🎯 ¿Qué estrategia tan mágica es esta? ¡20 indicadores trabajando juntos!

¿Sabías? Esta estrategia es como tener un asistente de inteligencia artificial súper inteligente para tus operaciones. Monitorea simultáneamente 20 señales diferentes del mercado, y solo cuando la mayoría de los indicadores dicen "adelante", te da una recomendación de trading. ¡Es como comprar una casa: solo cuando la ubicación, el precio, la distribución, el transporte… todo te satisface, tomas la decisión!

¡Punto clave! No es una estrategia de un solo indicador común, sino un "sistema de resonancia multidimensional". Imagina: si solo un amigo te dice que una acción es buena, quizás dudes; pero si 20 amigos expertos te lo confirman, ¿no tendrías más confianza?

📊 Desvelando el arsenal principal

Los tres mosqueteros de la identificación de tendencias 🗡️

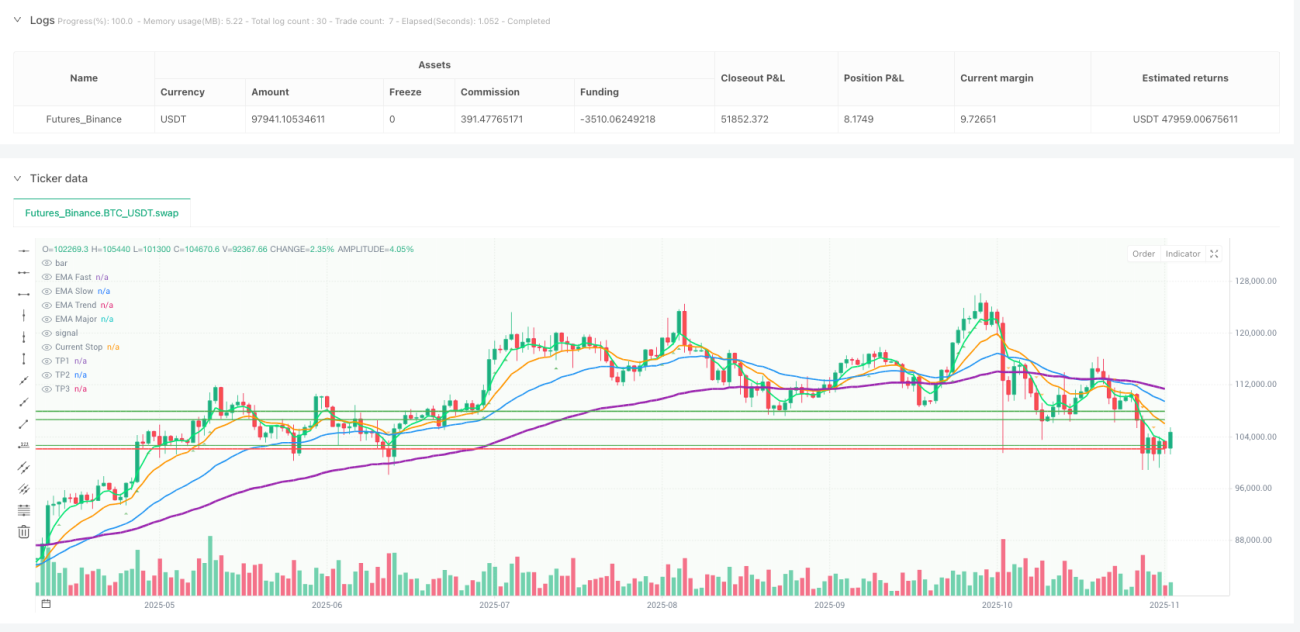

- EMA rápida (5) vs EMA lenta (13): detectan giros de tendencia a corto plazo

- EMA de filtro de tendencia (34): confirman la dirección a medio plazo

- EMA de tendencia principal (89): capturan la gran dirección sin dejarse engañar por pequeños movimientos

Análisis multi-temporal ⏰

¡Esta función es genial! La estrategia analiza simultáneamente las tendencias de 1 hora y 4 horas, como cuando conduces: miras tanto el camino inmediato como la ruta general del GPS. Evita la incómoda situación de "el marco temporal pequeño dice alcista, el grande dice bajista".

Gestión inteligente del riesgo 🛡️

- Ajuste dinámico del tamaño de la posición: se adapta automáticamente según la volatilidad del mercado

- Toma de ganancias parciales: sin codicia, se recoge una parte cuando es favorable

- Stop loss móvil: protección de ganancias

🔥 La lógica de trading con 20 seguros

Señales para ir largo (comprar) requieren:

- Tendencia alcista: todas las EMAs en orden alcista

- Momento suficiente: RSI, MACD, RSI estocástico dan luz verde

- Volumen de confirmación: subidas con volumen son genuinas

- Estructura de mercado saludable: máximos crecientes

- Soporte de liquidez: niveles de soporte clave intactos

Las señales para ir corto son exactamente opuestas.

Guía para evitar errores ⚠️: La estrategia también incluye una "detección de compresión de Bandas de Bollinger". Cuando el mercado está demasiado plano, pausa las operaciones para evitar ser zarandeado en mercados laterales.

💰 El secreto para maximizar ganancias

Estrategia de toma de ganancias por tramos 📈

- Primer objetivo: con 2 veces el riesgo/beneficio, vender el 30% de la posición

- Segundo objetivo: con 3.5 veces, vender otro 40%

- Resto de la posición: proteger con stop loss móvil, dejando correr las ganancias

Mejora del stop loss inteligente 🎯

Al alcanzar 2.5 veces el beneficio, el stop loss se mueve automáticamente al precio de coste, asegurando que esta operación al menos no pierda. ¡Es como comprar un seguro para tus ganancias!

Stop loss dinámico de seguimiento 🏃♂️

Cuando los beneficios alcanzan cierto nivel, el stop loss sigue el precio como una sombra, protegiendo las ganancias y dejando espacio para que el precio suba.

🚀 ¿Por qué esta estrategia es tan potente?

- Cobertura completa: análisis técnico, gestión de capital, control de riesgos, todo incluido

- Filtro inteligente: 20 condiciones que seleccionan cuidadosamente, aumentando enormemente la tasa de éxito

- Alta adaptabilidad: análisis multi-temporal, adecuado para diferentes entornos de mercado

- Diseño humanizado: ejecución automatizada, evitando trading emocional

Esta estrategia es como tener un equipo de traders experimentados metido en código, trabajando 24/7 sin descanso para encontrar las mejores oportunidades de trading.

/*backtest

start: 2024-11-12 00:00:00

end: 2025-11-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('Amir Mohammad Lor ', shorttitle='MPF', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15, pyramiding=0, max_bars_back=1000)

// === INPUTS ===- 1