cinco subestrategias diferentes:

-

Estrategia MACD: Utiliza el cruce de la línea MACD con la línea de señal para determinar la dirección de la tendencia del mercado. Cuando la línea MACD cruza por encima de la línea de señal, genera una señal de compra; cuando cruza por debajo, genera una señal de venta.

-

Estrategia RSI estocástico: Combina las ventajas del RSI y los indicadores estocásticos para monitorear las condiciones de sobrecompra y sobreventa del mercado. Cuando el RSI estocástico está por debajo del umbral de sobreventa establecido, genera una señal de compra; cuando está por encima del umbral de sobrecompra, genera una señal de venta.

-

Estrategia EMA de sobrecompra/sobreventa: Utiliza la EMA para identificar el grado de desviación del precio respecto a su media. Cuando el RSI está por debajo del umbral de sobreventa establecido, genera una señal de compra; cuando está por encima del umbral de sobrecompra, genera una señal de venta.

-

Estrategia de Súper Tendencia: Establece un canal de precios basado en múltiplos del ATR y determina la dirección del trading mediante cambios en la tendencia. Cuando el indicador de Súper Tendencia pasa de negativo a positivo, genera una señal de compra; cuando pasa de positivo a negativo, genera una señal de venta.

-

Estrategia de cruce de medias móviles: Utiliza el cruce de dos medias móviles de diferentes períodos para determinar la tendencia del mercado. Cuando la media móvil de corto plazo cruza por encima de la de largo plazo, genera una señal de compra; cuando cruza por debajo, genera una señal de venta.

La estrategia calcula ponderadamente las señales de cada subestrategia mediante un sistema de pesos personalizable, y solo activa una operación cuando la suma ponderada supera el umbral establecido. Además, la estrategia incluye un mecanismo de identificación de posibles techos y suelos, que permite ajustar las posiciones cuando el mercado podría estar a punto de revertirse.

Este mecanismo de confirmación de señales en múltiples niveles reduce eficazmente las señales falsas, mejora la fiabilidad del sistema de trading, y la flexibilidad en la configuración de parámetros permite que la estrategia se adapte a diferentes instrumentos y marcos temporales.

Ventajas de la estrategia

-

Confirmación múltiple de señales: Las señales generadas por cinco indicadores técnicos independientes se ponderan, lo que reduce la posibilidad de engaño de un solo indicador y mejora la calidad y fiabilidad de las señales de trading.

-

Sistema de pesos adaptativo: Cada subestrategia puede tener un peso diferente, lo que permite al trader ajustar el enfoque de la estrategia según su confianza en cada indicador y su rendimiento histórico, aumentando la flexibilidad.

-

Gestión de riesgos completa: La estrategia incorpora mecanismos de control de riesgos en múltiples niveles, incluyendo stop loss, take profit multinivel y ajuste dinámico del stop loss, asegurando un control rápido del riesgo en movimientos adversos del mercado.

-

Identificación automatizada de posibles techos y suelos: Mediante un análisis integral de RSI, volumen y evolución de precios, la estrategia puede identificar posibles techos y suelos del mercado, y cerrar parcialmente las posiciones en momentos oportunos para asegurar ganancias o reducir pérdidas.

-

Alta personalización: Prácticamente todos los parámetros son ajustables, incluyendo los períodos de cálculo de cada indicador, los valores de los pesos, los porcentajes de take profit/stop loss, etc., lo que permite al trader optimizar la estrategia según su estilo personal y diferentes condiciones del mercado.

-

Mecanismo de retardo incorporado: Para evitar entrar en operaciones demasiado pronto o basándose en ruido, la estrategia utiliza un mecanismo de confirmación retardada, asegurando que solo las señales persistentes activen las operaciones, reduciendo el impacto de las fluctuaciones a corto plazo.

-

Filtro temporal: La estrategia permite establecer fechas de inicio y fin para las operaciones, lo que permite al trader realizar backtesting en períodos específicos o evitar épocas de anomalías conocidas en el mercado.

Riesgos de la estrategia

-

Riesgo de sobreoptimización de parámetros: Debido a la gran cantidad de parámetros, existe el riesgo de sobreajuste a datos históricos, lo que podría provocar un rendimiento deficiente en trading real. La solución es realizar backtesting en múltiples marcos temporales e instrumentos, utilizando configuraciones de parámetros relativamente robustas y evitando optimizaciones excesivas para datos históricos específicos.

-

Riesgo de cambio en las condiciones del mercado: El rendimiento de la estrategia puede diferir en mercados con tendencia y en mercados laterales, y un cambio repentino en las condiciones del mercado podría reducir la eficacia. La solución es introducir un mecanismo de identificación del entorno de mercado, ajustando los parámetros o pausando las operaciones según el estado del mercado.

-

Riesgo de conflicto de señales: El uso simultáneo de múltiples indicadores puede generar señales contradictorias, lo que lleva a decisiones confusas. La solución es establecer pesos razonables para cada indicador, dando más importancia a los más fiables, y asegurando que los umbrales de señal sean adecuados para reducir la probabilidad de conflictos.

-

Riesgo de mala gestión del capital: Aunque la estrategia incluye mecanismos de stop loss, una gestión inadecuada del capital puede provocar un agotamiento rápido de los fondos. La solución es controlar estrictamente el porcentaje de capital asignado a cada operación, asegurando que el riesgo máximo por operación esté dentro de límites asumibles.

-

Riesgo de fallo técnico: Los sistemas de trading automatizados pueden enfrentar problemas técnicos como cortes de red o retrasos en los datos. La solución es establecer mecanismos de intervención manual y monitorizar periódicamente el estado del sistema para gestionar las anomalías a tiempo.

Direcciones de optimización de la estrategia

-

Incorporar un filtro de entorno de mercado: Desarrollar un indicador que identifique si el mercado actual es tendencial o lateral, y ajustar dinámicamente los pesos de cada subestrategia según el estado del mercado: reforzar las estrategias de seguimiento de tendencia en mercados tendenciales y las estrategias de oscilación en mercados laterales.

-

Introducir optimización mediante machine learning: Utilizar técnicas de aprendizaje automático para ajustar automáticamente los parámetros y pesos de cada indicador, permitiendo que la estrategia aprenda y se adapte continuamente a los datos de mercado más recientes, mejorando su capacidad de adaptación dinámica.

-

Añadir análisis de volumen: Incorporar cambios en el volumen como señal adicional de confirmación, ejecutando operaciones solo cuando el volumen respalde la señal esperada, aumentando la credibilidad de las señales.

-

Optimizar el algoritmo de identificación de techos y suelos: Mejorar la lógica actual de identificación de techos y suelos añadiendo más factores de confirmación, como patrones de precios o confirmación en múltiples marcos temporales, para aumentar la precisión.

-

Incorporar indicadores de sentimiento: Integrar indicadores de sentimiento del mercado, como el índice de miedo (VIX) o la relación de opciones call/put, para ajustar la estrategia o pausar las operaciones en momentos de sentimiento extremo, evitando un exceso de trading en períodos de alta volatilidad.

-

Desarrollar mecanismos dinámicos de take profit y stop loss: Ajustar automáticamente los niveles de take profit y stop loss según la volatilidad del mercado: ampliar los rangos de stop loss en mercados de alta volatilidad y reducirlos en mercados de baja volatilidad, haciendo que la gestión de riesgos sea más flexible y efectiva.

-

Optimización de marcos temporales: Añadir funcionalidad de análisis en múltiples marcos temporales, exigiendo confirmación de señales tanto en marcos temporales superiores como inferiores para reducir falsos rompimientos y señales falsas.

Conclusión

La estrategia de trading inteligente con múltiples indicadores ponderados construye un sistema de trading completo y flexible mediante la integración de diversas herramientas de análisis técnico y la asignación de diferentes pesos. Esta estrategia no solo cuenta con confirmación múltiple de señales, sistema de pesos adaptativo y funciones completas de gestión de riesgos, sino que también incluye un mecanismo automatizado de identificación de posibles techos y suelos, lo que le confiere una gran capacidad de adaptación en entornos de mercado complejos y cambiantes.

Aunque existen riesgos potenciales como la sobreoptimización de parámetros, cambios en las condiciones del mercado y conflictos de señales, estos pueden controlarse eficazmente mediante una configuración razonable de parámetros, identificación del entorno de mercado y una estricta gestión del capital. Las direcciones futuras de optimización incluyen la incorporación de filtros de entorno de mercado, la introducción de técnicas de machine learning, el refuerzo del análisis de volumen y la mejora del algoritmo de identificación de techos y suelos, entre otros. Estas mejoras aumentarán aún más la estabilidad y rentabilidad de la estrategia.

Para los inversores que buscan un método de trading sistemático, esta estrategia de trading inteligente con múltiples indicadores ponderados ofrece un marco digno de consideración. No solo reduce la influencia de los factores emocionales en las decisiones de trading, sino que también permite optimizar continuamente el rendimiento del trading mediante un enfoque basado en datos. Al implementar esta estrategia, se recomienda comenzar con una configuración de parámetros conservadora, realizar ajustes graduales y monitorizar de cerca el rendimiento de la estrategia para encontrar la configuración que mejor se adapte a la tolerancia al riesgo y a las condiciones del mercado individuales.

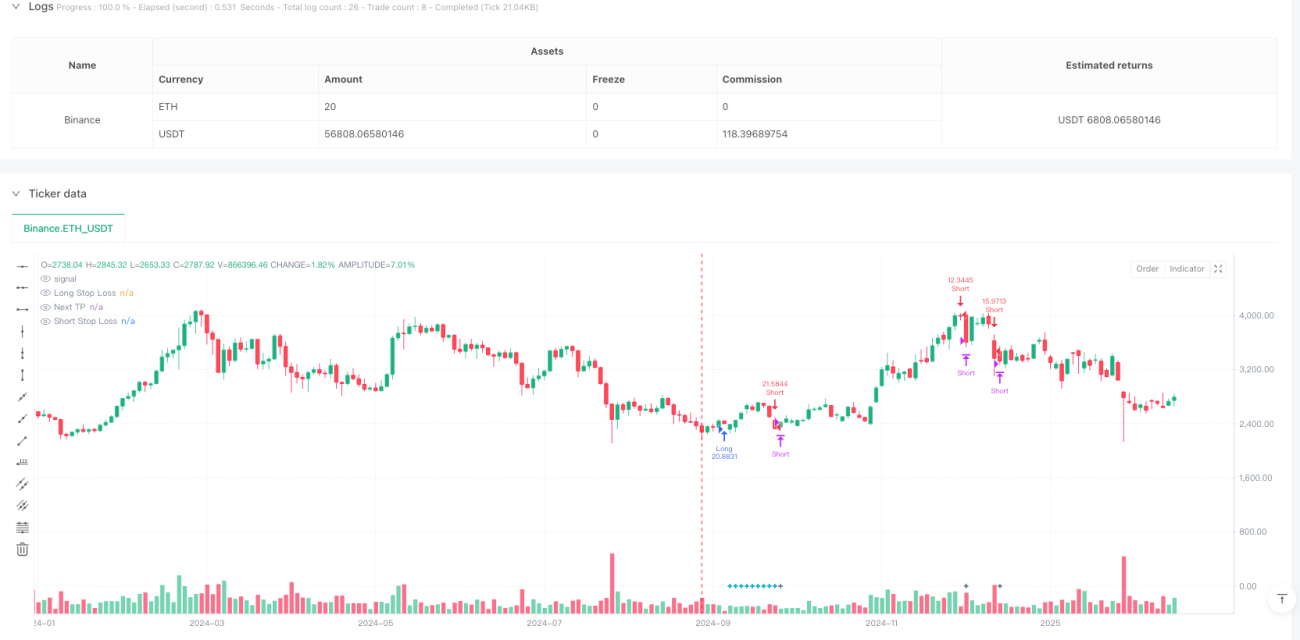

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1