Estrategia cuantitativa de divergencia dinámica del RSI

Resumen

El Estrategia Cuantitativa de Divergencia de Doble Pivote RSI es una estrategia de trading avanzada que identifica oportunidades de reversión potencial mediante la detección de divergencias alcistas y bajistas regulares entre la acción del precio y el Índice de Fuerza Relativa (RSI). Esta estrategia emplea un algoritmo automatizado de detección de puntos pivote, combinado con dos métodos diferentes de gestión de stop loss/take profit, abriendo posiciones automáticamente cuando se confirma una señal de divergencia. El núcleo de la estrategia radica en verificar mediante cálculos matemáticos precisos la divergencia entre el precio y el indicador RSI, y utilizar un mecanismo de gestión de riesgos dinámico para garantizar que cada operación cumpla con una relación riesgo-beneficio predefinida.

Principios de la Estrategia

- Módulo de cálculo del RSI: Se utiliza el método de suavizado de Wilder para calcular el valor del RSI de 14 períodos (ajustable), empleando el precio de cierre como fuente de entrada predeterminada (configurable).

- Detección de puntos pivote:

- Se utiliza una ventana deslizante de 5 períodos (ajustable) a izquierda y derecha para detectar máximos y mínimos locales del indicador RSI.

- Mediante la función

ta.barssincese garantiza que entre los puntos pivote haya un intervalo de 5 a 60 velas (rango ajustable).

- Lógica de confirmación de divergencia:

- Divergencia alcista: el precio forma un nuevo mínimo mientras el RSI forma un mínimo más alto.

- Divergencia bajista: el precio forma un nuevo máximo mientras el RSI forma un máximo más bajo.

- Sistema de ejecución de operaciones:

- Mecanismo de stop loss de modo dual: basado en el punto de giro de los últimos 20 períodos (ajustable) o en la amplitud de la volatilidad del ATR.

- Cálculo dinámico del take profit: según el monto del riesgo multiplicado por la relación riesgo-beneficio preestablecida (predeterminada 2:1).

- Sistema de visualización: se marcan en el gráfico todas las señales de divergencia válidas y se muestran en tiempo real las líneas horizontales de stop loss (rojo) y take profit (verde) de la posición actual.

Análisis de Ventajas

- Mecanismo de verificación multidimensional: exige que tanto el precio como el RSI cumplan simultáneamente una forma específica, y que el intervalo de tiempo esté dentro del rango preestablecido, lo que reduce significativamente la probabilidad de señales falsas.

- Gestión de riesgos adaptativa:

- El modo de puntos de giro es adecuado para mercados con tendencia, capturando eficazmente movimientos de oleada.

- El modo ATR es adecuado para mercados laterales, ajustando automáticamente la amplitud del stop loss según la volatilidad.

- Parámetros altamente configurables: todos los parámetros clave (período del RSI, rango de detección de pivotes, relación riesgo-beneficio, etc.) se pueden ajustar según las características del mercado.

- Gestión de capital científica: se adopta de forma predeterminada una proporción de posición del 10%, evitando una exposición excesiva al riesgo en una sola operación.

- Retroalimentación visual en tiempo real: mediante marcas en el gráfico y líneas dinámicas de stop loss/take profit, se proporciona un soporte de decisión de trading intuitivo.

Análisis de Riesgos

- Riesgo de retraso: el RSI, como indicador rezagado, puede generar señales tardías en movimientos unidireccionales bruscos. Mitigación: combinar con un filtro de tendencia o acortar el período del RSI.

- Riesgo en mercados laterales: en ausencia de una tendencia clara pueden generarse señales falsas consecutivas. Mitigación: activar el modo ATR y aumentar el multiplicador, o añadir un filtro de volatilidad.

- Riesgo de sobreajuste de parámetros: ciertas combinaciones de parámetros pueden funcionar bien en datos históricos pero fallar en operaciones reales. Mitigación: realizar pruebas de estrés en múltiples plazos y múltiples instrumentos.

- Riesgo de condiciones extremas: los gaps de precios pueden invalidar el stop loss. Mitigación: evitar operar antes y después de eventos económicos importantes, o utilizar cobertura con opciones.

- Dependencia del marco temporal: el rendimiento varía considerablemente entre diferentes plazos. Mitigación: realizar una optimización de backtesting exhaustiva en el marco temporal objetivo.

Direcciones de Optimización

- Verificación con indicadores compuestos: agregar MACD o indicadores de volumen como segunda confirmación para mejorar la calidad de las señales.

- Ajuste dinámico de parámetros: ajustar automáticamente el período del RSI y el multiplicador ATR según la volatilidad del mercado.

- Optimización con machine learning: utilizar algoritmos genéticos para optimizar combinaciones de parámetros clave.

- Análisis de múltiples marcos temporales: introducir un filtro de dirección de tendencia de un marco temporal superior.

- Gestión dinámica de posiciones: ajustar el tamaño de la posición según la volatilidad para lograr un equilibrio de riesgos.

- Filtro de eventos: integrar datos del calendario económico para evitar operar antes y después de la publicación de datos importantes.

Conclusión

La Estrategia Cuantitativa de Divergencia de Doble Pivote RSI ofrece un método estructurado de trading de reversión mediante la identificación sistemática de divergencias y una gestión de riesgos rigurosa. Su valor central radica en transformar conceptos tradicionales de análisis técnico en reglas de trading cuantificables, y adaptarse a diferentes entornos de mercado mediante un mecanismo de stop loss de modo dual. El buen rendimiento de la estrategia requiere tres elementos clave: una optimización adecuada de parámetros, un control de riesgos estricto y una disciplina de ejecución consistente. Esta estrategia es especialmente adecuada para entornos de mercado con cierta volatilidad pero sin tendencias extremas, y constituye una excelente plantilla para que los traders intermedios hagan la transición al trading cuantitativo.

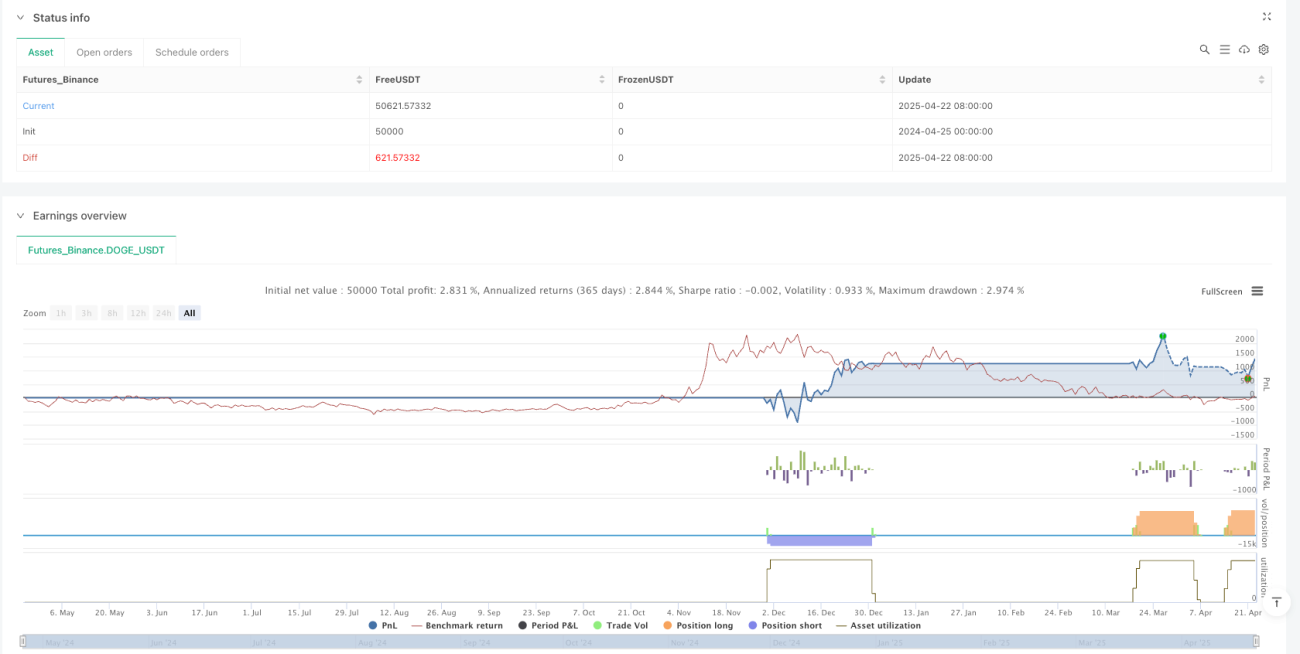

/*backtest

start: 2024-04-25 00:00:00

end: 2025-04-23 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"DOGE_USDT"}]

*/

//@version=6

strategy("RSI Divergence Strategy - AliferCrypto", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// === RSI Settings ===- 1