Resumen

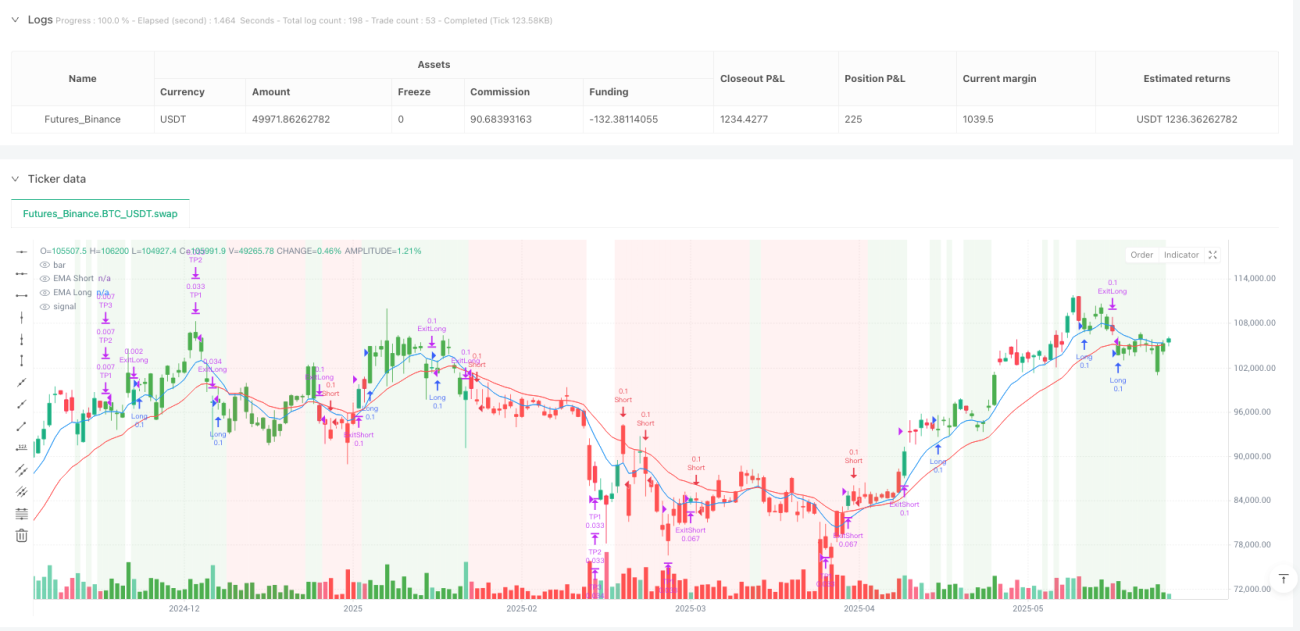

El Estrategia de Seguimiento de Volatilidad Dinámica Multiperiodo es un sistema de trading a corto plazo que combina el cruce de medias móviles exponenciales (EMA) rápidas/lentas con un filtro del Índice de Fuerza Relativa (RSI). Esta estrategia se centra en buscar oportunidades de retroceso dentro de la tendencia dominante a corto plazo, reduciendo el ruido mediante múltiples mecanismos de confirmación. Sus características principales incluyen control de riesgo basado en el Rango Verdadero Promedio (ATR), un trailing stop adaptativo, ajuste del stop basado en volumen y tres objetivos de toma de ganancias parciales. Además, la estrategia incorpora una verificación del RSI en un marco temporal superior como mecanismo de salida temprana de advertencia, evitando permanecer demasiado tiempo en tendencias desfavorables.

Principio de la Estrategia

El principio de funcionamiento de la estrategia se basa en una arquitectura de pilas de señales de múltiples capas:

- Identificación de tendencia: Se determina la dirección de la microtendencia mediante el cruce de la EMA rápida y la EMA lenta. Cuando la EMA rápida está por encima de la EMA lenta, se identifica una tendencia alcista; por el contrario, es bajista.

- Filtro de salud del impulso: Evita perseguir movimientos excesivamente extendidos. Solo se permite tomar posiciones largas cuando el RSI está por debajo del nivel de sobrecompra; solo se permite tomar posiciones cortas cuando el RSI está por encima del nivel de sobreventa.

- Mecanismo de confirmación de velas: Exige que las condiciones de señal se mantengan durante múltiples velas consecutivas, filtrando eficazmente el ruido del mercado.

- Activación de entrada: Se emite una orden de mercado cuando aparece la vela que completa la ventana de confirmación.

- Stop loss inicial: Ajuste de volatilidad basado en ATR, con ajuste dinámico según el volumen relativo.

- Lógica de trailing stop: Combinación óptima de puntos pivote y stop loss base ATR para asegurar ganancias.

- Monitorización del RSI en marco temporal superior: Proporciona señales de salida del contexto del mercado, evitando operar contra la tendencia.

- Objetivos de ganancias escalonados: Se establecen tres objetivos basados en ATR para reducir progresivamente la posición.

- Limitador de operaciones: Limita el número máximo de operaciones por fase de tendencia para evitar el exceso de trading.

La innovación clave de la estrategia radica en la integración orgánica de múltiples indicadores técnicos con indicadores de comportamiento del mercado (como volumen y volatilidad), formando un sistema de trading altamente adaptable que ajusta automáticamente sus parámetros en diferentes condiciones del mercado.

Ventajas de la Estrategia

- Alta adaptabilidad: Los stops y objetivos ajustados por ATR permiten que la estrategia se adapte a diferentes condiciones de volatilidad del mercado sin necesidad de reoptimizar parámetros con frecuencia.

- Gestión de riesgo multicapa: Combina stop loss inicial, trailing stop, toma de ganancias parcial y filtros RSI de múltiples periodos para formar un sistema completo de control de riesgo.

- Mecanismo de filtrado de ruido: El requisito de confirmación de velas consecutivas reduce eficazmente las señales falsas, mejorando la calidad de las operaciones.

- Percepción de liquidez: Ajusta el nivel de stop loss mediante el ratio de volumen, reduciendo automáticamente la exposición al riesgo en entornos de baja liquidez.

- Monitorización de la madurez de la tendencia: A medida que la tendencia se desarrolla, reduce automáticamente el número de operaciones permitidas, evitando el exceso de trading en fases tardías.

- Mecanismo flexible de toma de ganancias: La estrategia de toma de ganancias parcial en tres niveles permite asegurar parte de las ganancias cuando el precio se mueve a favor, manteniendo al mismo tiempo el potencial de subida.

- Análisis entre periodos: La monitorización del RSI en un marco temporal superior proporciona una perspectiva más amplia del contexto del mercado, evitando aferrarse a señales microscópicas durante cambios importantes de tendencia.

- Facilidad de ejecución: A través de la integración con PineConnector, se puede automatizar la estrategia fácilmente, reduciendo la intervención humana y el impacto emocional.

Riesgos de la Estrategia

- Riesgo de retroceso: A pesar de las múltiples capas de control de riesgo, en condiciones extremas del mercado (como gaps o flash crashes), la estrategia aún podría enfrentar retrocesos mayores a los esperados. La solución es reducir el tamaño de la posición o aumentar el múltiplo del ATR.

- Sensibilidad a los parámetros: Ciertos parámetros clave, como la longitud de las EMAs y los umbrales del RSI, tienen un impacto significativo en el rendimiento de la estrategia. Una optimización excesiva puede conllevar riesgo de sobreajuste. Se recomienda utilizar pruebas hacia adelante en lugar de optimización dentro de la muestra.

- Costos de trading por alta frecuencia: Como estrategia a corto plazo, la frecuencia de trading es alta, y los costos acumulados (spread, comisiones) pueden afectar significativamente los beneficios reales. Se deben considerar los costos reales de trading en las pruebas retrospectivas.

- Riesgo de latencia: La latencia de ejecución de PineConnector (aproximadamente 100-300 ms) puede aumentar el deslizamiento en mercados de alta volatilidad. No se recomienda su uso en mercados extremadamente volátiles o con baja liquidez.

- Redibujo de puntos pivote: En gráficos de plazos muy cortos (por debajo de minutos), los puntos pivote pueden redibujarse durante la formación de la vela en tiempo real, afectando la precisión del stop loss.

- Retraso en la identificación de tendencias: La identificación basada en cruces de EMA tiene un retraso inherente, lo que puede hacer que se pierdan parte de los movimientos al inicio de una tendencia.

- Riesgo de apalancamiento excesivo: Si se configura un multiplicador de posición demasiado grande, podría generar un riesgo excesivo en una sola operación, agotando rápidamente el capital de la cuenta.

Direcciones de Optimización de la Estrategia

- Optimización con machine learning: Introducir algoritmos de aprendizaje automático para ajustar dinámicamente los parámetros de EMA y RSI, adaptándose a diferentes condiciones del mercado. Esto resolvería el problema de adaptabilidad insuficiente de los parámetros fijos en distintas fases del mercado.

- Clasificación del estado del mercado: Incorporar análisis de agrupamiento de volatilidad para dividir el mercado en estados de volatilidad alta, media y baja, adoptando parámetros diferenciados para cada estado. Esto mejoraría la adaptabilidad en mercados en transición.

- Mecanismo de consenso de múltiples indicadores: Integrar otros indicadores de impulso y tendencia (como MACD, Bandas de Bollinger, KDJ) para formar un sistema de consenso, generando señales solo cuando la mayoría de los indicadores coinciden. Esto ayuda a reducir señales falsas.

- Filtro temporal inteligente: Añadir análisis de los períodos del mercado y patrones de volatilidad, evitando sesiones de baja eficiencia y eventos de alta volatilidad conocidos (como publicaciones de datos económicos importantes).

- Proporción dinámica de toma de ganancias parciales: Ajustar automáticamente el porcentaje de toma de ganancias y la distancia objetivo según la volatilidad del mercado y la fuerza de la tendencia, reteniendo más posición en tendencias fuertes y tomando ganancias más agresivamente en tendencias débiles.

- Fortalecimiento del control de retrocesos: Introducir un mecanismo de riesgo adaptativo basado en patrones históricos de retroceso, reduciendo automáticamente la frecuencia de trading o aumentando la distancia del stop loss al detectar precursores similares a grandes retrocesos pasados.

- Mejora con datos de alta frecuencia: Cuando sea posible, integrar datos de tick para optimizar la entrada, reduciendo el deslizamiento y mejorando el precio de entrada.

- Análisis de correlación entre mercados: Añadir análisis de correlación con mercados relacionados, aprovechando las relaciones de adelanto-retraso entre mercados para mejorar la calidad de las señales.

Resumen

El Estrategia de Seguimiento de Volatilidad Dinámica Multiperiodo es un sistema de trading a corto plazo que combina herramientas clásicas de análisis técnico con métodos cuantitativos modernos de gestión de riesgos. A través de una arquitectura de pilas de señales de múltiples capas, que integra identificación de tendencia con EMA, filtrado de impulso con RSI, mecanismo de confirmación de velas consecutivas, ajuste de volatilidad con ATR y análisis multiperiodo, construye un marco integral de toma de decisiones de trading. Su característica más notable es la adaptabilidad: ajusta automáticamente los parámetros de trading y las medidas de control de riesgo según la volatilidad del mercado, el volumen y la madurez de la tendencia.

Aunque existen algunos riesgos inherentes, como la sensibilidad a los parámetros, los costos de trading de alta frecuencia y el riesgo de latencia, estos pueden ser controlados eficazmente mediante una gestión adecuada del capital y una optimización continua. Las futuras direcciones de optimización se centran principalmente en la optimización de parámetros con machine learning, la clasificación del estado del mercado, los mecanismos de consenso de múltiples indicadores y la gestión dinámica del riesgo.

Para los traders que buscan capturar oportunidades de retroceso dentro de la tendencia en mercados a corto plazo, esta estrategia ofrece un marco estructurado que equilibra la captura de oportunidades de trading con el control de riesgos. Sin embargo, como con todas las estrategias de trading, se recomienda probarla ampliamente en una cuenta demo antes de su aplicación real, y ajustar los parámetros según la tolerancia al riesgo personal y el tamaño del capital.

- 1