Estrategia del ciclo de halving de Bitcoin

Estrategia del ciclo de halving: datos históricos muestran un rendimiento promedio superior al 1000%

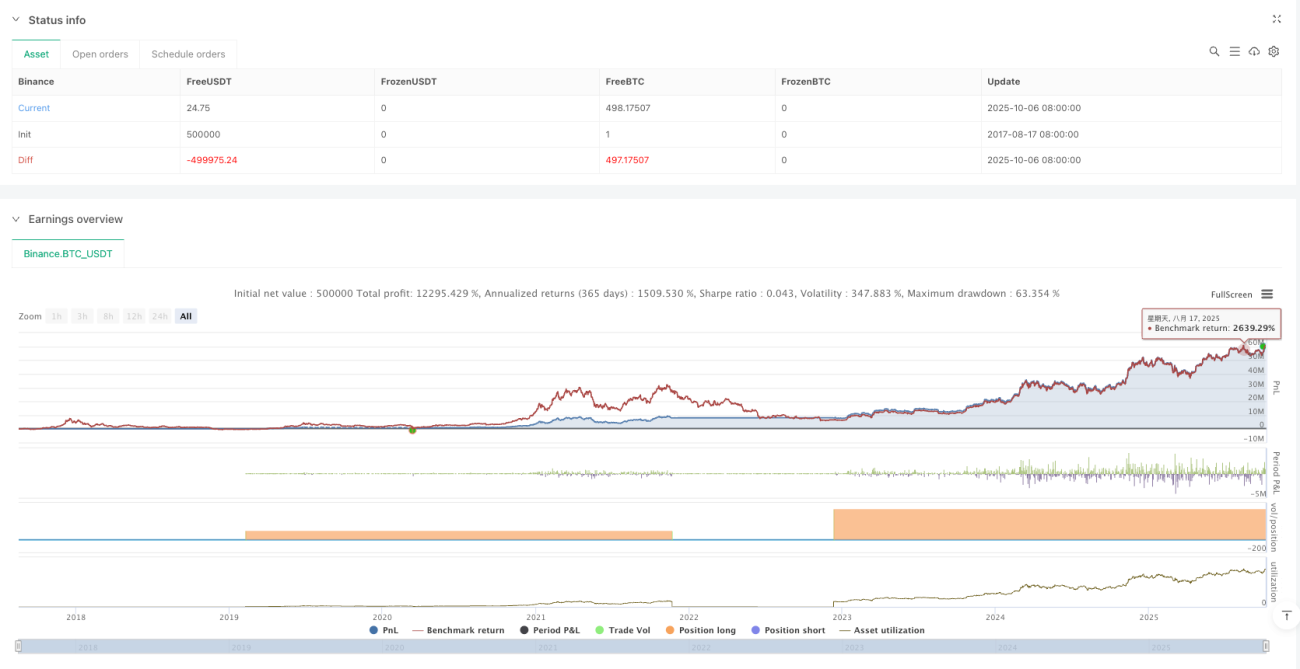

Esta no es otra estrategia de análisis técnico, sino un marco de inversión a largo plazo basado en el ciclo de halving de 4 años de Bitcoin. Los datos de backtesting muestran que, siguiendo estrictamente los puntos temporales del halving para comprar y vender, el rendimiento máximo en un solo ciclo puede superar el 2000%. Pero no se emocione demasiado, esta estrategia requiere una gran fuerza de voluntad y tolerancia al riesgo.

La lógica central es simple y directa: comprar en el halving, vender en lotes después de 40-80 semanas para obtener ganancias, y reconstruir la posición después de 135 semanas. Suena fácil, pero requiere una voluntad de acero.

Marco operativo de tres fases: una selección de momento más precisa que el DCA tradicional

Fase 1: Periodo de compra en el halving (semanas 0-40)

Construir la posición inmediatamente después del evento de halving, este es el punto de entrada central de toda la estrategia. Los datos históricos muestran que las primeras 40 semanas después del halving son el mejor período de acumulación, cuando el sentimiento del mercado generalmente aún no ha reflejado completamente el impacto de la reducción de la oferta.

Fase 2: Periodo de obtención de ganancias (semanas 40-80)

Las semanas 40-80 posteriores al halving son históricamente la ventana dorada para el estallido del precio de Bitcoin. Tras el halving de 2016, Bitcoin subió más del 3000% en la semana 78, y de manera similar después del halving de 2020. Esta ventana de tiempo no es una suposición, sino una deducción matemática basada en los fundamentos de oferta y demanda.

Fase 3: Periodo de acumulación en mercado bajista (después de la semana 135)

Normalmente, 135 semanas después del halving se entra en un mercado bajista profundo, momento en el que se inicia la estrategia DCA. Esta elección de momento es superior al DCA ciego, ya que evita inversiones ineficaces en los picos del mercado alcista.

Control de riesgos: no es una estrategia de victoria segura, requiere disciplina estricta

Mayor riesgo: falta de ejecución

El mayor enemigo de la estrategia no es la volatilidad del mercado, sino la naturaleza humana. Comprar en el halving requiere actuar en contra de la corriente cuando el mercado es pesimista, y obtener ganancias requiere mantener la calma en medio del frenesí. La historia muestra que el 90% de las personas no puede ejecutar completamente la estrategia.

Requisitos de gestión de capital

Se recomienda no invertir más del 20% del capital total en una sola operación, ya que un solo ciclo puede enfrentar una caída de más del 80%. En el mercado bajista de 2018, Bitcoin cayó de 20,000 a 3,200 dólares, e incluso comprando en el momento "correcto" se sufrirían grandes pérdidas flotantes.

Riesgo de cambios en el entorno del mercado

La estrategia se basa en datos de 3 ciclos completos, pero el mercado de Bitcoin se está volviendo más maduro. La entrada de capital institucional, la aprobación de ETFs y otros factores pueden alterar el patrón cíclico tradicional. El rendimiento pasado no garantiza resultados futuros, esto no es solo una frase hecha.

Configuración de parámetros: basada en modelos matemáticos, no en juicios subjetivos

Punto de inicio de ganancias a las 40 semanas: Basado en el cálculo del punto de equilibrio de oferta y demanda después del halving. Salir demasiado pronto podría hacer perder el movimiento principal, demasiado tarde podría quedar atrapado en el pico.

Punto final de ganancias a las 80 semanas: Los datos históricos muestran que la semana 80 después del halving es un intervalo de alta probabilidad para el tope de precio. En este momento, se debe comenzar a reducir la posición gradualmente, sin codiciar el último tramo de subida.

Inicio del DCA a las 135 semanas: Es la solución estadísticamente óptima para la zona de fondo del mercado bajista, donde la relación riesgo-beneficio al comenzar el DCA es la mejor.

Consejos prácticos: adecuado para inversores a largo plazo, no para trading a corto plazo

Esta estrategia es adecuada para capital con un horizonte de inversión de más de 5 años, no para inversores que necesiten el dinero pronto o tengan baja tolerancia al riesgo. Un solo ciclo requiere soportar un período de pérdidas flotantes de 2-3 años, lo que supone una gran presión psicológica.

La tasa de éxito de la estrategia no radica en predecir el precio a corto plazo, sino en aprovechar el ciclo de oferta y demanda a largo plazo. El halving de Bitcoin es un evento determinista, pero el momento y la magnitud de la reacción del precio siguen siendo inciertos.

Aviso importante: Esta es una estrategia de inversión de alto riesgo, con la posibilidad de perder todo el capital. Los datos históricos de backtesting no garantizan rendimientos futuros. Antes de invertir, evalúe cuidadosamente su propia tolerancia al riesgo.

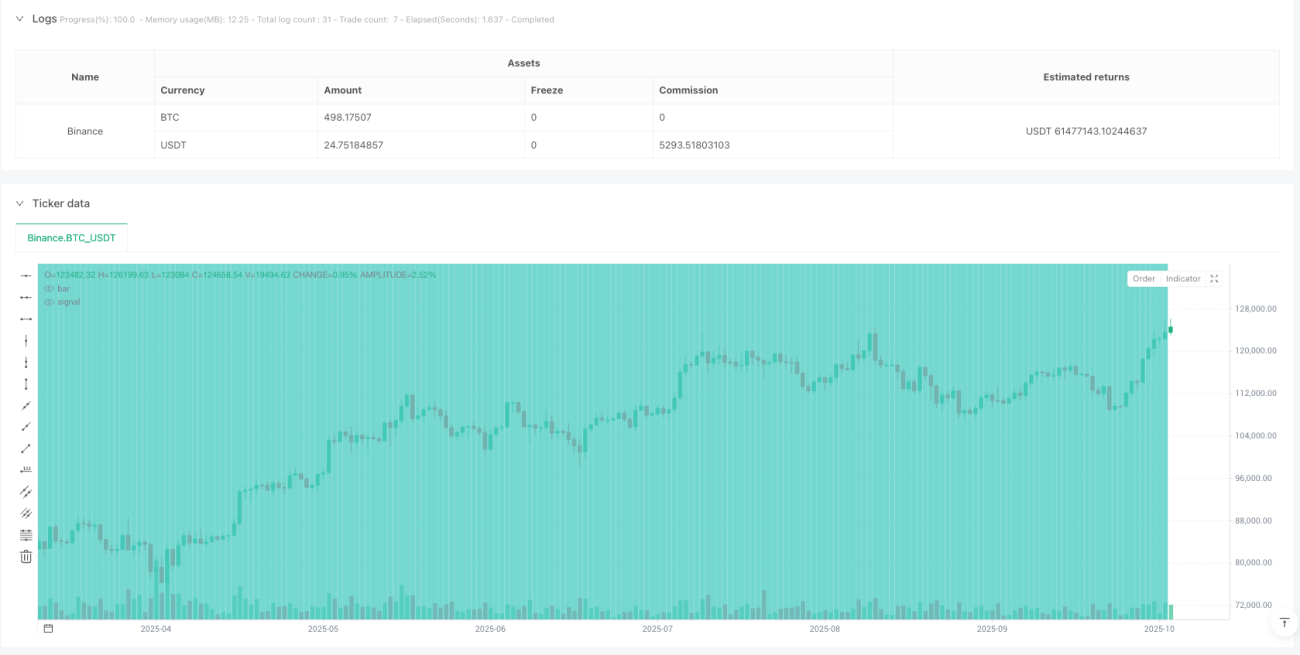

/*backtest

start: 2017-08-17 08:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT","balance":500000}]

*/

//@version=6

strategy(title='Bitcoin Halving Cycle Profit - Backtesting', shorttitle='BTC Halv', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.1)

// ════════════════════════════════════════════════════════════════════════════════════════════════- 1