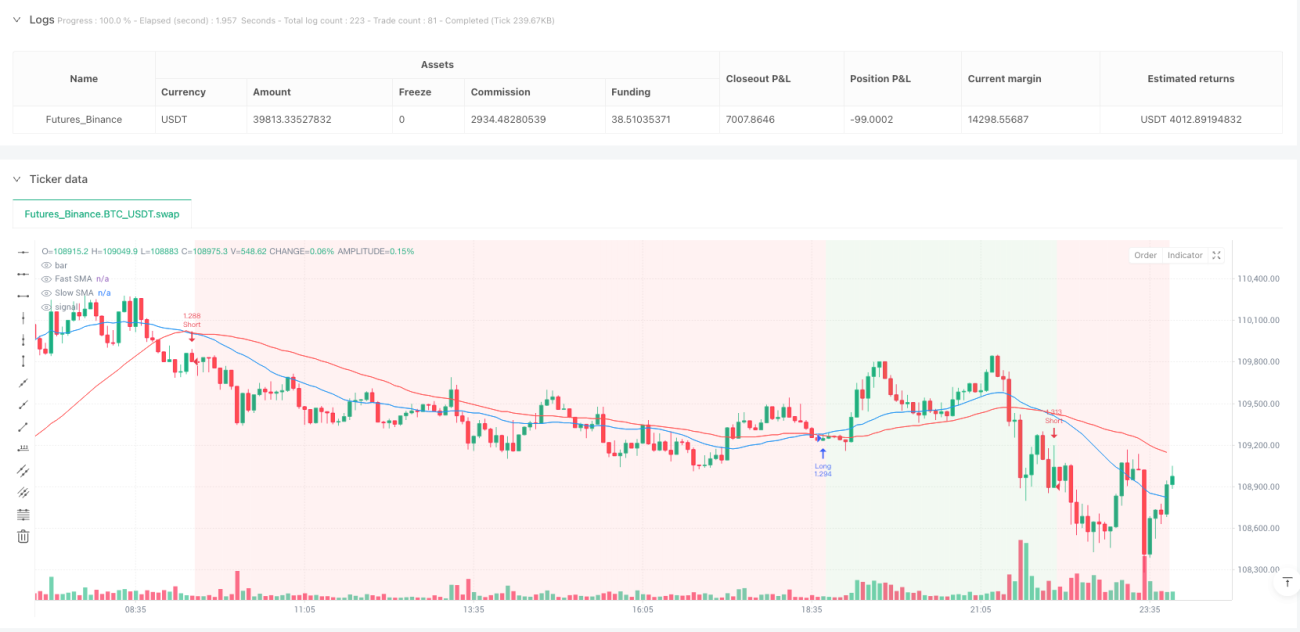

Estrategia de seguimiento de tendencia con cruce de medias móviles dobles y sistema avanzado de gestión de riesgos

Resumen de la Estrategia

La Estrategia de Seguimiento de Tendencia con Cruce de Medias Móviles Dobles es un sistema de trading cuantitativo que combina análisis técnico con una gestión integral del riesgo. El núcleo de la estrategia utiliza las señales de cruce entre una Media Móvil Simple rápida (Fast SMA) y una Media Móvil Simple lenta (Slow SMA) para identificar cambios en la tendencia del mercado, y asegura la seguridad del capital mediante múltiples mecanismos de control de riesgo. La estrategia está implementada en la plataforma Pine Script y es adecuada para el trading de seguimiento de tendencia en una variedad de instrumentos.

Principio de la Estrategia

La estrategia toma decisiones comerciales basándose en la interacción entre dos medias móviles simples:

-

Mecanismo de generación de señales:

- Señal de compra (long): cuando la SMA rápida (por defecto 24 períodos) cruza por encima de la SMA lenta (por defecto 48 períodos)

- Señal de venta (short): cuando la SMA rápida cruza por debajo de la SMA lenta

- Señal de cierre: cuando ocurre un cruce en la dirección opuesta

-

Control de momento de ejecución:

La estrategia ejecuta todas las decisiones comerciales al cierre de la vela (barra), evitando el sesgo de anticipación (look-ahead bias) y garantizando la fiabilidad y realidad de los resultados del backtesting. -

Sistema de gestión de capital:

- Control de riesgo por operación: por defecto, se limita el riesgo máximo de cada operación al 2.0% del capital total de la cuenta

- Cálculo automático del tamaño de la posición: se ajusta dinámicamente en función de la distancia al stop loss y el monto de riesgo, asegurando que no se exceda el límite de riesgo preestablecido

-

Control de riesgo multinivel:

- Stop Loss fijo: se establece inmediatamente después de entrar en la operación un stop loss con un porcentaje fijo (por defecto 0.8%) para limitar la pérdida de cada operación

- Take Profit: se calcula automáticamente basado en la relación riesgo/recompensa (por defecto 2.0), por ejemplo, un stop loss del 0.8% combinado con una relación riesgo/recompensa de 2.0 da un objetivo de ganancia del 1.6%

- Trailing Stop Loss avanzado:

- Condición de activación: se activa cuando las ganancias alcanzan un porcentaje preestablecido (por defecto 1.0%)

- Mecanismo de trailing: una vez activado, el precio de stop loss sigue el precio más alto (para posiciones largas) o el precio más bajo (para posiciones cortas), manteniendo una distancia especificada (por defecto 0.5%)

- Garantía de seguridad: asegura que el trailing stop nunca esté por debajo del nivel de stop loss inicial, protegiendo el capital mientras permite que las ganancias sigan creciendo

Esta estrategia captura tendencias mediante el cruce de medias móviles y utiliza medidas integrales de gestión de riesgos para garantizar la seguridad y sostenibilidad de las operaciones.

Ventajas de la Estrategia

-

Mecanismo robusto de identificación de tendencias:

- El sistema de cruce de medias móviles dobles es un indicador clásico de seguimiento de tendencia, con eficacia y estabilidad validadas históricamente.

- Ajustando los períodos de las medias rápidas y lentas, se puede adaptar a las características de tendencia de diferentes entornos de mercado y marcos temporales.

-

Gestión precisa del capital:

- Asignación dinámica del riesgo basada en el valor neto de la cuenta, asegurando que el riesgo de cada operación permanezca siempre dentro de límites controlables.

- El tamaño de la posición se ajusta automáticamente según la distancia real al stop loss, evitando problemas de apalancamiento excesivo o tamaño de posición demasiado pequeño.

- El sistema incluye mecanismos de seguridad incorporados para prevenir errores de cálculo en condiciones extremas.

-

Protección multinivel contra riesgos:

- El stop loss fijo proporciona protección básica, limitando la pérdida máxima.

- El objetivo de ganancias basado en la relación riesgo/recompensa asegura que las ganancias promedio superen las pérdidas promedio.

- El mecanismo de trailing stop loss avanzado protege las ganancias ya obtenidas sin afectar el potencial de ganancias de la continuación de la tendencia.

-

Control temporal de la ejecución de operaciones:

- Todas las decisiones comerciales se ejecutan estrictamente al precio de cierre de la vela, evitando el sesgo de anticipación.

- El parámetro

process_orders_on_close=truegarantiza que el procesamiento de órdenes se ajuste a un entorno de trading real. - La lógica de trading se basa en las señales de la vela anterior, evitando el uso de datos futuros.

-

Sistema de trailing stop loss adaptativo:

- El trailing stop loss solo se activa después de que la operación alcanza un nivel de ganancia preestablecido, evitando una activación prematura.

- El nivel de stop loss se ajusta automáticamente a medida que el precio se mueve, asegurando parte de las ganancias mientras permite que la tendencia continúe.

- El mecanismo de protección incorporado garantiza que el trailing stop no caiga por debajo del nivel de stop loss inicial, proporcionando una protección continua contra riesgos.

Riesgos de la Estrategia

-

Retraso en la identificación de tendencias:

- Las medias móviles son indicadores inherentemente rezagados y pueden reaccionar con retraso en los puntos de inflexión de la tendencia.

- En mercados laterales (sin tendencia), pueden generar señales falsas frecuentes, provocando el "efecto sierra" (Whipsaw).

- Mitigación: se puede considerar agregar condiciones de filtro adicionales, como indicadores de volatilidad o confirmación de la fuerza de la tendencia.

-

Problemas de adaptabilidad de parámetros fijos:

- La efectividad de los períodos SMA predeterminados (24 y 48) puede variar según el mercado y el marco temporal.

- Los porcentajes fijos de stop loss y take profit pueden no ser adecuados en todos los entornos de volatilidad.

- Mitigación: se recomienda ajustar los parámetros según las características específicas del instrumento y la volatilidad histórica, o introducir mecanismos de parámetros adaptativos.

-

Momento de activación del trailing stop:

- Si el nivel de ganancia para activar el trailing stop (por defecto 1.0%) se establece demasiado alto, se pueden perder oportunidades de asegurar ganancias.

- Si se establece demasiado bajo, puede activarse prematuramente, limitando las ganancias potenciales.

- Mitigación: ajustar los parámetros del trailing stop en función de la proporción del Rango Verdadero Medio (ATR) del instrumento objetivo, haciéndolo más adaptativo.

-

Riesgo de gestión de capital:

- Para instrumentos de volatilidad muy baja, un stop loss de porcentaje fijo puede resultar en posiciones demasiado grandes.

- En condiciones extremas del mercado (como gaps o flash crashes), puede que no sea posible ejecutar al precio de stop loss preestablecido.

- Mitigación: considerar establecer límites máximos de posición, o ajustar dinámicamente los parámetros de riesgo basándose en indicadores de volatilidad (como ATR).

-

Limitaciones de implementación técnica:

- La lógica alternativa cuando el porcentaje de stop loss se establece en cero o negativo puede generar riesgos inesperados.

- No se consideran los costos de transacción ni el deslizamiento en el rendimiento real de la estrategia.

- Mitigación: mejorar la lógica de manejo de errores, agregar más verificaciones de seguridad e incluir los costos de transacción en el backtesting.

Direcciones de Optimización de la Estrategia

-

Optimización del mecanismo de generación de señales:

- Introducir períodos adaptativos de medias móviles: ajustar dinámicamente los períodos de las medias rápidas y lentas según la volatilidad del mercado, mejorando la adaptabilidad a diferentes entornos.

- Agregar indicadores de confirmación adicionales: combinar indicadores como el Índice de Fuerza Relativa (RSI), Estocástico (Stochastic) o MACD para filtrar señales de baja calidad.

- Considerar el análisis de estructura de precios: integrar factores como soporte/resistencia y reconocimiento de patrones de precios para mejorar la calidad de las señales.

-

Mejora del sistema de gestión de riesgos:

- Stop loss adaptativo a la volatilidad: establecer la distancia de stop loss dinámicamente basada en indicadores de volatilidad como ATR, en lugar de un porcentaje fijo.

- Estrategia de trailing stop escalonado: implementar trailing stop de múltiples niveles, con una distancia de seguimiento que se reduce progresivamente a medida que aumentan las ganancias.

- Control de drawdown máximo: agregar un mecanismo de ajuste de riesgo basado en el porcentaje de drawdown máximo de la cuenta, reduciendo automáticamente el riesgo en entornos de mercado desfavorables.

-

Optimización de la entrada:

- Filtro de fuerza de tendencia: ejecutar señales de trading solo cuando la fuerza de la tendencia alcanza un umbral determinado.

- Filtro de ventana de volatilidad: operar solo en entornos de volatilidad adecuados, evitando mercados con volatilidad excesiva o insuficiente.

- Mejor precio de ejecución: investigar el mejor momento y nivel de precio para entrar después de la generación de la señal.

-

Marco de backtesting y evaluación:

- Consistencia en múltiples marcos temporales: verificar la consistencia y robustez de la estrategia en diferentes marcos temporales.

- Análisis de sensibilidad: probar exhaustivamente el impacto de los cambios en cada parámetro sobre el rendimiento de la estrategia, identificando las combinaciones de parámetros más estables.

- Simulación de Monte Carlo: evaluar la distribución de probabilidad y robustez de la estrategia mediante la aleatorización de los resultados de las operaciones.

-

Mejora de la implementación técnica:

- Mejorar el manejo de errores: reforzar el tratamiento de casos límite para garantizar un funcionamiento estable de la estrategia en todo tipo de condiciones de mercado.

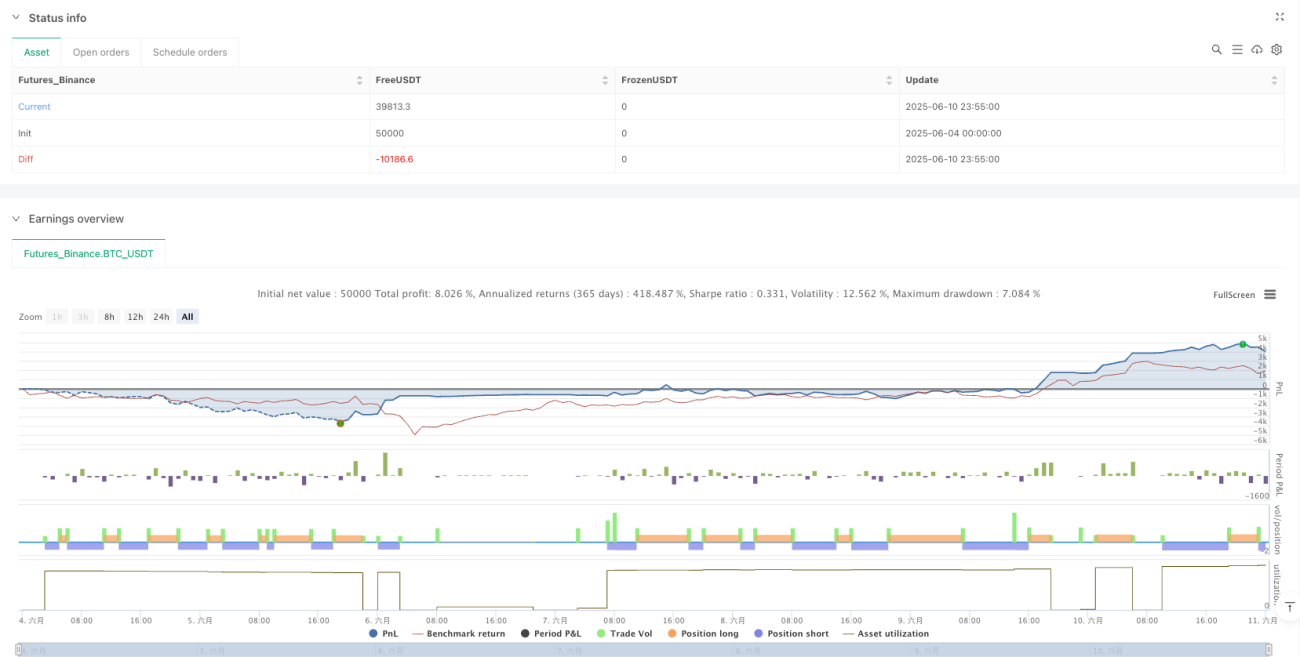

- Agregar monitoreo de indicadores de rendimiento: realizar un seguimiento en tiempo real de indicadores clave como el Ratio de Sharpe, drawdown máximo, etc.

- Visualización del estado de la estrategia: mejorar la interfaz gráfica para mostrar de forma intuitiva el estado de la estrategia, las posiciones abiertas y el nivel de riesgo.

Conclusión

La Estrategia de Seguimiento de Tendencia con Cruce de Medias Móviles Dobles es un sistema de trading completo que combina un método clásico de análisis técnico con conceptos modernos de gestión de riesgos. Su principal ventaja radica en el mecanismo simple y claro de identificación de tendencias junto con un sistema de control de riesgos multinivel. En particular, su precisa gestión de capital y su avanzado mecanismo de trailing stop loss ofrecen a la estrategia un buen potencial de rentabilidad ajustada al riesgo.

Sin embargo, la estrategia también enfrenta desafíos como el retraso inherente de las medias móviles y la adaptabilidad de los parámetros. Mediante la introducción de parámetros adaptativos, la mejora de los mecanismos de filtrado de señales y la optimización del sistema de gestión de riesgos, se podría mejorar aún más el rendimiento de la estrategia.

En general, se trata de un marco de estrategia cuantitativa bien estructurado y lógico, adecuado como base para sistemas de seguimiento de tendencia a mediano y largo plazo, especialmente en mercados con características de tendencia claras. Para los traders, comprender y dominar los principios de gestión de riesgos es más importante que copiar los parámetros de la estrategia, y esta es la parte más valiosa de la estrategia.

- 1