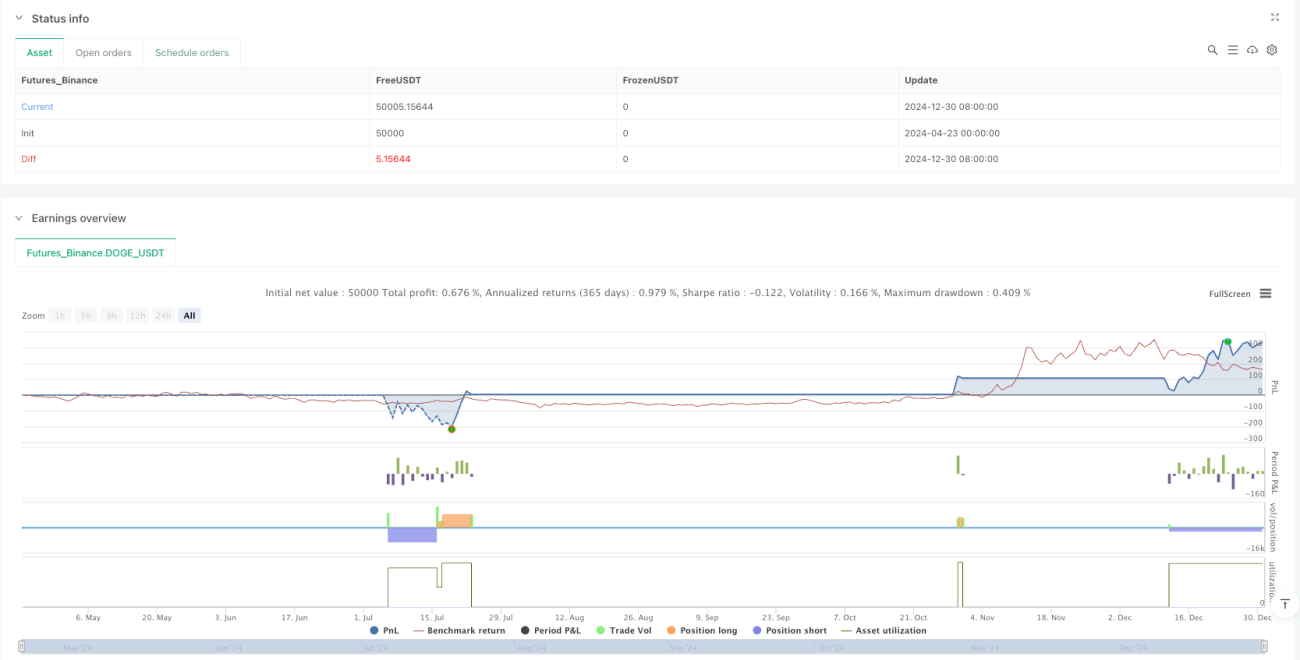

Resumen

Esta estrategia es un sistema de seguimiento de tendencias multifactorial que combina el indicador de parada y reversión (SAR), la media móvil exponencial (EMA), el índice de fuerza relativa (RSI) y el índice de movimiento direccional promedio (ADX). Identifica posibles direcciones de tendencia mediante la sinergia de múltiples indicadores técnicos y genera señales de trading cuando se confirma la tendencia. La estrategia también emplea un método dinámico de gestión de riesgos basado en el rango verdadero promedio (ATR), calculando automáticamente los niveles de stop loss y take profit.

Principio de la estrategia

- Confirmación de tendencia: Cuando el precio supera el SAR y el precio de cierre está por encima de la EMA rápida, se confirma una tendencia alcista; cuando el precio cae por debajo del SAR y el precio de cierre está por debajo de la EMA rápida, se confirma una tendencia bajista.

- Filtro de impulso: Se utiliza el RSI para filtrar las señales, exigiendo RSI > 60 para posiciones largas y RSI < 40 para posiciones cortas, asegurando que las operaciones se realicen en la dirección de un impulso fuerte.

- Validación de la fuerza de la tendencia: Se verifica la fuerza de la tendencia mediante el ADX (umbral 30), evitando operar en mercados laterales.

- Gestión de riesgos: Se calcula un stop loss dinámico (1.5 veces el ATR) y un take profit (2 veces el ATR) basados en el ATR, y el tamaño de la posición se determina como un porcentaje fijo del capital de la cuenta (por defecto 2%).

Ventajas de la estrategia

- Validación multifactorial: La verificación múltiple mediante SAR, EMA, RSI y ADX mejora significativamente la calidad de las señales.

- Gestión dinámica de riesgos: El stop loss y take profit basados en ATR se adaptan automáticamente a los cambios en la volatilidad del mercado.

- Filtro de fuerza de tendencia: El umbral del ADX filtra eficazmente las falsas rupturas, operando solo en mercados con tendencia fuerte.

- Cálculo automatizado de posición: La gestión de riesgos basada en el riesgo garantiza una exposición consistente por operación.

- Retroalimentación visual clara: Las señales de trading se muestran de forma intuitiva con fondos de colores.

Riesgos de la estrategia

- Riesgo de retraso: SAR y EMA son indicadores de seguimiento de tendencia, que pueden presentar retraso en los cambios de tendencia.

- Sensibilidad a los parámetros: Los períodos cortos del RSI (6) y de la EMA (2) pueden provocar un exceso de operaciones.

- Riesgo del umbral ADX: Un umbral fijo de ADX (30) puede comportarse de manera inestable en diferentes condiciones de mercado.

- Riesgo de amplificación de la volatilidad: Un multiplicador fijo del ATR puede resultar en stops demasiado amplios durante episodios de volatilidad extrema.

Soluciones:

- Optimizar dinámicamente el umbral del ADX y los parámetros del RSI.

- Añadir un filtro de volatilidad (por ejemplo, el índice VIX).

- Utilizar una gestión de posición progresiva en lugar de un porcentaje fijo.

Direcciones de optimización

- Parametrización dinámica: Convertir los parámetros fijos en dinámicos según el estado del mercado, por ejemplo, ajustando el multiplicador del ATR según la volatilidad.

- Integración de aprendizaje automático: Entrenar modelos con datos históricos para optimizar la combinación de parámetros de los indicadores.

- Confirmación en múltiples marcos temporales: Añadir confirmación de tendencia en marcos temporales superiores.

- Filtro de volatilidad anómala: Pausar las operaciones durante eventos noticiosos importantes.

- Estrategia de salida compuesta: Combinar mecanismos de salida como el trailing stop y la salida por tiempo.

Conclusión

Esta estrategia multifactorial de tendencia muestra un rendimiento excelente en mercados con tendencia, gracias a la sinergia de indicadores y una gestión de riesgos rigurosa. Su principal fortaleza reside en la validación múltiple de las señales y el control dinámico del riesgo, pero se debe prestar atención a la sensibilidad de los parámetros y al riesgo de retraso. Las optimizaciones futuras deberían enfocarse en mecanismos de adaptación de parámetros y en la identificación del estado del mercado para mejorar la robustez de la estrategia.

- 1