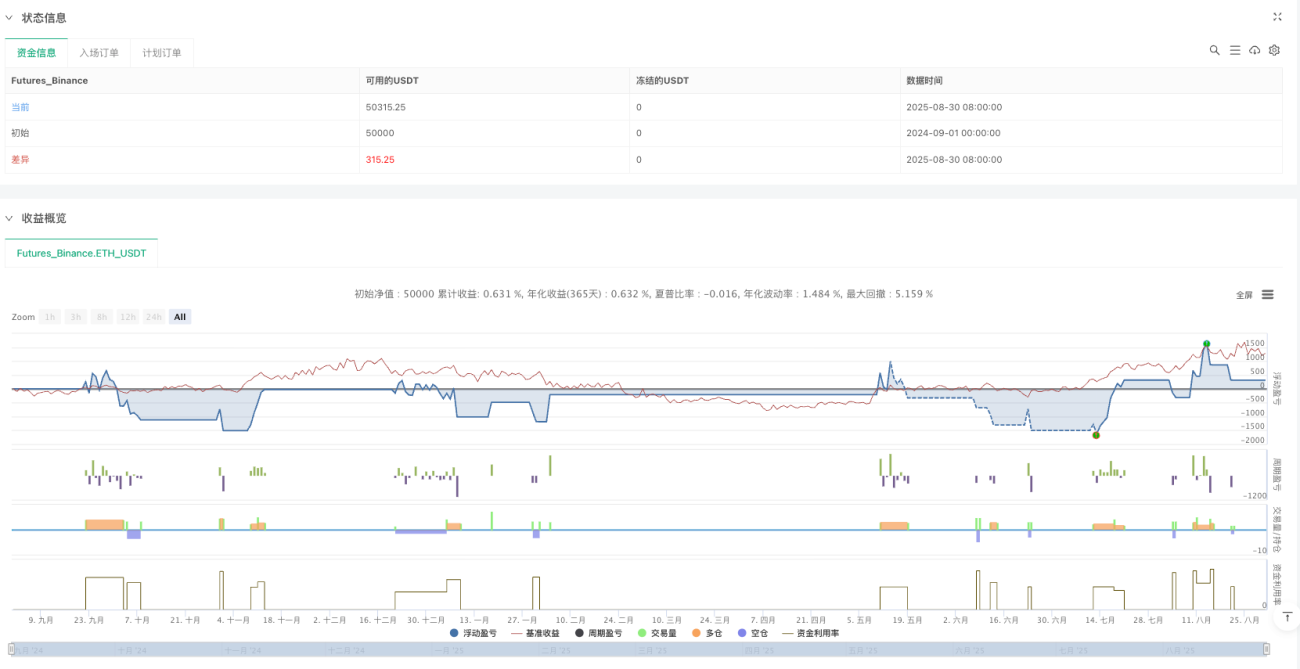

🎯 ¿Qué tan potente es realmente esta estrategia?

¿Sabías que el 90% de los traders en el mercado compran en máximos y venden en mínimos, pero los verdaderos expertos buscan la "zona de vacío de precios"? ¡Este Advanced FVG Strategy Pro+ está diseñado específicamente para capturar esos misteriosos huecos, un superarma 🚀

FVG (Fair Value Gap) es simplemente la "zona en blanco" que queda cuando el precio salta, como cuando saltas un charco al caminar; tarde o temprano tendrá que volver a "rellenar el hueco". Esta estrategia consiste en emboscarse en el mejor momento junto al "borde del hueco" esperando que el pez muerda el anzuelo.

💡 ¡Puntos clave! Tres tecnologías centrales de vanguardia

1. Análisis en múltiples marcos temporales 📊

¡Ya no te limitas a un solo período! La estrategia puede ejecutarse en gráfico de 5 minutos pero usando señales FVG de 1 hora. Es como usar un telescopio para ver montañas lejanas y una lupa para ver detalles, ¡una visión más completa!

2. Filtro de tendencia IIR 🌊

¡Esto no es una media móvil común! Utiliza un filtro paso bajo IIR de nivel ingenieril que identifica con precisión la dirección de la tendencia. Imagínate esto como instalar un "radar de tendencia" en tus operaciones, ¡atacando solo cuando el viento sopla a favor!

3. Gestión inteligente del riesgo 🛡️

Admite dos modos de riesgo: porcentaje y cantidad fija, además de un mecanismo de protección contra la quiebra. Es como tener cinturón de seguridad y airbag en un coche, ¡protegiendo tu cuenta de manera más segura!

🎪 Escenarios de aplicación práctica

Ideal para estas situaciones:

- Buscar oportunidades de ruptura en mercados laterales ⚡

- Puntos de reingreso en tendencias durante retrocesos 📈

- Sniper preciso cerca de niveles importantes de soporte/resistencia 🎯

Guía para evitar errores:

- Pausar su uso antes de noticias importantes

- Tener precaución con criptomonedas de baja liquidez

- Ajustar los parámetros de riesgo según la volatilidad del mercado

🚀 ¿Por qué elegir esta estrategia?

Las estrategias tradicionales o dan muy pocas señales perdiendo oportunidades, o dan demasiadas señales cayendo en falsas rupturas. Esta estrategia, mediante múltiples mecanismos de filtrado, logra ataques precisos con el lema "menos es más".

Y lo mejor es que todos los parámetros son personalizables, como un ingeniero de sonido ajustando el ecualizador. Puedes "sintonizar" el ritmo de trading más adecuado según las diferentes condiciones del mercado 🎵

Recuerda: una buena estrategia no es la que te hace operar todos los días, sino la que te permite actuar cuando tienes más certeza. ¡Esa es la magia de la estrategia FVG! ✨

- 1