Estrategia de promedio escalonado de tendencia: ¿cómo "relajarse" elegantemente cuando el mercado está lateral?

¿Por qué las estrategias tradicionales de seguimiento de tendencia fallan con frecuencia en mercados laterales?

Como profesional del trading cuantitativo, a menudo me preguntan: ¿por qué las estrategias que funcionan de maravilla en mercados con tendencia sufren grandes retrocesos en cuanto el mercado entra en rango?

La respuesta es sencilla: la mayoría de las estrategias de seguimiento de tendencia padecen un "trastorno obsesivo-compulsivo por la tendencia": siempre intentan mantener un trading de alta frecuencia en cualquier entorno de mercado, ignorando un hecho básico: el 70% del tiempo el mercado se encuentra en un rango lateral.

La estrategia "Promedio escalonado de tendencia" que analizamos hoy aborda este punto débil con una solución interesante: seguir activamente en mercados con tendencia y "descansar con elegancia" en mercados laterales.

¿Qué es el "promedio escalonado"? ¿Cómo redefine este concepto el seguimiento de tendencia?

Las estrategias tradicionales de medias móviles tienen un defecto fatal: siempre están cambiando. Tanto si el mercado está en una fuerte tendencia como en un rango lateral, la media se ajusta constantemente con las fluctuaciones de precio, generando así numerosas señales falsas.

La idea central del "promedio escalonado" es: "congelar" la media móvil bajo condiciones específicas.

La lógica de implementación concreta es la siguiente:

-

Detección del estado de tendencia: se evalúa la fuerza de la tendencia mediante el indicador ADX.

- ADX > 25: mercado con tendencia fuerte.

- Pendiente de la media móvil < 0.3 %: mercado lateral.

-

Conmutación dinámica de la media móvil:

- En tendencia fuerte: seguimiento normal con EMA(21).

- En lateral: la media se "congela" en una posición horizontal, formando soporte/resistencia.

La sutileza de este diseño es que la estrategia muestra diferentes "personalidades" según el entorno de mercado: sensible en tendencia, estable en lateral.

¿Cómo implementar el sistema de "captura de tendencia"?

Además del mecanismo básico de promedio escalonado, la estrategia integra un módulo de "captura de tendencia", que considero la parte más innovadora:

Mecanismo de reversión rápida:

- Cuando aparece una fuerte tendencia opuesta justo después de cerrar una posición.

- Se abre una nueva posición rápidamente en un plazo de 3 periodos.

- Condición: ADX > 30 y la diferencia entre DI+ y DI- > 10.

Este diseño resuelve un problema importante de las estrategias tradicionales: cómo ajustar rápidamente la posición al inicio de una reversión de tendencia.

Imaginemos una situación: acabas de cerrar una posición larga por stop loss y el mercado inmediatamente forma una fuerte tendencia bajista. Las estrategias tradicionales tendrían que esperar a que se confirme una nueva señal, pero este sistema de "captura de tendencia" puede abrir una posición corta en menos de 3 periodos.

Gestión de riesgos: ¿por qué distinguir entre estados de mercado?

Lo más valioso de esta estrategia es su mecanismo de gestión de riesgos diferenciado:

Control de riesgos en mercado lateral:

- Ajustar el stop loss cerca de la media escalonada.

- Reducir el múltiplo de ATR, apretando el stop.

- Establecer objetivos más conservadores.

Control de riesgos en mercado con tendencia:

- Usar el múltiplo de ATR estándar para el stop.

- Activar el trailing stop escalonado.

- Permitir un mayor margen de fluctuación del precio.

Este diseño refleja una filosofía importante en trading: diferentes entornos de mercado requieren diferente tolerancia al riesgo. En mercados laterales debemos ser más cautos; en mercados con tendencia necesitamos dar más espacio a las ganancias.

Trailing stop escalonado: ¿cómo equilibrar protección de beneficios y seguimiento de tendencia?

Los trailing stops tradicionales suelen ser demasiado mecánicos: o demasiado ajustados, provocando salidas prematuras, o demasiado laxos, sin proteger las ganancias de forma efectiva. El trailing stop escalonado de esta estrategia ofrece una solución más inteligente:

Lógica del escalonamiento:

- La distancia entre escalones se calcula dinámicamente en función del ATR.

- Se pueden configurar hasta 5 niveles de escalón.

- Cada vez que se supera un escalón, el stop loss se eleva en consecuencia.

La ventaja de este diseño es que protege las ganancias y al mismo tiempo da suficiente espacio para que la tendencia se desarrolle.

¿Qué hay que tener en cuenta en la aplicación práctica?

Basándome en mi experiencia en trading real, al usar este tipo de estrategia conviene prestar atención a lo siguiente:

-

La trampa de la optimización de parámetros: No optimizar en exceso el umbral del ADX; valores entre 25 y 30 suelen ser estables en la mayoría de los mercados.

-

Adaptabilidad al mercado: La estrategia funciona mejor en mercados con volatilidad moderada. En entornos de volatilidad extrema puede ser necesario ajustar el múltiplo de ATR.

-

Gestión de capital: Se recomienda que cada posición no supere el 10% del capital total, especialmente cuando se activa la función de captura de tendencia.

-

Trampas del backtesting: Prestar especial atención al impacto del deslizamiento y las comisiones, sobre todo en el trading frecuente en mercados laterales.

¿Cuál es el valor innovador de esta estrategia?

Desde la perspectiva del desarrollo de estrategias cuantitativas, esta estrategia representa una importante dirección evolutiva: el paso de una lógica única a una adaptación multiestado.

Las estrategias tradicionales suelen intentar enfrentarse a todas las situaciones de mercado con una lógica fija, mientras que esta estrategia muestra la sabiduría de "adaptarse a las condiciones locales":

- En mercados con tendencia se comporta como un agresivo seguidor de tendencia.

- En mercados laterales se comporta como un conservador operador de rango.

Esta forma de pensar es una inspiración importante para los desarrolladores de estrategias: debemos dotar a las estrategias de la capacidad de "percibir el mercado", en lugar de ejecutar ciegamente una lógica fija.

Por último, hay que subrayar que ninguna estrategia es universal. Aunque esta estrategia de promedio escalonado es elegante en teoría, en la práctica debe ajustarse al entorno de mercado concreto y a las preferencias de riesgo personales. Recuerda: la mejor estrategia siempre es la que mejor se adapta a ti.

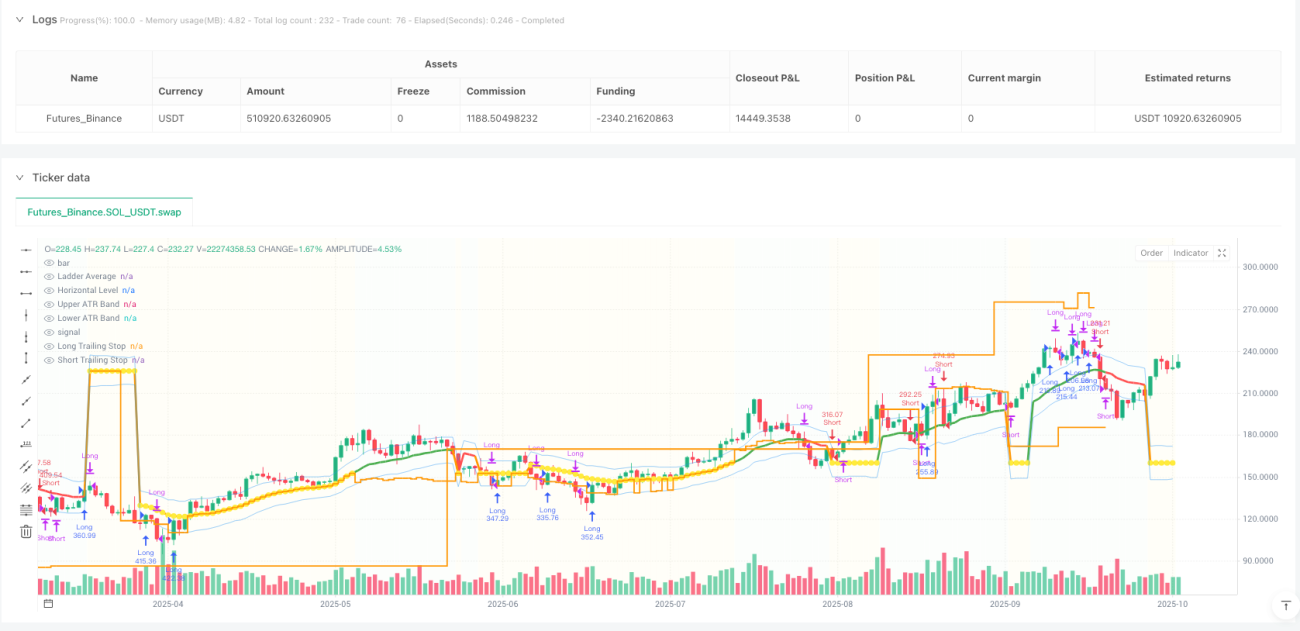

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1